Relocating out West represents the ultimate retirement dream for many, but picturesque mountain towns and desert oases often harbor hidden challenges that quickly drain your savings and compromise your health. Before packing up for the frontier, you must evaluate extreme weather patterns, soaring housing costs, and surprisingly sparse medical networks. Western retirement towns frequently market their scenery while downplaying severe wildfire seasons, water shortages, and isolation from specialized care. Evaluating these locations with a critical eye prevents costly relocation mistakes that trap retirees in unsuitable environments. By understanding the genuine drawbacks of these popular western retirement destinations, you can make an informed decision that protects your financial security and ensures your physical well-being throughout your golden years.

Mountain Towns With Hidden Hardships

The allure of the Rocky Mountains and the Pacific Northwest is undeniable. Waking up to snow-capped peaks and pristine pine forests sounds like a permanent vacation. However, the realities of aging in these rugged environments often force retirees into a secondary, much more stressful relocation just a few years later.

1. Bend, Oregon

Bend consistently ranks at the top of magazines’ “best places to retire” lists, celebrated for its craft breweries, river trails, and mountain biking. Unfortunately, the reality of living in Central Oregon has shifted dramatically over the past decade. The most severe drawback is the summer wildfire season. As a retiree seeking fresh air, you may find yourself trapped indoors from July through September, running expensive HEPA air purifiers because the Air Quality Index routinely reaches hazardous levels. Furthermore, the influx of remote workers has pushed the median home price to staggering heights, driving up property taxes and local service costs. For retirees on a fixed income, the math in Bend rarely works out favorably anymore.

2. Bozeman, Montana

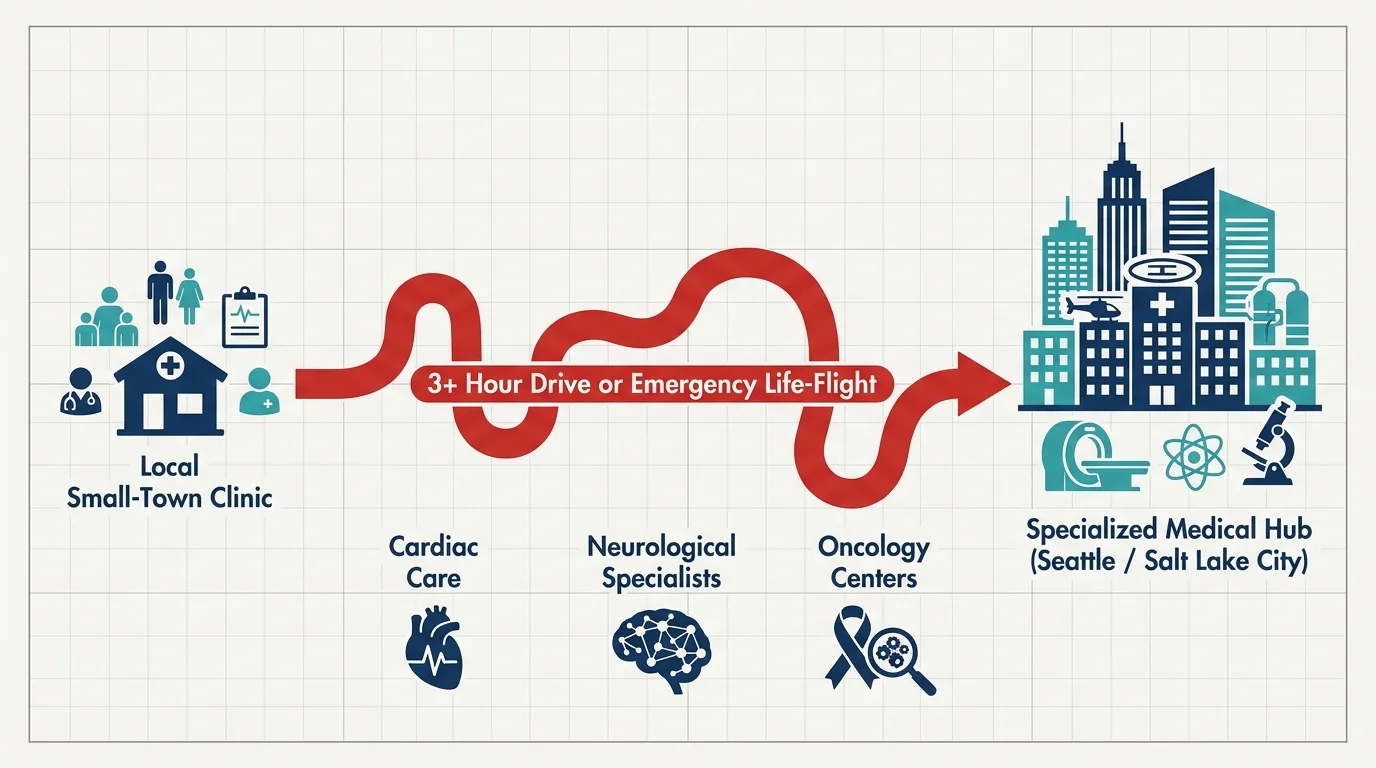

Often romanticized by television shows and western folklore, Bozeman attracts retirees looking for wide-open spaces and authentic western charm. The disappointment sets in when November arrives. Winter in Bozeman is brutal and long, frequently lasting a full seven months. Shoveling heavy snow and navigating sheets of black ice pose severe physical risks; a single slip-and-fall can permanently alter your retirement trajectory. Additionally, while Bozeman has a competent local hospital, treating complex cardiac, neurological, or oncological conditions often requires a strenuous drive or a flight to larger medical hubs in Seattle or Salt Lake City.

3. Jackson, Wyoming

Jackson offers unparalleled beauty at the doorstep of the Grand Tetons, coupled with Wyoming’s incredibly tax-friendly environment. Yet, it operates as an enclave for the ultra-wealthy. Unless you are bringing an eight-figure portfolio, you will likely feel the crushing weight of the local economy. Everything from groceries to home maintenance carries a massive premium. More importantly, the extreme isolation of the Jackson Hole valley becomes a distinct liability as you age. The area lacks a robust, multi-disciplinary senior healthcare infrastructure, meaning any severe medical emergency often triggers a costly life-flight out of the valley.

Desert Oases Facing Environmental Realities

Trading snow shovels for golf clubs drives tens of thousands of retirees to the American Southwest. The sunshine is abundant, but the environmental fragility and explosive population growth in these desert towns create significant long-term risks for seniors.

4. Sedona, Arizona

The majestic red rocks of Sedona offer a deeply spiritual and visually stunning backdrop for retirement. However, the town’s infrastructure was never designed for the millions of tourists who flood the area annually. Retirees living in Sedona frequently complain that they cannot leave their driveways on weekends due to miles-long traffic jams along State Route 89A. The cost of living is exceptionally high, and essential services are strained. Most concerning for retirees is the healthcare situation; while Sedona has clinics, residents must frequently travel 45 minutes to Cottonwood or nearly two hours to Phoenix for specialized medical procedures or acute hospital care.

5. Palm Springs, California

Palm Springs is a mid-century modern paradise that caters heavily to the 55-plus demographic. The primary disappointment here is the punishing summer climate. While the winters are glorious, the temperatures from June through October routinely exceed 115 degrees. Retirees often find themselves experiencing a “summer hibernation,” staying confined to heavily air-conditioned spaces for months on end. This isolation takes a toll on mental health and social lives. Additionally, you must navigate California’s high state income tax, which applies to various forms of retirement income, and manage sky-high utility bills required to cool your home for half the year.

6. St. George, Utah

Situated in the southwestern corner of Utah, St. George has exploded in popularity due to its proximity to Zion National Park and relatively lower cost of living compared to neighboring states. However, the area faces an existential threat: a severe, ongoing water crisis. Built in a harsh desert, the region relies heavily on the overallocated Colorado River basin. Retirees moving here are often shocked by strict water rationing protocols and the corresponding spike in utility costs. The relentless summer heat also limits outdoor activities, and the cultural landscape can feel remarkably homogenous, which may isolate those looking for diverse, varied social circles.

High-Altitude and Rapidly Changing Havens

Some western destinations fail retirees not because of heat or isolation, but due to physiological challenges and rapid socioeconomic shifts that completely change the character of the town.

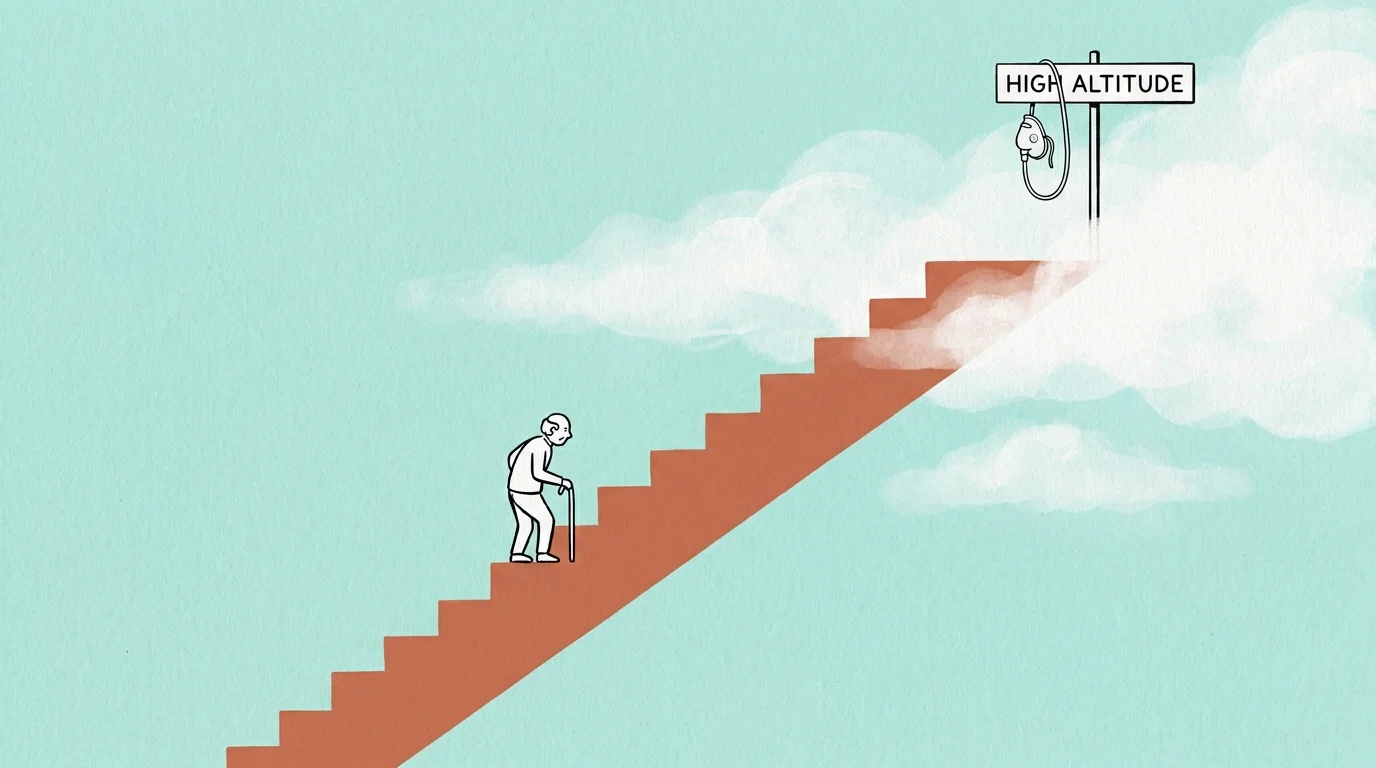

7. Santa Fe, New Mexico

Santa Fe is a cultural treasure, rich with art galleries, world-class cuisine, and distinctive adobe architecture. The hidden danger here is the elevation. Sitting at over 7,100 feet above sea level, the thin air can wreak havoc on an aging body. Retirees with mild, previously unnoticeable heart conditions, high blood pressure, or chronic obstructive pulmonary disease (COPD) often find their symptoms severely exacerbated upon moving to Santa Fe. Many seniors spend heavily to relocate here, only to have their doctors order them to move back down to sea level a year later. Combined with a surprisingly high crime rate in certain surrounding areas and an expensive housing market, Santa Fe requires extreme caution.

8. Coeur d’Alene, Idaho

Northern Idaho has become a magnet for retirees fleeing high taxes and urban congestion. Coeur d’Alene offers beautiful lakes and outdoor recreation, but the transition can be jarring. First, the region experiences deeply gloomy, overcast winters that stretch for months, which can trigger seasonal affective disorder (SAD) in those used to sunny climates. Second, the massive recent influx of new residents has caused property values to skyrocket. This has led to drastic property tax reassessments, shocking retirees on fixed incomes who assumed moving to Idaho would secure their financial stability.

9. Reno, Nevada

Marketed as the “Biggest Little City in the World,” Reno boasts no state income tax and close proximity to Lake Tahoe. Unfortunately, Reno sits in a geographic bowl that frequently acts as a sink for wildfire smoke blowing over the Sierra Nevada mountains from California. The air quality during late summer can be abysmal. Furthermore, the influx of tech companies has transformed the local economy; housing prices have surged, pricing out many middle-class retirees. The persistent, pervasive casino culture dominating the downtown core also tires quickly for residents looking for a tranquil retirement environment.

Evaluating Healthcare Access in the West

The single most critical failure point in a western retirement relocation is underestimating the drop in healthcare quality and accessibility. Moving from a densely populated suburb to a rugged western town means giving up competitive hospital systems and vast networks of specialists.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

Before you commit to a western destination, compare the structural realities of healthcare and daily living. Use this baseline comparison to guide your research:

| Relocation Factor | Traditional Suburb / City | Remote Western Town | Retirement Impact |

|---|---|---|---|

| Specialized Medicine | Multiple competing hospital networks within 20 miles. | Basic urgent care; specialists visit once a month or require travel. | Delayed diagnoses and massive travel expenses for chronic care management. |

| Medicare Advantage | Robust, highly competitive network options. | Few, if any, in-network providers. May require switching to Original Medicare. | Higher out-of-pocket costs and fewer predictable copays. |

| Emergency Response | Ambulance response in under 10 minutes. | Volunteer EMS; potential weather delays for life-flight helicopters. | Higher risk of permanent injury or death during acute cardiac or stroke events. |

| Caregiving Services | Large pool of home health aides and assisted living facilities. | Severe labor shortages; multi-year waitlists for memory care. | Spouses bear the total burden of caregiving, leading to extreme physical burnout. |

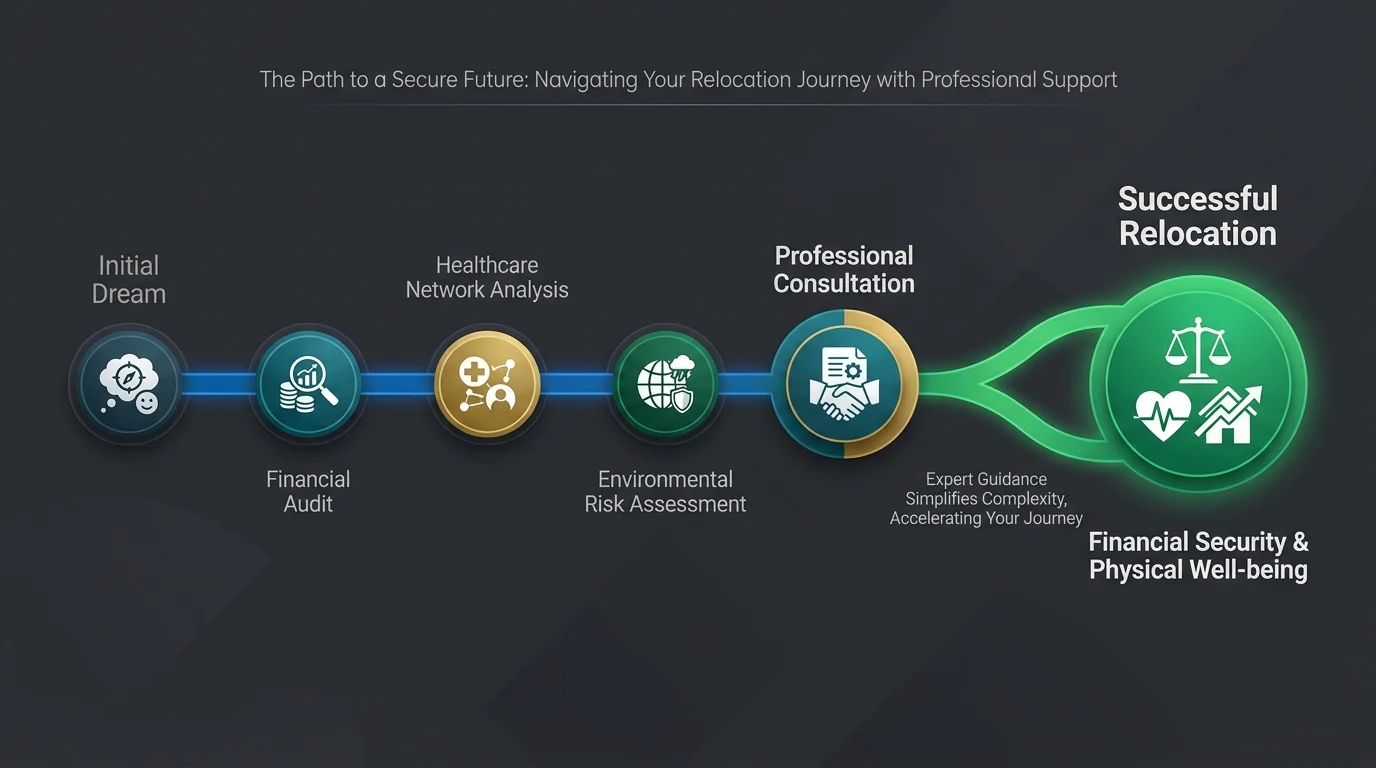

The Pre-Move Reality Check

To avoid becoming a cautionary tale, you need a methodical approach to evaluating any western retirement destination. Take these specific actions before you contact a real estate agent:

- Rent During the Worst Season: Do not just visit Sedona in April or Bozeman in September. Rent an Airbnb in Palm Springs in August, or stay in Bend during peak fire season in August. You must experience the area when the climate is at its most hostile.

- Audit the Medical Network: Call your current health specialists and ask for their exact equivalents in your target town. Then, log into Medicare.gov and verify that those specific doctors accept your coverage. If you use a Medicare Advantage plan, you may find your network completely evaporates across state lines.

- Investigate Water and Utilities: In the West, water is wealth. Speak to local utility companies about historical rate increases over the last five years and ask about community water rights. A cheap house in the desert is worthless if the municipality restricts your water usage.

- Calculate the “Grandchild Tax”: Map out the exact logistics and costs required to visit your family. If flying out of Jackson or Bozeman requires three layovers and $800 per ticket, you will see your family far less often than you hope.

Don’t Make These Mistakes

Emotional decision-making drives most relocation regrets. Retirees frequently confuse a beloved vacation spot with a practical daily living environment. When you vacation, you tolerate traffic, ignore the cost of groceries, and rarely think about the proximity to an oncology center. When you live there, those factors dictate your quality of life.

Another common mistake is failing to test the social waters. Western towns often have highly entrenched local populations. If you move to a small mountain town and do not ski, mountain bike, or fly fish, you may find it incredibly difficult to build a new social network. Loneliness is a profound health risk for seniors, matching the physiological impacts of smoking. Do not move somewhere beautiful if it means moving somewhere lonely.

When Professional Advice Is Worth It

Relocating across state lines during retirement is a complex legal and financial maneuver. The stakes are too high to rely solely on internet research. It is highly recommended to engage professionals before making your final decision.

First, consult a fiduciary financial advisor or tax professional to model your new tax burden. Moving from a high-tax state to a no-income-tax state like Nevada or Wyoming sounds great, but those states often make up the difference through aggressive sales taxes, vehicle registration fees, and property taxes.

Second, work with a State Health Insurance Assistance Program (SHIP) counselor. These federally funded, unbiased experts can help you navigate how your Medicare coverage will change when you cross state lines. They will ensure you do not inadvertently trigger a lapse in coverage or step into a massive out-of-network billing situation.

Finally, consider utilizing the Eldercare Locator, a public service of the U.S. Administration on Aging. By entering the ZIP code of your prospective new home, you can instantly connect with the local Area Agency on Aging to evaluate the community support services, transportation options, and home modification assistance available in that specific western town.

Frequently Asked Questions

What is the worst western state to retire in for taxes?

California generally imposes the highest overall tax burden, including high income taxes, sales taxes, and taxes on certain retirement distributions. However, property taxes in states like Texas and Idaho can also severely impact fixed-income retirees, proving that “no income tax” does not always mean “cheap.”

How does high altitude affect aging bodies?

At elevations above 5,000 feet, the air contains less oxygen per breath. This forces your heart and lungs to work significantly harder. For seniors with pulmonary issues, asthma, or cardiovascular disease, this can lead to chronic fatigue, dizziness, and dangerous exacerbations of existing conditions.

Will my Medicare Advantage plan work if I move to a western state?

Typically, no. Medicare Advantage plans operate on localized, county-by-county networks. If you move out of your plan’s service area, you qualify for a Special Enrollment Period. You must use this time to either select a new Medicare Advantage plan in your new ZIP code or return to Original Medicare and purchase a Medigap policy. Always verify options on Medicare.gov before moving.

Are there tools to calculate the true cost of living in a new state?

Yes. Organizations like AARP offer Livability Indexes, and financial institutions provide cost-of-living calculators. You should specifically look at the costs of healthcare, utilities (heating in the mountains, cooling in the desert), and home insurance, as western states are seeing massive insurance premium spikes due to wildfire risks.

Your retirement years should be a time of peace, stability, and enjoyment, not a constant battle against extreme weather, high costs, and medical scarcity. Take the time to aggressively vet your dream destination. Look past the scenic postcards and evaluate the rugged reality of daily western living. Start by auditing the local healthcare network in your desired town today—it is the single most important step you can take toward a secure retirement relocation.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Medicare rules, Social Security benefits, and tax laws change regularly—verify current details at Medicare.gov, SSA.gov, or with a licensed professional.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.