Your carefully calculated nest egg might look perfect on paper until invisible tax leaks slowly drain thousands of dollars from your accounts. Many retirees focus exclusively on saving during their working years, completely overlooking how the IRS treats those withdrawals once the paychecks stop. A truly tax-efficient retirement protects your hard-earned wealth from unnecessary depletion through strategic planning rather than guesswork. By understanding how different income streams interact with federal brackets, you take immediate control of your financial future. This guide reveals the hidden vulnerabilities in standard retirement strategies and equips you with actionable methods to plug these costly leaks, ensuring your retirement finances last exactly as long as you need them to.

What You Need to Know

- Location Matters: Every account type—from traditional IRAs to Roths and brokerages—carries unique tax consequences upon withdrawal.

- The Domino Effect: Pulling money from the wrong account at the wrong time can trigger sudden taxes on your Social Security benefits and spike your Medicare premiums.

- Proactive Strategy: Utilizing tools like Roth conversions and Qualified Charitable Distributions (QCDs) before age 73 can significantly lower your lifetime tax bill.

- State Differences: Federal taxes are only half the battle; where you live dramatically impacts how much of your retirement income you actually keep.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” — Robert Kiyosaki

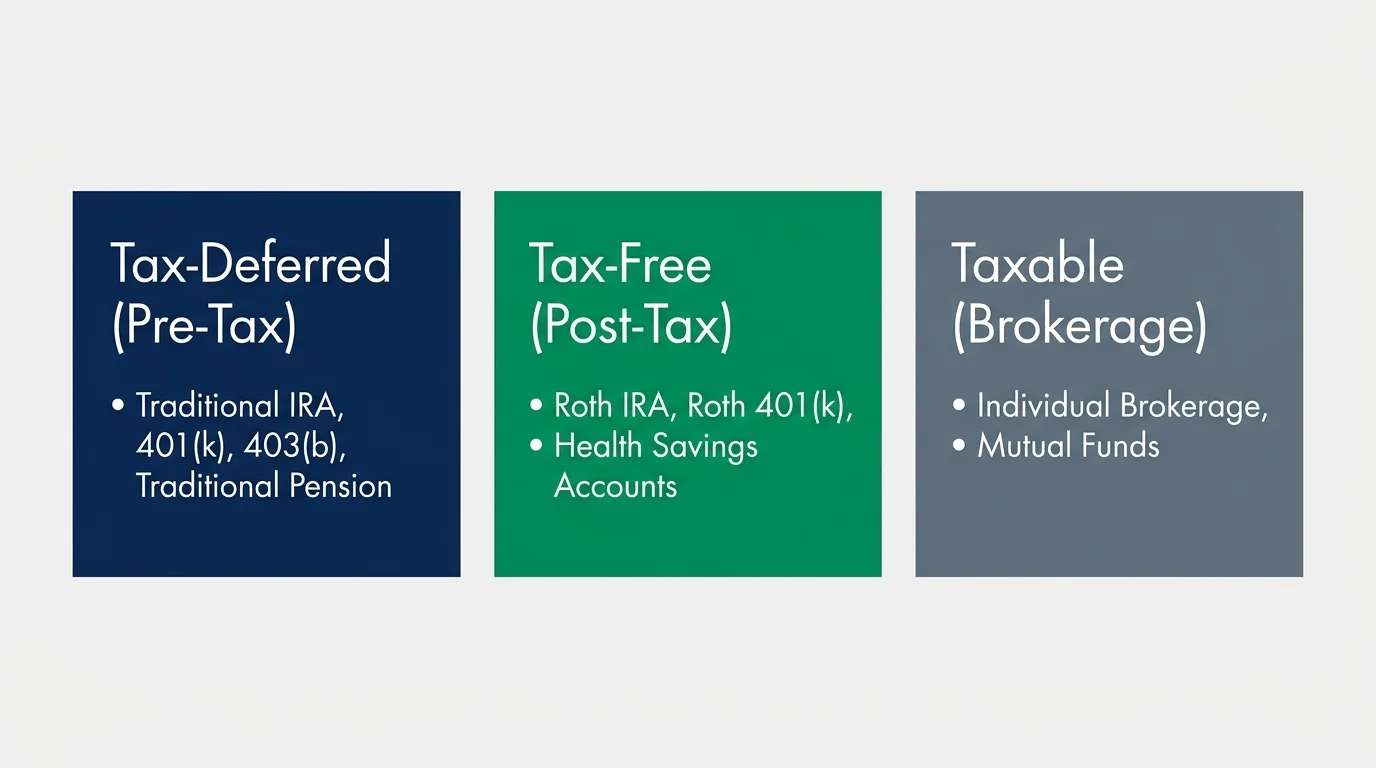

Understanding Your Retirement Income Buckets

Effective retirement tax planning starts with organizing your assets into three distinct buckets. Most Americans spend decades accumulating wealth in tax-deferred accounts, creating a massive future tax liability. To execute a tax-efficient retirement, you need to understand exactly how the IRS views each dollar you withdraw.

| Account Type | Tax Treatment on Contributions | Tax Treatment on Withdrawals | Common Examples |

|---|---|---|---|

| Tax-Deferred (Pre-Tax) | Contributions lower your taxable income today. | Taxed as ordinary income. Required Minimum Distributions (RMDs) apply. | Traditional IRA, 401(k), 403(b), Traditional Pension |

| Tax-Free (Post-Tax) | Contributions are made with after-tax money. | 100% tax-free withdrawals. No RMDs during your lifetime. | Roth IRA, Roth 401(k), Health Savings Accounts (for medical) |

| Taxable (Brokerage) | Funded with after-tax money. No initial tax break. | Subject to capital gains taxes and dividend taxes, which are often lower than ordinary income rates. | Individual brokerage accounts, mutual funds, joint stock accounts |

If 90% of your wealth sits in the tax-deferred bucket, you lose flexibility. Every time you need money for a new car, a roof repair, or a dream vacation, you must withdraw a larger gross amount to cover the associated income taxes. Building up your tax-free and taxable buckets gives you the leverage to dictate your own tax bracket year after year.

The Social Security Tax Torpedo

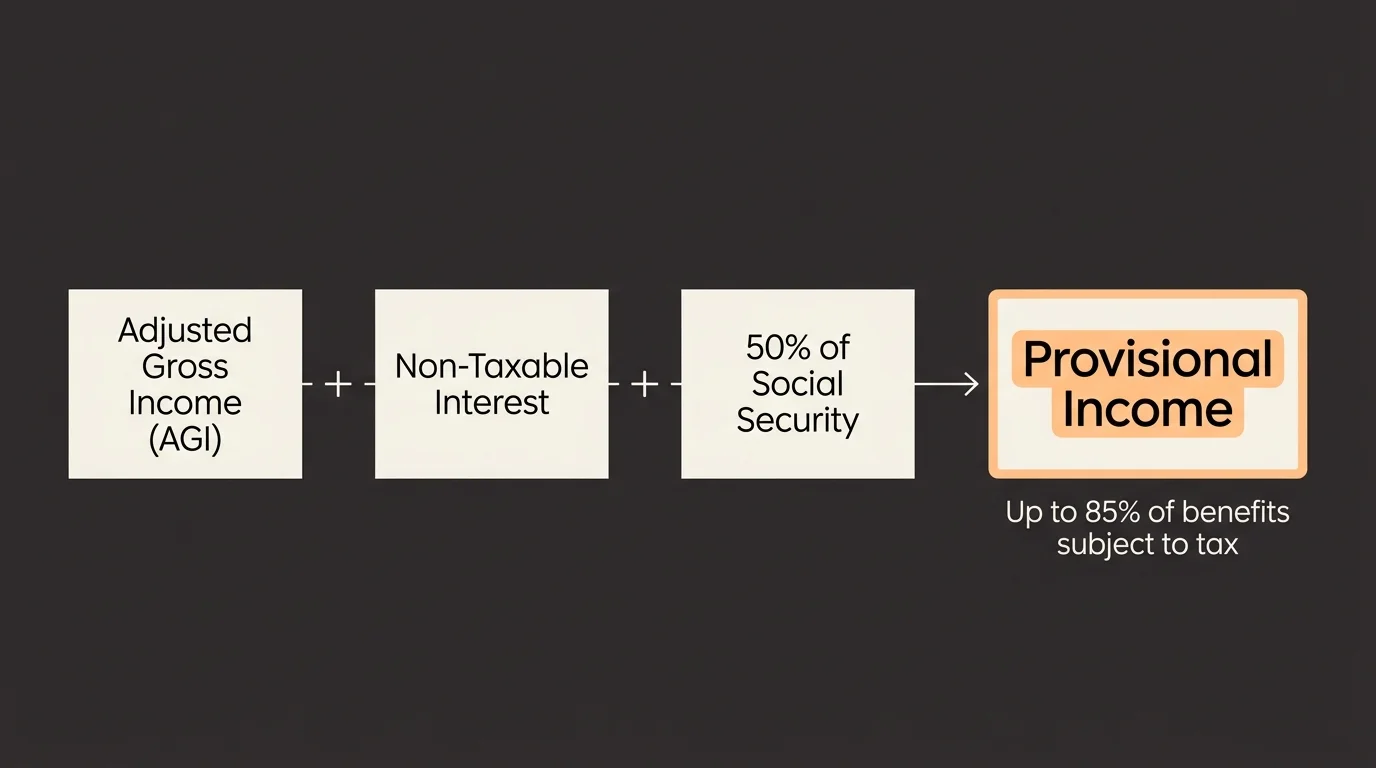

One of the most surprising tax leaks occurs when retirees realize the federal government taxes their Social Security benefits. Depending on your total income, up to 85% of your benefits could be subject to ordinary income tax. The IRS calculates this using a metric called “Provisional Income.”

Your Provisional Income equals your Adjusted Gross Income (AGI) plus any non-taxable interest (like municipal bonds) plus 50% of your Social Security benefits. When you withdraw heavily from your traditional 401(k) to cover living expenses, you push your AGI higher. This artificial income spike triggers the “tax torpedo,” abruptly forcing your Social Security benefits into the taxable category.

By blending your withdrawals—taking some from a taxable brokerage account or a Roth IRA—you keep your Provisional Income low. This strategy preserves the tax-free status of your Social Security checks. To understand exactly how your specific benefit amount factors into this equation, always check your current earnings record through the Social Security Administration.

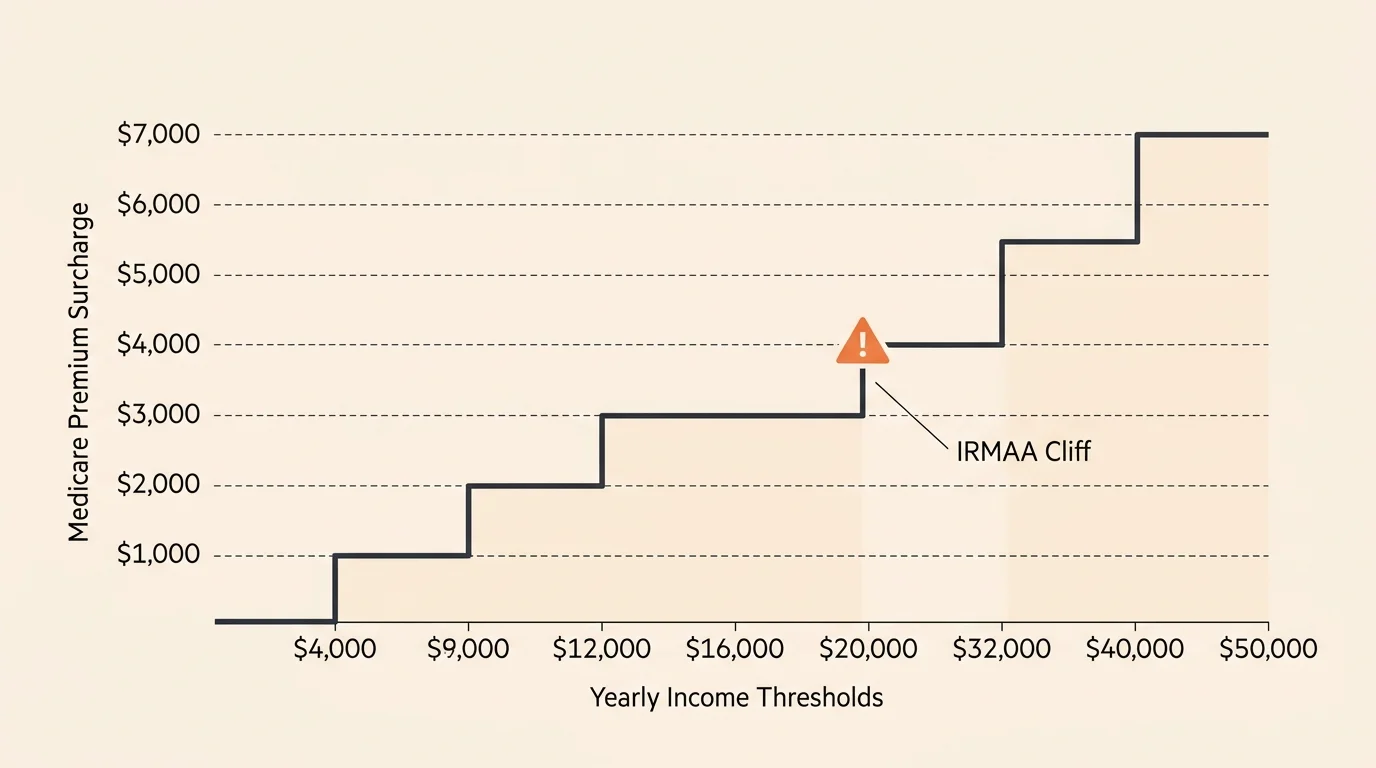

Medicare IRMAA: The Hidden Tax on Health Coverage

Retirement finances face another invisible threat: the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is essentially a surcharge added to your Medicare Part B and Part D premiums if your income exceeds specific thresholds set by the government.

Unlike standard tax brackets, IRMAA operates as a “cliff.” If your Modified Adjusted Gross Income (MAGI) exceeds the limit by even a single dollar, you instantly jump to the next premium tier, potentially costing you and your spouse thousands of dollars in extra healthcare costs for the year.

Medicare looks at your tax return from two years prior to determine your premium. Therefore, a massive traditional IRA withdrawal you take at age 71 will dictate the Medicare premiums you pay at age 73. Navigating this two-year lookback period requires precision. You can review current IRMAA income brackets directly at Medicare.gov to project your future premium costs.

Proven Retirement Tax Strategies

Plugging the leaks in your retirement plan requires action. Implementing these retirement tax strategies can insulate your portfolio against rising tax rates and unexpected surcharges.

Strategic Roth Conversions

A Roth conversion involves moving money from your traditional pre-tax IRA into a Roth IRA. You pay ordinary income tax on the converted amount in the year you make the move. Why do this? By converting smaller amounts strategically over several years—usually during your early retirement years before claiming Social Security or facing RMDs—you “fill up” the lower tax brackets. Once the money sits in the Roth IRA, all future growth and withdrawals are entirely tax-free. This drastically reduces your future RMD obligations and keeps your lifetime tax bill manageable.

Qualified Charitable Distributions (QCDs)

If you give to charity and face Required Minimum Distributions, writing a check from your personal bank account is a massive missed opportunity. A Qualified Charitable Distribution allows you to transfer funds directly from your IRA to an eligible charity. This satisfies your RMD for the year but completely excludes the withdrawn amount from your taxable income. Because the money never touches your AGI, it protects you from the Social Security tax torpedo and Medicare IRMAA cliffs. Review the current limits and guidelines for QCDs via the IRS Retirement Plans portal.

Asset Location

Asset allocation dictates what you invest in; asset location dictates where you hold those investments. Tax-efficient retirement planning requires placing high-growth, highly taxed assets (like taxable bonds or actively managed mutual funds) into your tax-deferred or tax-free accounts. Conversely, you should hold assets that generate long-term capital gains or qualified dividends in your taxable brokerage accounts to benefit from lower, preferential tax rates.

Common Retirement Traps

Even diligent savers fall into specific behavioral traps that trigger unnecessary tax liabilities. Watch out for these common missteps:

- Taking RMDs at the End of the Year: Waiting until December to process your Required Minimum Distribution limits your flexibility. If a market downturn occurs, you are forced to sell assets at a loss just to satisfy the IRS mandate. Schedule distributions systematically throughout the year.

- Ignoring State Taxes: Moving to a new state for the weather without analyzing the tax code can ruin a financial plan. Some states do not tax income but levy brutal property taxes; others tax traditional IRA withdrawals but exempt pensions or Social Security.

- Selling the Wrong Assets for Cash: Liquidating highly appreciated stock in a single calendar year can easily push you into a higher capital gains bracket and trigger the Net Investment Income Tax (NIIT). Always harvest investment losses to offset these gains when generating cash flow.

When to Consult a Professional

You manage your daily budget perfectly, but orchestrating the sequence of withdrawals across multiple tax codes often requires outside expertise. Consult a fiduciary financial planner or a Certified Public Accountant (CPA) well before you turn 73 (the current age RMDs generally begin). Professionals run advanced tax-projection software to map out Roth conversions, calculate optimal withdrawal ratios, and monitor the two-year IRMAA lookback window. If you plan to leave a significant inheritance, an estate planning attorney will help you navigate complex beneficiary rules to ensure your children inherit wealth rather than a massive tax burden.

Frequently Asked Questions

At what age do I have to start taking minimum distributions?

Under current rules established by the SECURE 2.0 Act, Required Minimum Distributions (RMDs) from traditional pre-tax retirement accounts begin at age 73 for individuals born between 1951 and 1959, and age 75 for those born in 1960 or later. Roth IRAs do not require minimum distributions during the original owner’s lifetime.

How much of my Social Security is taxable?

Depending on your Provisional Income, the IRS taxes up to 85% of your Social Security benefits. If your combined income (AGI + nontaxable interest + half your benefits) remains below specific IRS thresholds, your benefits may be completely federal-tax-free. State taxes on Social Security vary widely depending on where you reside.

Can I avoid taxes on my IRA withdrawals entirely?

Traditional IRA withdrawals are universally taxed as ordinary income unless you utilize a Qualified Charitable Distribution (QCD). By transferring the funds directly to a qualified 501(c)(3) charity, the distribution satisfies your RMD without adding a single dollar to your taxable income.

Your Next Move

Do not wait for a surprise tax bill to evaluate your withdrawal strategy. Pull out your most recent tax return, log into your retirement accounts, and identify the specific tax buckets holding your wealth. If your portfolio is overwhelmingly pre-tax, outline a multi-year plan to diversify your tax exposure through calculated Roth conversions or strategic capital gains realization. Taking deliberate action today shields your wealth from invisible leaks, giving you the freedom to enjoy the retirement you earned.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: July 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.