Filing taxes in retirement feels like learning a completely new language where the penalties for misunderstanding the vocabulary are staggering. You might think leaving the workforce simplifies your financial life, but navigating multiple income streams actually increases your risk of unintentional tax evasion. From miscalculating required distributions to hiding income from a seemingly innocent side hustle, innocent mistakes easily trigger audits under strict IRS tax rules. Protecting your nest egg means understanding exactly how the government views your Social Security benefits, pension payouts, and investment withdrawals. By identifying the subtle ways retirees accidentally break tax laws, you can ensure your hard-earned money stays safely in your accounts.

1. Ignoring Income From Your Retirement Side Hustle

Many retirees embrace the gig economy to stay active and supplement their fixed income. Whether you sell handmade furniture, consult for your former employer, or pet-sit for neighbors, the IRS considers this taxable income. A common misconception persists that small amounts of cash or peer-to-peer payments fall below a reporting threshold and remain invisible to the government.

Failing to report this income crosses the line from a simple tax mistake into deliberate tax fraud. The IRS utilizes sophisticated matching systems to track deposits, and third-party payment processors now issue 1099-K forms for relatively small transaction volumes. When you omit this income on your tax return, you willfully misrepresent your earnings.

To maintain flawless tax compliance, track every dollar you earn outside of your traditional retirement accounts. Use dedicated accounting software or a simple spreadsheet to log your side hustle revenue and valid business expenses. Reporting this income accurately protects you from severe audit penalties and back taxes.

2. Miscalculating the Taxability of Social Security Benefits

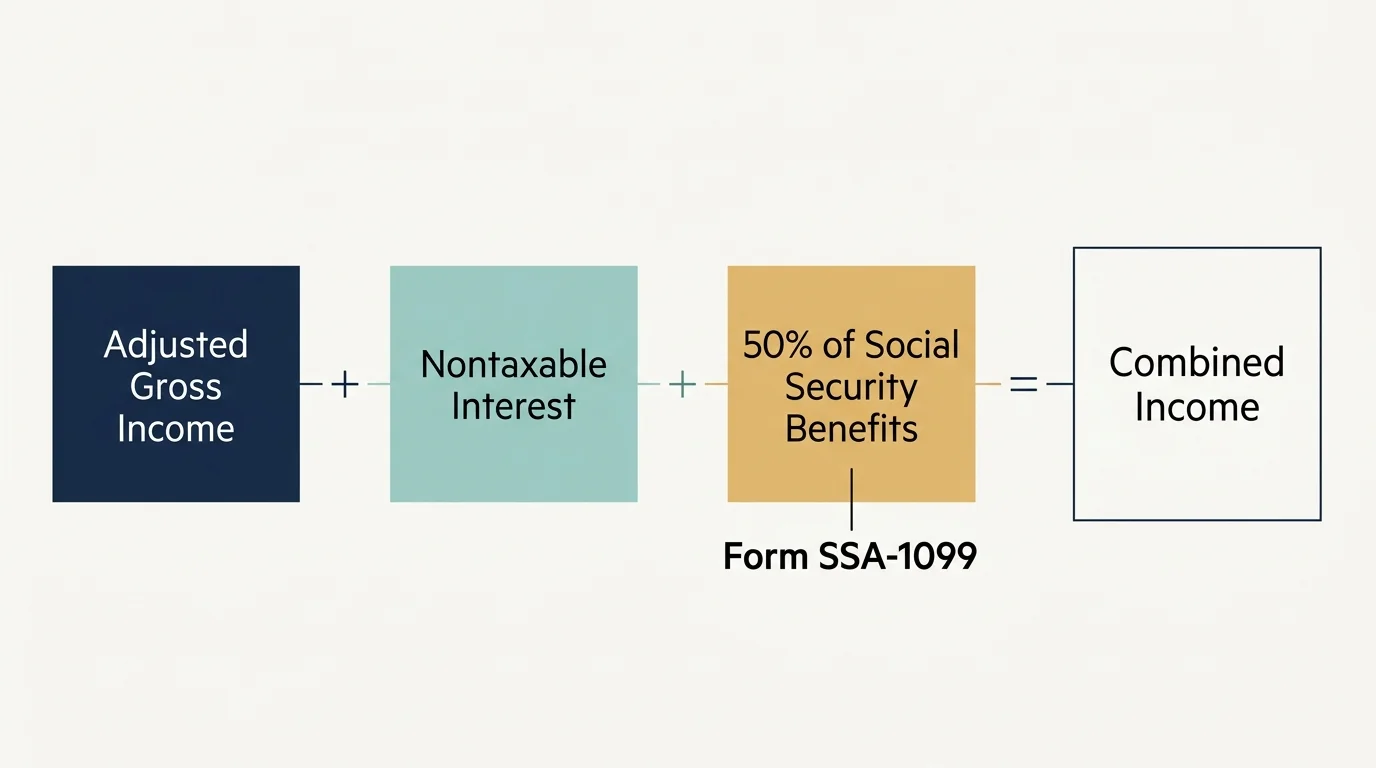

You paid into the Social Security system for decades, leading you to naturally assume your monthly benefits belong entirely to you, tax-free. Unfortunately, depending on your total financial picture, up to 85% of your Social Security benefits could be subject to federal income tax. The government calculates this using a formula known as “combined income,” which adds your adjusted gross income, nontaxable interest, and half of your Social Security benefits.

Retirees often attempt to manipulate their income reporting to stay below the taxation thresholds. Intentionally omitting other income sources—such as capital gains or municipal bond interest—to falsely lower your combined income constitutes tax fraud. The Social Security Administration reports your exact benefit amounts directly to the IRS via Form SSA-1099. Any discrepancy between their records and your tax filing instantly triggers a red flag in the IRS system.

Review your combined income annually, especially before taking large withdrawals from traditional IRAs. Planning your distributions strategically allows you to minimize the tax impact legally, without resorting to dangerous omissions on your return.

3. Mishandling Required Minimum Distributions (RMDs)

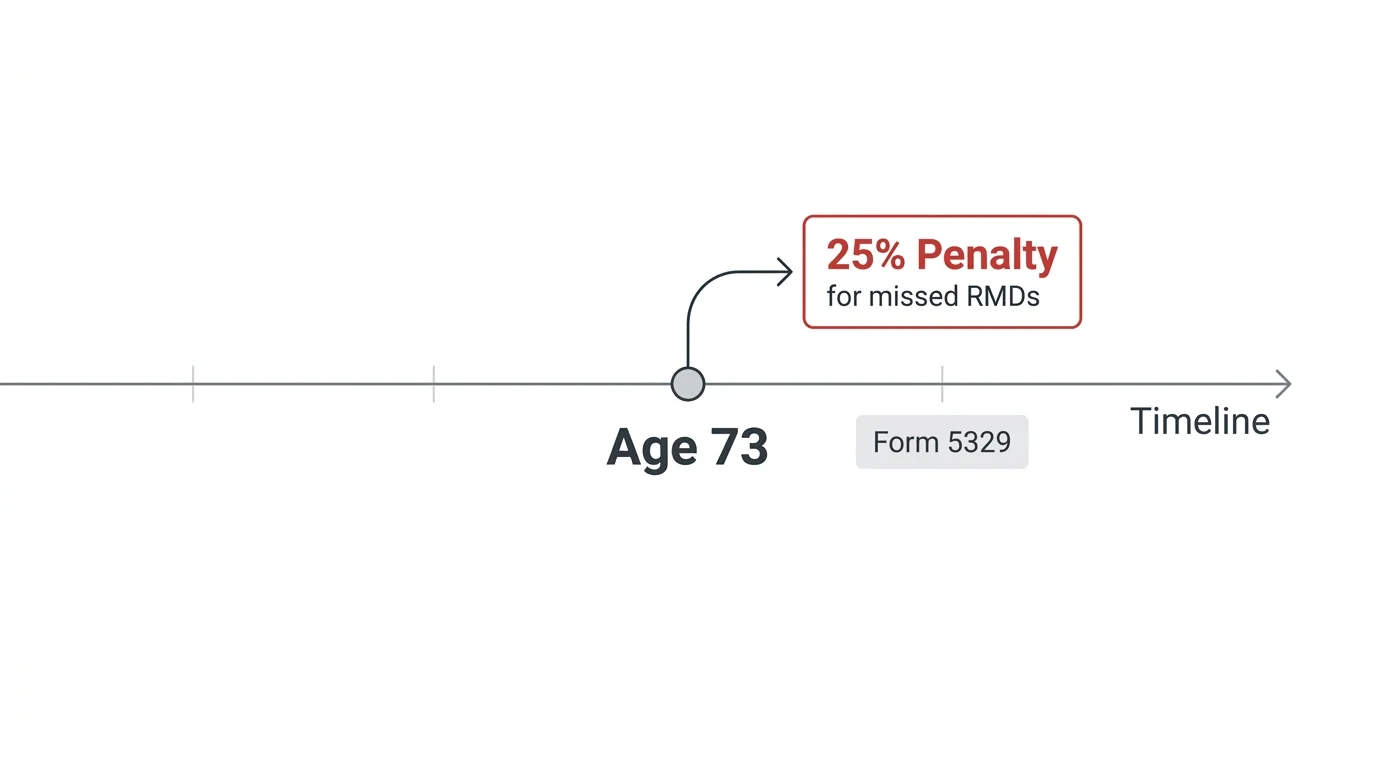

Once you reach age 73, the IRS mandates that you begin withdrawing specific amounts from your traditional IRAs and 401(k)s each year. These Required Minimum Distributions ensure the government finally collects taxes on the money you deferred during your working years. Calculating the exact amount requires using life expectancy tables provided by the IRS, and the penalty for missing an RMD equals a steep 25% of the amount you failed to withdraw.

Tax fraud occurs when retirees realize they missed an RMD and deliberately falsify their tax returns to hide the error. Rather than filing the required Form 5329 to report the shortfall and request a penalty waiver, some individuals simply ignore the mistake and hope the IRS fails to notice. Falsifying forms to cover up missed distributions constitutes intentional evasion.

If you miss an RMD deadline, address it immediately. Take the required distribution, pay the associated taxes, and file the proper paperwork to request leniency. The IRS often waives the penalty for genuine errors if you take prompt corrective action. For detailed calculation worksheets, consult the official IRS Retirement Plans portal.

4. Exaggerating Medical Expense Deductions

Healthcare costs represent one of the largest expenses in retirement, making the medical expense deduction highly attractive. Current tax laws allow you to deduct qualified unreimbursed medical expenses that exceed 7.5% of your adjusted gross income. However, the desperation to cross that high threshold leads many well-meaning retirees to claim ineligible expenses.

Classifying non-qualified expenses as medical necessities directly violates IRS tax rules. You cannot legally deduct over-the-counter vitamins, cosmetic procedures, general gym memberships, or wellness retreats, even if a doctor broadly suggested they would improve your health. Claiming these items as qualified medical deductions requires a specific Letter of Medical Necessity outlining a diagnosed condition.

- Qualified Deductions: Prescription medications, Medicare premiums, dental care, hearing aids, and necessary home modifications for accessibility.

- Fraudulent Deductions: General health supplements, non-prescription reading glasses, elective cosmetic surgeries, and standard fitness equipment.

Maintain meticulous records and strict boundaries regarding your healthcare deductions. Keep all receipts and documentation aligned with the guidelines outlined on Medicare.gov and IRS Publication 502.

5. Fudging State Residency for Tax Benefits

Snowbirds who split their time between multiple states frequently run into trouble with state residency rules. Moving from a high-tax state like New York or California to a state with no income tax like Florida or Texas offers massive financial benefits. However, simply buying a condo in a tax-free state does not legally change your tax domicile.

Claiming primary residency in a tax-free state while actually spending the majority of your year in a high-tax state is a common form of tax fraud. State revenue departments aggressively audit wealthy retirees suspected of faking their residency. Auditors will scrutinize your cell phone location data, EZ-Pass toll records, voter registration, country club memberships, and even where your pet sees the veterinarian.

To establish legitimate residency, you must generally spend more than 183 days in your new state and sever primary ties with your former state. Update your driver’s license, register your vehicles, move your primary banking, and shift your voting registration to demonstrate your true intent to relocate.

6. Neglecting Foreign Account Reporting While Traveling

Retiring abroad or spending extensive time traveling internationally appeals to many older Americans seeking adventure and a lower cost of living. To facilitate daily life overseas, you might open a local bank account to pay rent, buy groceries, or manage foreign investments. The United States demands strict reporting of all global assets.

If the combined value of your foreign financial accounts exceeds $10,000 at any point during the calendar year, you must file a Report of Foreign Bank and Financial Accounts (FBAR). Deliberately hiding offshore assets or failing to report foreign accounts carries devastating consequences. The IRS views unreported offshore money as a prime indicator of tax evasion, regardless of your intentions.

Even if your foreign accounts generate no taxable interest, the reporting requirement remains absolute. Ensure you file your FBAR electronically with the Financial Crimes Enforcement Network (FinCEN) by the annual deadline to protect your international retirement lifestyle.

7. Claiming Ineligible Family Members as Dependents

Retirees frequently step in to provide financial assistance to their families. You might invite a struggling adult child to move back home or pay the tuition for a grandchild’s college education. Naturally, you might assume that providing this level of support entitles you to claim them as a dependent on your tax return.

Claiming a relative as a dependent requires passing strict IRS dependency tests. You must provide more than 50% of their total financial support for the year, including housing, food, medical care, and education. If your adult child earns their own income and provides more than half of their own support, claiming them as a dependent on your taxes is fraudulent.

Misrepresenting your financial relationships to secure higher deductions or favorable tax credits violates federal law. Before listing any family member on your tax return, run through the IRS dependency worksheets to confirm they legally qualify as a qualifying child or qualifying relative.

Errors That Cost Retirees Thousands

Understanding how different income sources face taxation is critical to avoiding costly filing mistakes. Retirees often assume all retirement funds follow the same rules, leading to underpayment penalties and accusations of fraud when the IRS corrects their returns.

Failing to distinguish between taxable and tax-free accounts causes massive headaches during tax season. When you withdraw money from various accounts, you must report them accurately according to their specific tax treatment.

| Income Source | Tax Treatment | Common Filing Mistake |

|---|---|---|

| Traditional IRA / 401(k) | Fully Taxable as Ordinary Income | Assuming withdrawals are capital gains. |

| Roth IRA | Tax-Free (if rules are met) | Accidentally reporting distributions as taxable income. |

| Social Security | Up to 85% Taxable based on Combined Income | Omitting the 1099-SSA entirely from the return. |

| Municipal Bonds | Federal Tax-Free (Usually) | Failing to report the interest for combined income calculations. |

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” — Robert Kiyosaki

When to Get Expert Help

Managing taxes in retirement requires a higher level of scrutiny than during your working years. While commercial tax software handles standard W-2 income beautifully, it often fails to prompt the right questions for complex retirement scenarios. You should strongly consider hiring a Certified Public Accountant (CPA) or a fiduciary financial advisor when you begin claiming Social Security, start taking RMDs, or decide to relocate across state lines.

Seek professional guidance immediately if you realize you have missed an RMD in a previous year or failed to report a foreign bank account. A qualified tax attorney or enrolled agent can help you utilize IRS amnesty programs and voluntary disclosure procedures. Attempting to fix years of accidental omissions on your own usually compounds the problem and increases your risk of triggering an aggressive audit.

Frequently Asked Questions

Can I go to jail for an accidental tax mistake?

No. The IRS distinguishes between genuine errors (negligence) and intentional deception (fraud). Accidental mistakes usually result in requests for clarification, back taxes owed, and potential financial penalties. Criminal charges and jail time are reserved for individuals who establish a clear pattern of willful tax evasion, hiding assets, or falsifying documents.

Do I have to report cash gifts from my children on my tax return?

No. Cash gifts received from family members do not count as taxable income for the recipient. You do not need to report these gifts on your federal income tax return. The person giving the gift is responsible for filing a gift tax return if the amount exceeds the annual exclusion limit.

How does the IRS know about my retirement account withdrawals?

Financial institutions are legally required to report your withdrawals directly to the government. Whenever you take a distribution from a traditional IRA, 401(k), or pension, the custodian generates a Form 1099-R. They send one copy to you and one copy directly to the IRS. If you fail to report this income on your tax return, the IRS computer system automatically flags the discrepancy.

Are my Medicare premiums tax-deductible?

Yes, Medicare Part B and Part D premiums qualify as deductible medical expenses. However, you can only deduct them if you itemize your deductions and your total qualified medical expenses exceed 7.5% of your adjusted gross income. If you take the standard deduction, you cannot separately deduct your Medicare premiums.

Protecting Your Peace of Mind

Your retirement years should focus on travel, family, and relaxation, not stressing over potential IRS audits. Maintaining strict tax compliance requires diligence, organization, and a willingness to adapt to evolving tax laws. Take the time this week to review your current tax strategy, double-check your dependency claims, and organize the records for any side-hustle income you generate.

By proactively addressing these common pitfalls, you shield your retirement savings from unnecessary penalties and keep your financial future secure. Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: July 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.