You might be staring at your portfolio wondering if you need to work another five years, but the math could already be in your favor. Many Americans overestimate the wealth required to step away from their careers by focusing on an arbitrary target number instead of actual cash flow. True retirement readiness involves examining how your debt, healthcare coverage, and guaranteed income streams align to cover your living expenses. If your mortgage is gone, your emergency fund is fully stocked, and you possess a clear strategy for bridging the healthcare gap before Medicare kicks in, you are likely positioned to leave the workforce today. Discover the concrete financial indicators signaling your early retirement dream is already a practical reality.

1. Your Debt Is Eliminated or Highly Manageable

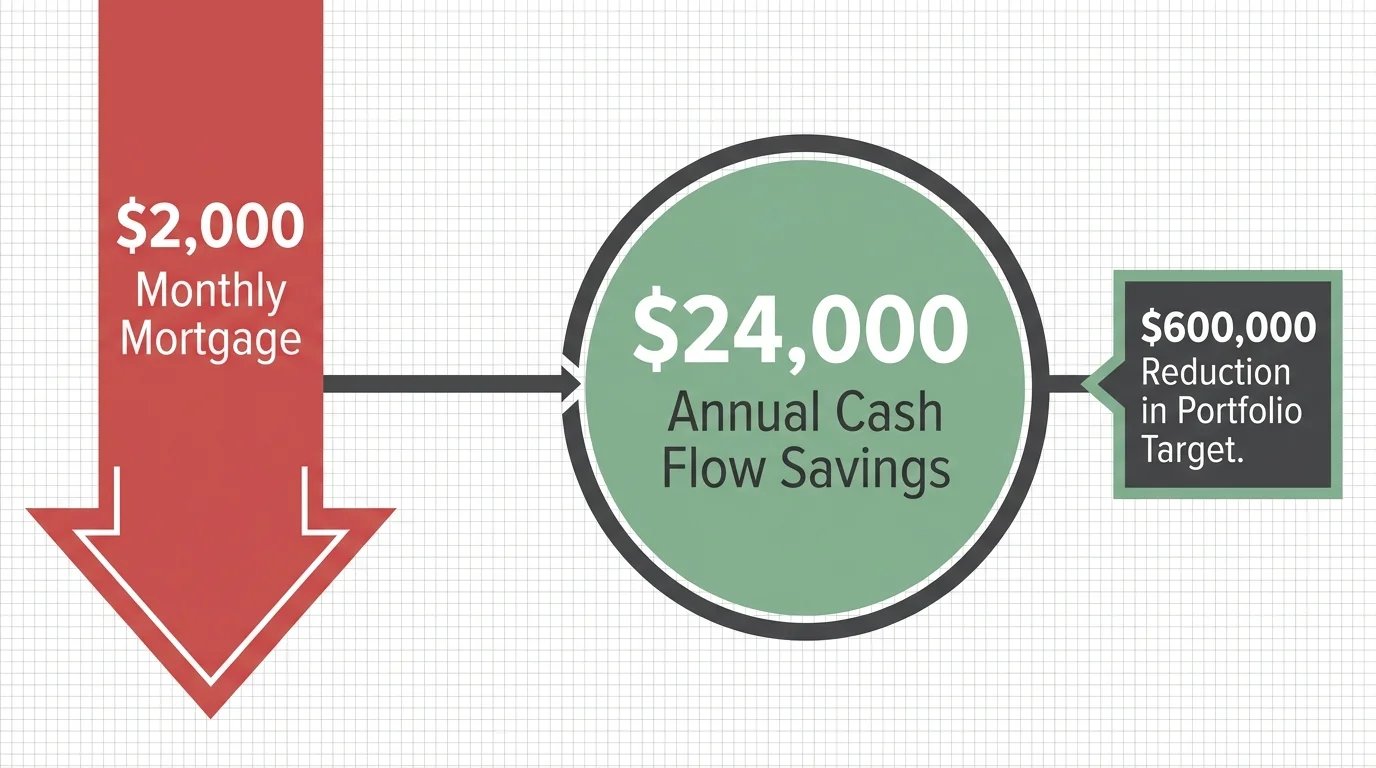

Entering retirement with significant debt acts as a severe drag on your fixed income, forcing you to pull more money from your investment accounts than you otherwise would. If you have systematically eliminated your high-interest consumer debt, auto loans, and your primary mortgage, your required monthly income drops dramatically.

Consider the math behind a paid-off home. If you eliminate a $2,000 monthly mortgage payment before leaving the workforce, you reduce your annual cash flow requirement by $24,000. Using the traditional 4% withdrawal rule as a benchmark, that $24,000 reduction means you need roughly $600,000 less in your investment portfolio to sustain your lifestyle. When your baseline living expenses are low, your retirement savings instantly become vastly more powerful, allowing you to retire years ahead of your original schedule.

2. You Have a Concrete Plan for Healthcare Before Medicare

The single largest barrier to early retirement for Americans is the healthcare gap—the years between leaving an employer-sponsored health plan and reaching age 65, when you finally qualify for federal health benefits. If you have a fully researched, viable strategy to cover your medical needs during this gap, you hold a massive advantage.

Effective strategies for bridging this gap include jumping onto a younger working spouse’s employer plan, utilizing COBRA benefits for up to 18 months, or purchasing a comprehensive policy through the Affordable Care Act (ACA) marketplace. Careful management of your taxable income during these early retirement years can even help you qualify for substantial ACA premium subsidies. Once you reach the appropriate age, you can transition smoothly into federal coverage; you can research the exact timeline and requirements at Medicare.gov. Having this transition mapped out removes the most unpredictable financial variable from your early retirement timeline.

3. Your Social Security Strategy Is Optimized for Your Lifespan

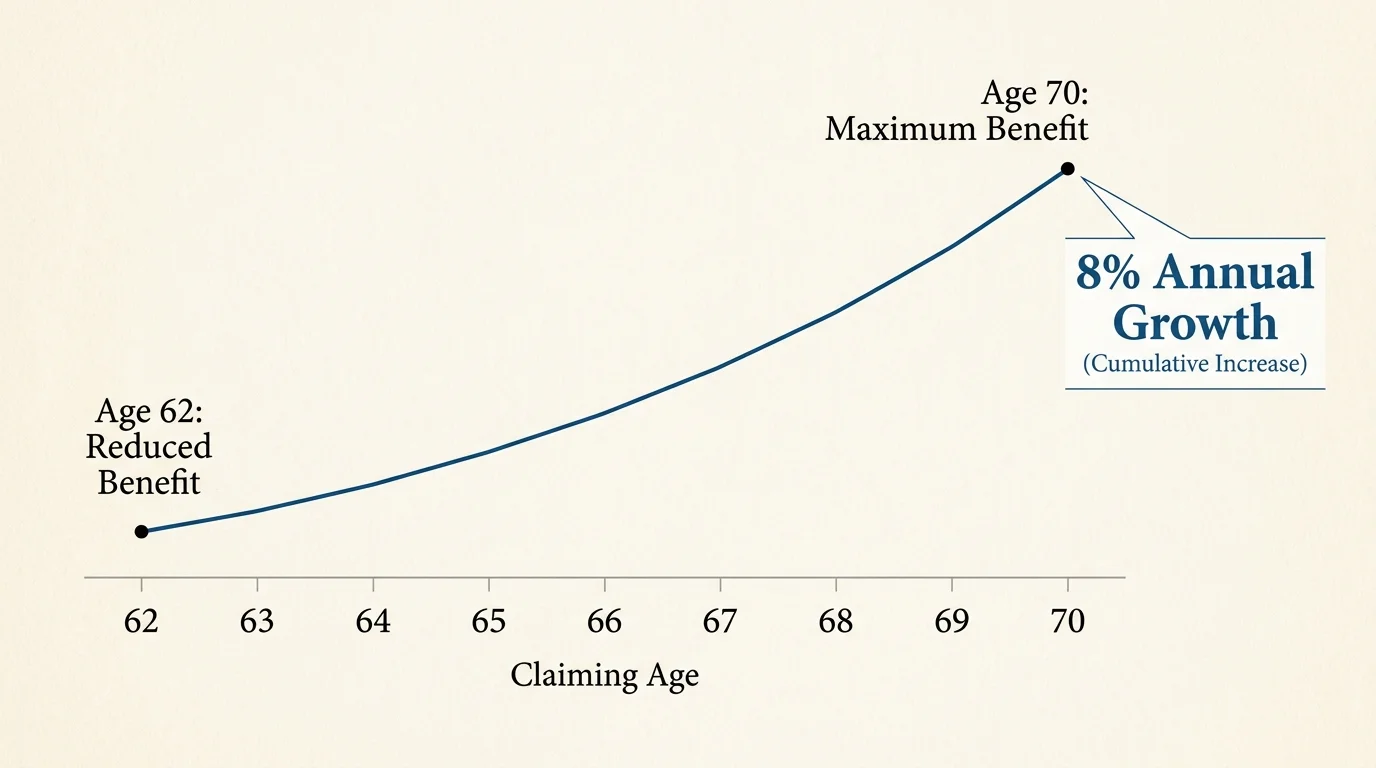

Many pre-retirees mistakenly assume they must claim Social Security immediately upon stopping work. If you understand how to separate the decision to retire from the decision to claim benefits, you demonstrate high-level financial readiness. Funding your initial retirement years through personal savings or part-time income allows your future Social Security benefits to grow substantially.

Your benefit amount hinges permanently on the age at which you file. Claiming before your Full Retirement Age (FRA) locks in a reduced monthly check for life, while delaying past your FRA earns you delayed retirement credits of 8% per year until age 70. You can utilize the Social Security Retirement Estimator to verify your specific numbers.

| Claiming Age | Percentage of FRA Benefit | Estimated Monthly Benefit | Strategic Considerations |

|---|---|---|---|

| Age 62 | 70% | $1,400 | Permanent reduction; best if health is poor or funds are critically needed. |

| Age 67 (FRA) | 100% | $2,000 | Standard baseline; allows you to earn unlimited outside income without penalty. |

| Age 70 | 124% | $2,480 | Maximum possible payout; ideal for longevity protection and surviving spouses. |

4. Your Withdrawal Rate Survives Stress Testing

It is easy to feel wealthy during a long bull market, but true early retirement readiness requires knowing your portfolio can survive a severe economic downturn. If you have run your numbers through Monte Carlo simulations—statistical models that test your portfolio against thousands of randomized market scenarios—and maintain a high probability of success, you are on solid ground.

Financial planners often reference a dynamic withdrawal strategy rather than a rigid, fixed percentage. Being financially ready means you understand you may need to withdraw 4% during prosperous years but temporarily tighten your belt to 3% during a bear market. If your baseline essential expenses can be met even at a highly conservative withdrawal rate, market volatility will not force you back into the labor market.

5. You Have Built a Two-Year Cash Buffer

One of the deadliest threats to an early retirement portfolio is sequence of returns risk—experiencing a severe market crash in the first few years of your retirement. When you sell equities during a market downturn to buy groceries and pay utilities, those shares are permanently gone; they cannot recover when the market inevitably rebounds.

You are ready to retire if you have insulated your portfolio by building a robust cash buffer. Maintaining 18 to 24 months of essential living expenses in highly liquid, low-risk vehicles—such as high-yield savings accounts, money market funds, or short-term Certificates of Deposit (CDs)—ensures you never have to sell stocks at a loss to fund your daily life. This cash wedge gives your equity investments the time they need to weather economic storms.

6. Your Post-Retirement Budget Is Based on Actual Tracking

Guessing your future expenses leads directly to financial anxiety. You are ready to retire early when your budget is built on documented spending habits rather than vague estimations. Successful early retirees know exactly what they spend on utilities, food, property taxes, and insurance because they have tracked it meticulously for years.

Furthermore, you recognize the “retirement smile” spending curve. You have budgeted for higher discretionary spending in your early, active years (travel, hobbies, home renovations), lower spending in your middle years as you settle into a routine, and potentially higher costs in your later years due to long-term care or medical needs. Anticipating these shifts rather than assuming a flat expense rate demonstrates deep financial maturity.

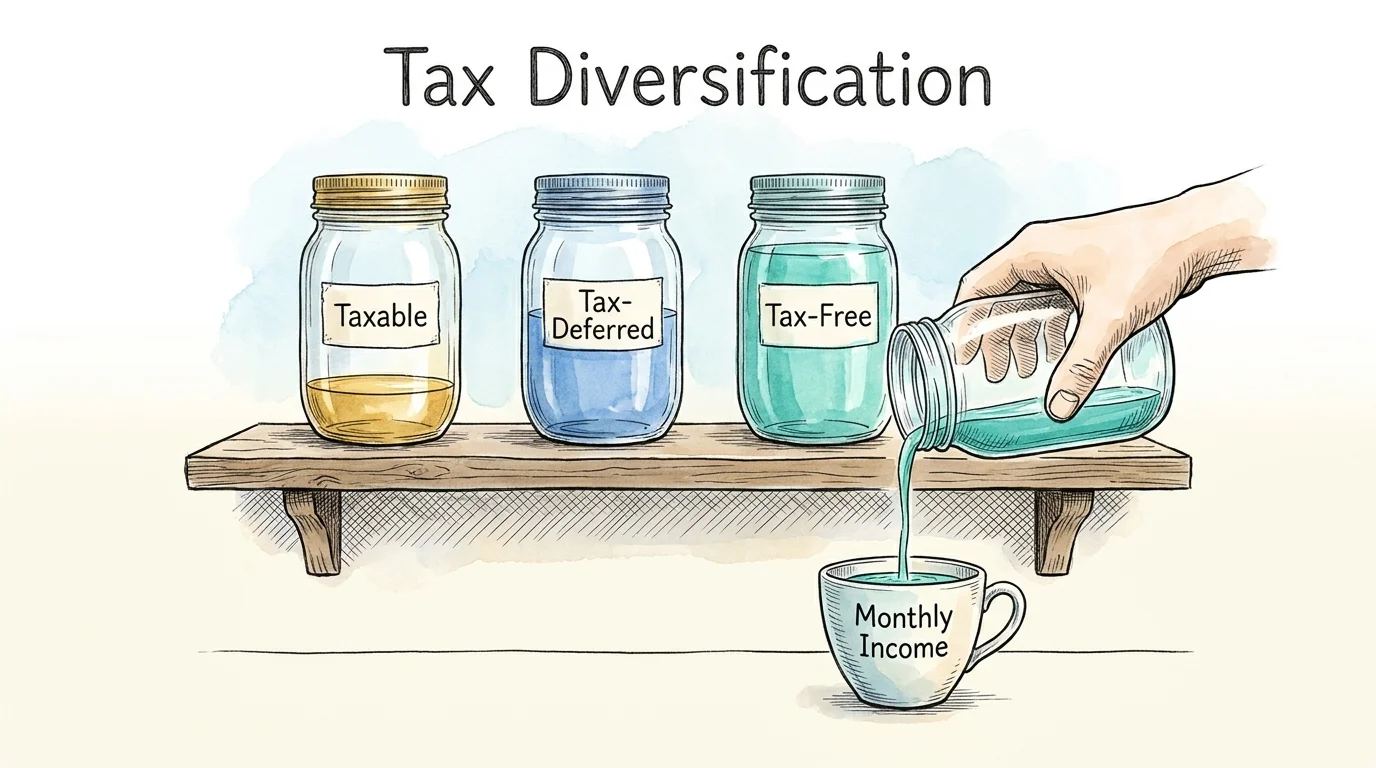

7. You Understand the Tax Implications of Your Withdrawals

It is not just about how much money you have saved; it is about how much of that money the IRS lets you keep. Early retirees face a complex tax landscape, but those who are prepared understand how to navigate different tax buckets. By utilizing a mix of taxable brokerage accounts, tax-deferred accounts (Traditional IRAs and 401k plans), and tax-free accounts (Roth IRAs), you can carefully control your taxable income each year.

Managing these withdrawals strategically can keep you in lower tax brackets, reduce capital gains taxes, and optimize your eligibility for healthcare subsidies. For thorough breakdowns of how distributions from different accounts are taxed, reviewing the guidelines provided by IRS Retirement Plans is a crucial step in formalizing your exit strategy.

8. You Are Emotionally and Socially Prepared for the Transition

Financial readiness is only half the equation; emotional readiness sustains you once the novelty of sleeping in wears off. Many driven professionals leave their careers only to find themselves grappling with a sudden loss of identity, purpose, and daily social interaction.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

You are truly ready to leave the workforce when you have a structured plan for your time. This means cultivating hobbies that challenge you, scheduling regular social engagements outside of your old professional network, and finding new avenues for intellectual stimulation, whether through volunteering, mentoring, or part-time passion projects. Having a clear vision for your daily life prevents the emotional decline that frequently accompanies a poorly planned exit.

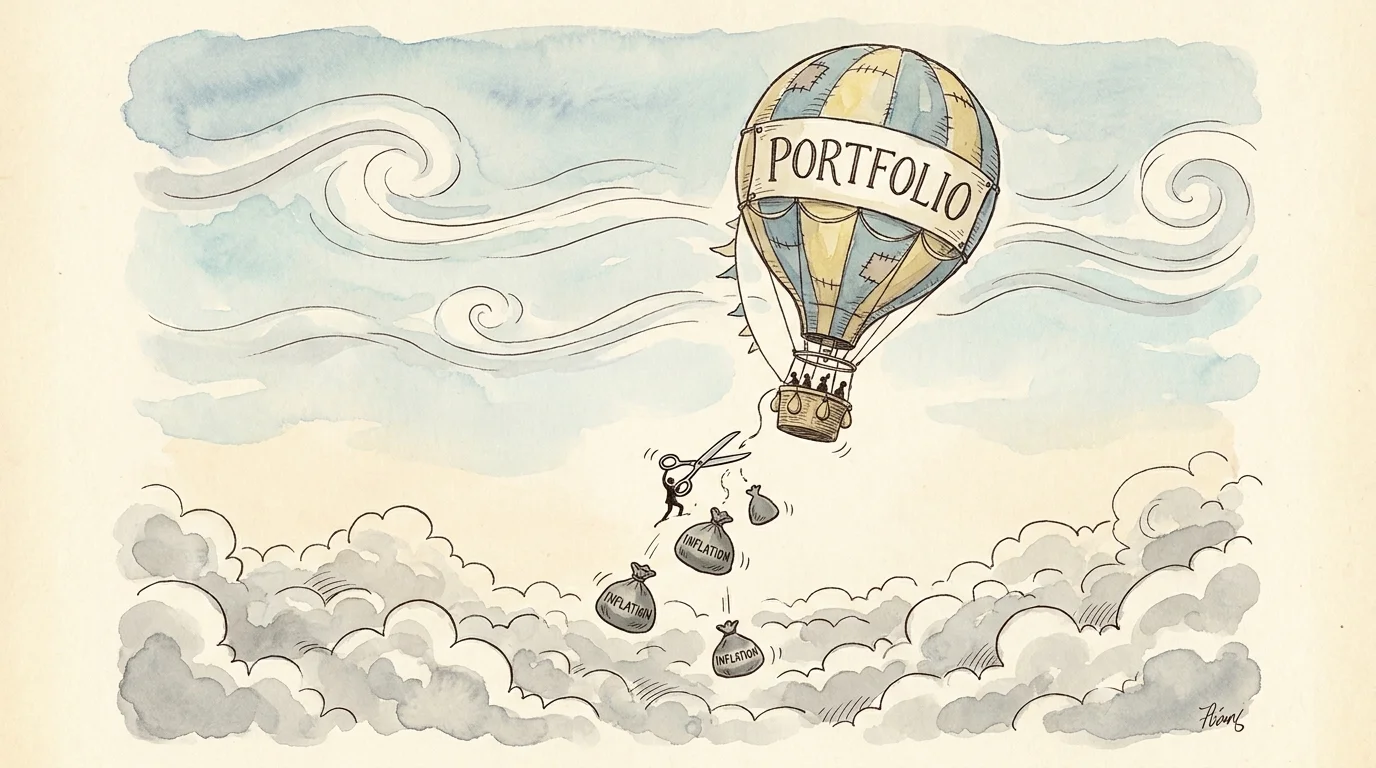

9. Your Portfolio Outpaces Inflation Without Excessive Risk

Retiring early means your savings must support you for 30 or even 40 years. Over that timeframe, inflation is a silent portfolio killer. If inflation averages just 3% annually, the cost of your living expenses will double in roughly 24 years. You cannot simply move your entire nest egg into cash or treasury bonds when you retire at 55; the loss of purchasing power will devastate your standard of living.

You show readiness when your asset allocation balances the need for immediate capital preservation with the necessity of long-term growth. Maintaining a sensible exposure to diversified equities ensures your portfolio generates the returns necessary to outpace the rising costs of food, fuel, and healthcare over the next three decades.

Errors That Cost Retirees Thousands

Even with excellent preparation, stumbling into common administrative or strategic traps can severely damage your early retirement timeline. Avoid these frequent missteps:

- Ignoring the Social Security Earnings Test: If you claim Social Security early (e.g., at age 62) but decide to take on part-time consulting work, the SSA will withhold $1 in benefits for every $2 you earn above an annual limit ($23,400 in 2026). Many early retirees lose thousands because they fail to realize their side income temporarily disqualifies them from receiving their full benefit.

- Miscalculating Medicare Surcharges (IRMAA): If you execute massive Roth conversions or sell significant real estate after turning 63, you might inadvertently spike your Modified Adjusted Gross Income (MAGI). This triggers the Income-Related Monthly Adjustment Amount (IRMAA), forcing you to pay hundreds of dollars more each month for Medicare Part B and Part D premiums two years later.

- Failing to Plan for Long-Term Care: Medicare does not cover custodial care, such as nursing home stays or daily living assistance. Assuming standard health insurance will cover cognitive decline or mobility issues leaves your portfolio dangerously exposed to sudden, massive medical bills late in life.

- Underestimating the Cost of Home Maintenance: Aging in place requires funds. Retirees often forget to budget for replacing a roof, updating an HVAC system, or retrofitting a home for mobility issues. Plan for an annualized home maintenance cost of roughly 1% to 2% of your property’s value.

When to Get Expert Help

You do not have to navigate the transition into early retirement alone. The complexity of tax codes, healthcare regulations, and investment withdrawal strategies often warrants professional oversight. Consider assembling a team of experts well before your target retirement date.

A fee-only, fiduciary financial advisor can stress-test your portfolio and optimize your withdrawal sequence to minimize your lifetime tax burden. For objective guidance on healthcare transitions, reach out to your local State Health Insurance Assistance Program (SHIP); their counselors provide free, unbiased assistance to help you understand Medicare enrollment periods and plan differences. Additionally, consulting an elder law attorney ensures your estate planning documents—such as durable powers of attorney and healthcare directives—are fully updated. For a comprehensive overview of financial rights and protections as you age, the Consumer Financial Protection Bureau (CFPB) offers excellent independent resources to help you protect your nest egg.

Frequently Asked Questions About Retiring Early

What is the Rule of 55 for early retirement?

The Rule of 55 is an IRS provision allowing workers who leave their job in or after the year they turn 55 to take distributions from their current employer’s 401(k) or 403(b) plan without facing the standard 10% early withdrawal penalty. However, this rule only applies to the plan associated with the job you just left, not to previous employers’ plans or your IRAs.

How much of my current income will I need in retirement?

Financial planners traditionally suggest aiming to replace 70% to 80% of your pre-retirement income. However, early retirees often find their actual needs depend heavily on their debt load. If your mortgage is paid off, you are no longer saving for retirement, and your commuting costs disappear, you might comfortably maintain your lifestyle on 50% to 60% of your previous gross income.

Can I get Medicare if I retire at 60?

No, standard Medicare eligibility begins at age 65. If you retire at 60, you must secure private health insurance—often through the ACA marketplace, COBRA, or a spouse’s employer—to bridge the five-year gap until your federal Medicare benefits activate.

How does early retirement affect my Social Security benefits?

Your Social Security benefit is calculated using your 35 highest-earning years. If you retire early and have fewer than 35 years of earnings, the Social Security Administration will factor in zeros for the missing years, which permanently lowers your baseline benefit. Furthermore, claiming the benefit before your Full Retirement Age results in an additional permanent percentage reduction.

Transitioning into retirement early is entirely achievable when you shift your focus away from a single, intimidating portfolio number and concentrate on controlling your variables. Take the time this week to run a fresh calculation of your baseline living expenses without your mortgage and commuting costs. The resulting number might prove that your financial independence date is much closer than you dared to hope.

Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.