Losing a spouse is an immense emotional shock, and the abrupt shift in your household income only compounds the stress. When your partner passes away, your combined Social Security income changes immediately. The fundamental rule of Social Security survivor benefits dictates that a surviving spouse gets to keep the larger of the two monthly checks, while the smaller payment disappears forever. Understanding exactly how this calculation works, what age restrictions apply, and when you can switch between your own retirement record and your survivor benefits will protect your financial security during a vulnerable transition. This guide delivers the concrete steps you must take to claim your widow or widower benefits and avoid permanent payout reductions.

The Core Rule: Keeping the Highest Check

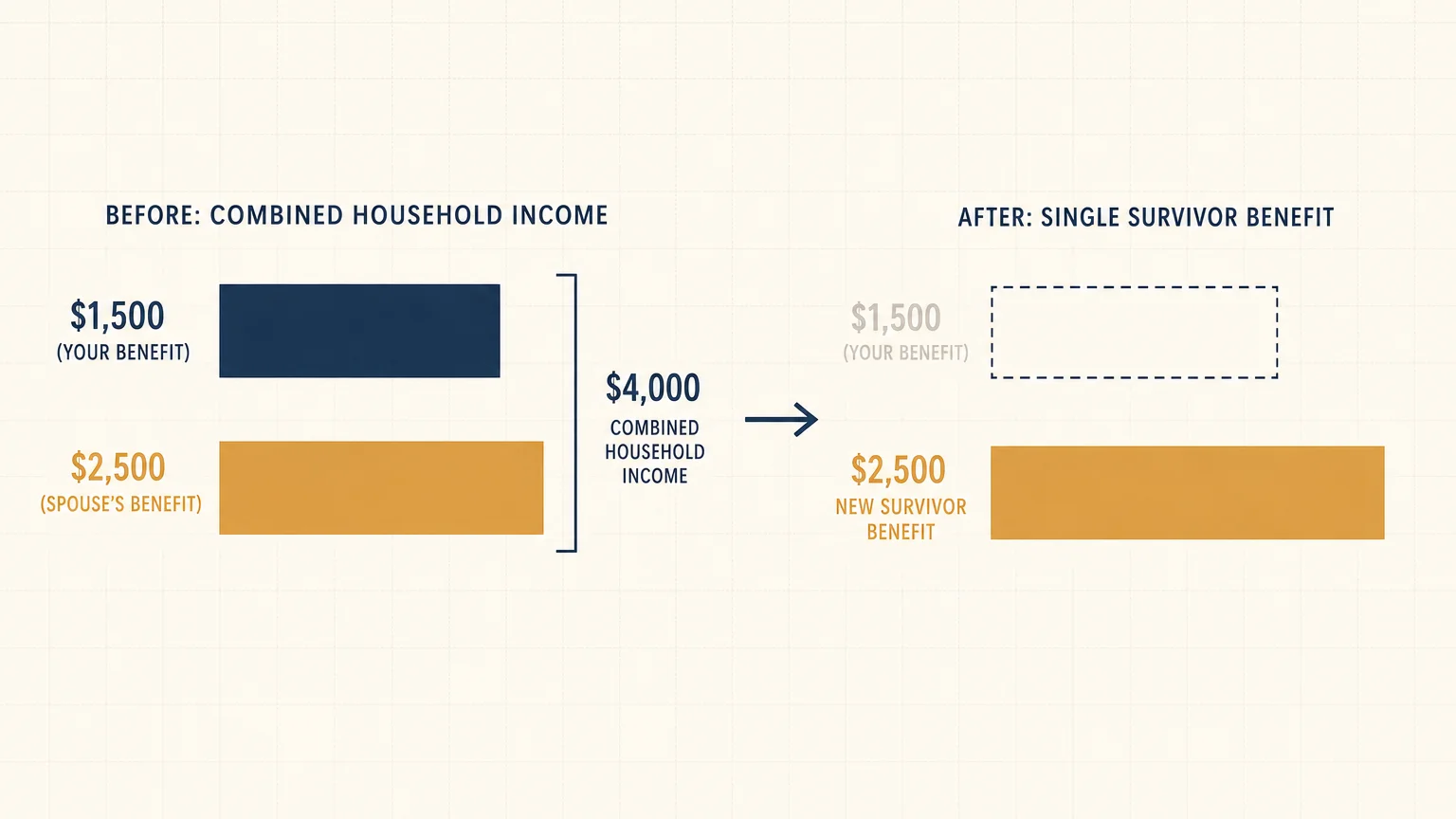

The Social Security Administration (SSA) enforces a straightforward but consequential rule when a married beneficiary dies. You do not get to keep both your Social Security check and your deceased spouse’s check. Instead, you inherit the higher of the two benefit amounts.

Consider a scenario where you receive $1,500 per month based on your earnings record, and your spouse receives $2,500. If your spouse passes away, your $1,500 payment ends. You step up to receive the $2,500 payment as your survivor benefit. Your household income drops from $4,000 to $2,500 instantly.

Financial planners often refer to this drop in income as the “widow’s penalty.” While your household income decreases drastically—sometimes by up to 50%—your household expenses rarely drop by the same margin. Property taxes, home maintenance, and utility bills remain largely unchanged. Furthermore, your tax filing status shifts from Married Filing Jointly to Single, which can push your remaining income into a higher tax bracket. Planning for this inevitable reduction in income is a cornerstone of robust retirement preparation.

“The best time to plan for retirement was 20 years ago. The second best time is today.”

How Your Age Impacts Your Survivor Payment

Just like standard retirement benefits, the age at which you claim survivor benefits dictates the monthly amount you receive. However, the timeline for survivor benefits operates differently than standard spousal or individual benefits.

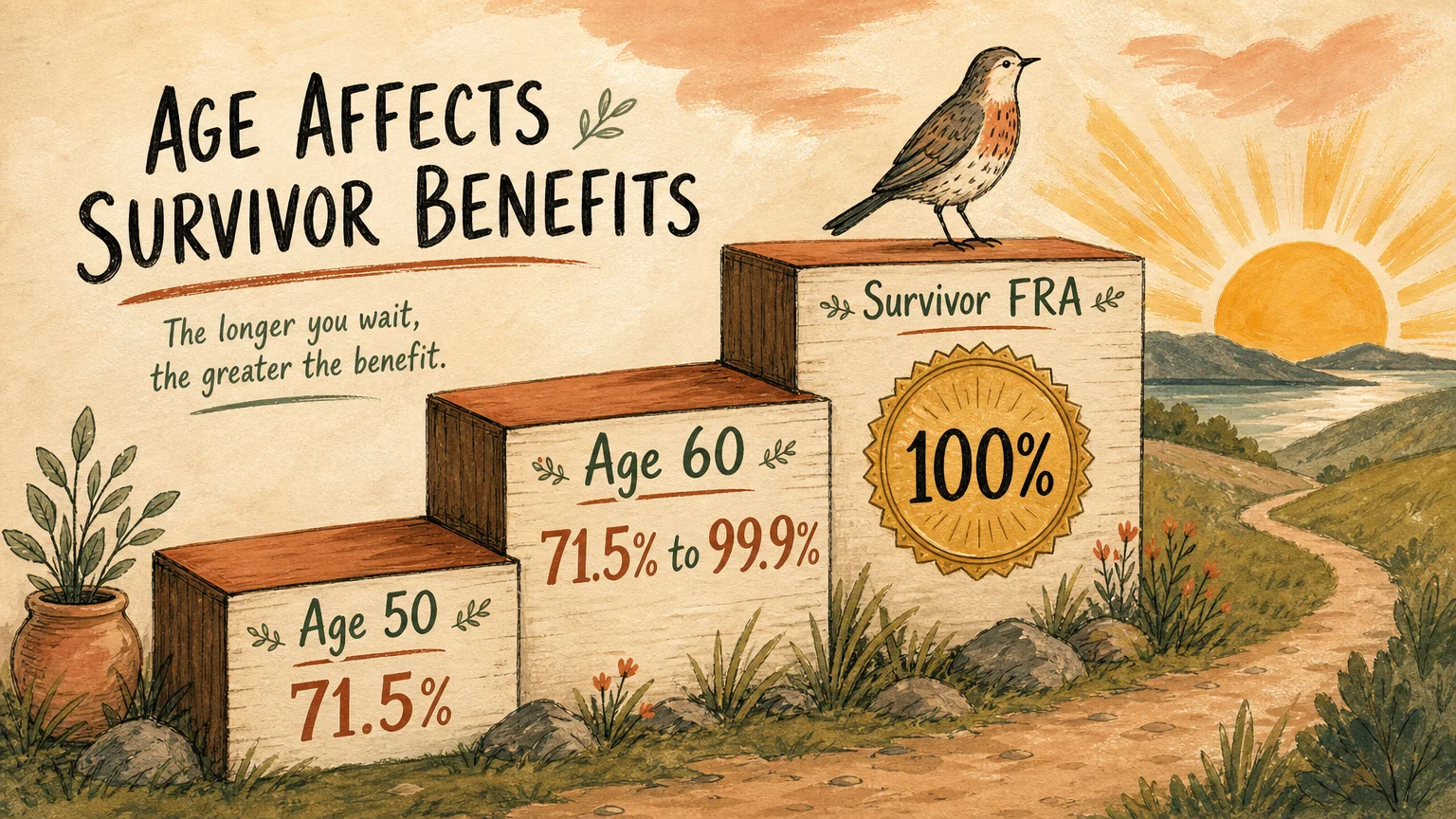

You can claim Social Security survivor benefits as early as age 60, or age 50 if you have a qualifying disability. Taking benefits before your designated Survivor Full Retirement Age (FRA) results in a permanent reduction to your monthly check. It is important to note that your Survivor FRA might differ slightly from your standard retirement FRA depending on your birth year.

| Claiming Age | Percentage of Deceased Spouse’s Benefit Received |

|---|---|

| Survivor Full Retirement Age (Typically 66 to 67) | 100% of the deceased spouse’s benefit |

| Age 60 to Survivor FRA | Pro-rated amount between 71.5% and 99.9% |

| Age 50 to 59 (If disabled) | 71.5% of the deceased spouse’s benefit |

| Any age (Caring for a child under 16 or disabled) | 75% of the deceased spouse’s benefit |

If your deceased spouse delayed claiming their own Social Security until age 70, they locked in delayed retirement credits. As a surviving spouse, you inherit those delayed credits. If you wait until your Survivor FRA to claim, you will receive the fully maximized amount your spouse was receiving (or was entitled to receive) at the time of their death.

Advanced Switching Strategies: Maximizing Your Payments

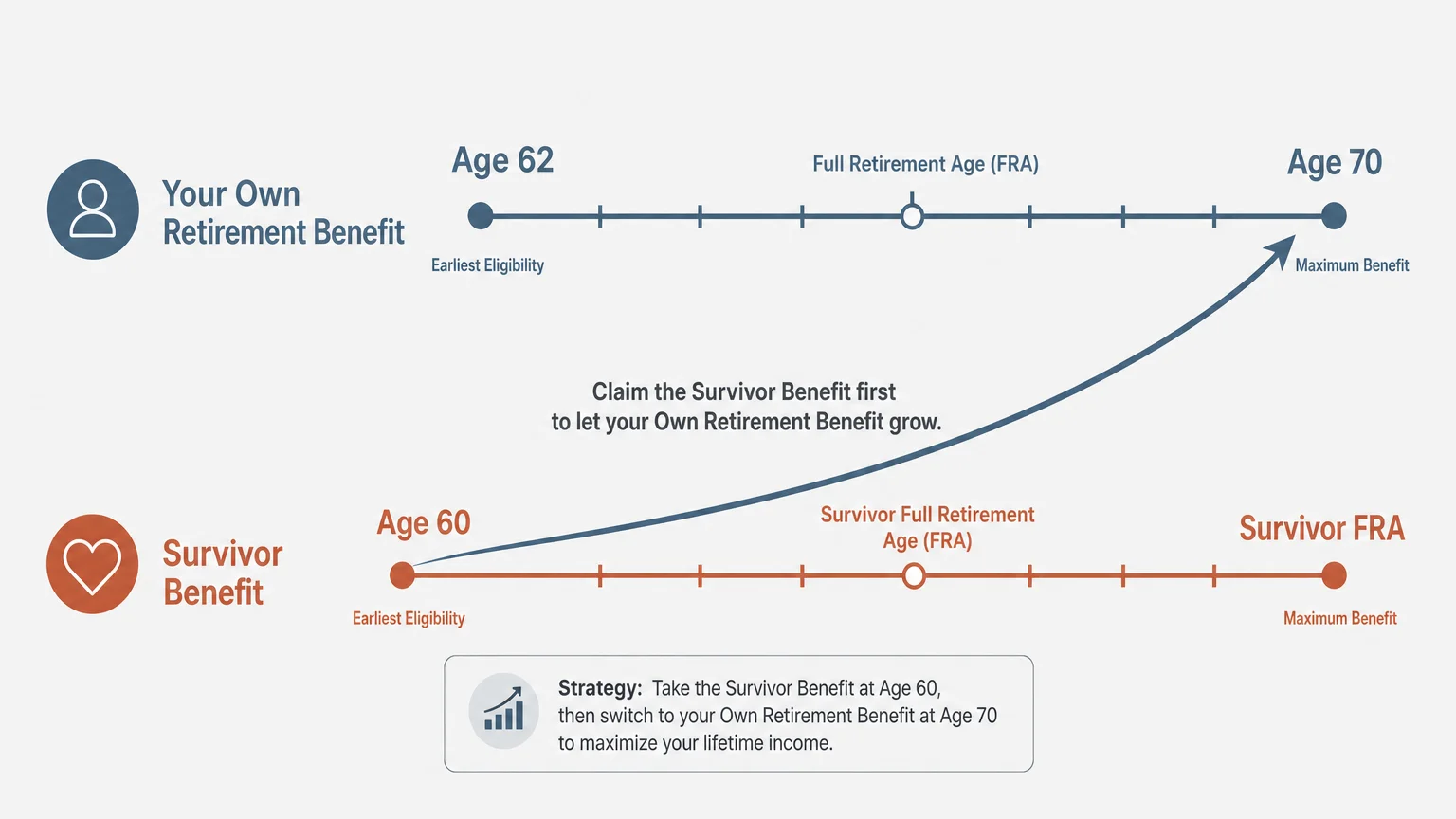

One of the most powerful and underutilized tools in the Social Security system is the ability to strategically switch between your own retirement benefit and your survivor benefit. Unlike standard spousal benefits—which force you to file for all available benefits at once under the “deemed filing” rule—survivor benefits remain completely separate.

This separation allows you to sequence your claims to maximize your lifetime income.

- Strategy 1: Claim Survivor Benefits First. You can claim a reduced survivor benefit at age 60. Meanwhile, you allow your own personal retirement benefit to accrue delayed retirement credits until it maxes out at age 70. At age 70, you contact the SSA and switch to your own record if it yields a higher monthly payment.

- Strategy 2: Claim Your Own Benefits First. If you retire early at age 62, you can claim your own reduced retirement benefit. You let your survivor benefit grow until it reaches its maximum value at your Survivor FRA, at which point you switch over to the higher survivor benefit. Note that survivor benefits do not earn delayed retirement credits past your Survivor FRA, so there is no financial advantage to delaying a survivor claim beyond that point.

Executing the right sequence requires running a break-even analysis based on your health, life expectancy, and financial needs. Comparing your options using tools from the National Council on Aging (NCOA) can provide valuable clarity.

What Happens If You Are a Surviving Divorced Spouse?

Divorce does not necessarily terminate your right to survivor benefits. You can collect benefits on your deceased ex-spouse’s record if you meet specific criteria established by the SSA.

To qualify as a surviving divorced spouse, your marriage must have lasted for at least 10 consecutive years. Additionally, you must currently be unmarried, or if you did remarry, that subsequent marriage must have occurred after you turned 60 (or 50 if disabled). If you remarry before age 60, you forfeit the right to claim survivor benefits on your deceased ex-spouse’s record unless that subsequent marriage ends.

Claiming survivor benefits on an ex-spouse’s record does not affect the benefits of their current surviving widow or widower. The SSA pays your claim from a separate pool, and the current spouse will never know you filed the claim.

Errors That Cost Retirees Thousands

Navigating the paperwork and administrative rules following a death is exhausting, but administrative missteps can trigger massive financial headaches. Protect yourself by avoiding these prevalent mistakes.

Cashing the Final Social Security Check

Social Security pays benefits in arrears. The check you receive in June covers the month of May. Crucially, the SSA requires an individual to live through the entire month to be eligible for that month’s benefit. If your spouse dies on May 30, they are not entitled to the benefit paid in June.

If the SSA deposits your deceased spouse’s final payment into a joint bank account, do not spend it. The SSA will eventually flag the death and automatically reverse the direct deposit. If you have already spent the funds or closed the account, the SSA will issue an overpayment notice and demand immediate repayment, often withholding your own benefits until the debt clears.

Failing to Report the Death Promptly

Typically, the funeral director reports the death to the SSA by submitting the deceased’s Social Security number. However, you should never assume this task is completed. Take the initiative to call your local Social Security office to confirm they have registered the death. Delaying this notification leads to overpayments and delays in processing your survivor benefits.

Missing the $255 Lump-Sum Death Benefit

The SSA provides a one-time lump-sum death payment of $255 to a surviving spouse who was living with the deceased at the time of death. While $255 does not cover modern funeral expenses, it is money you are rightfully owed. You must actively apply for this payment within two years of the date of death; the SSA does not send it automatically.

“The goal of retirement is to live off your assets—not live off your regrets.”

When to Get Expert Help

Because survivor benefit calculations interact closely with your broader financial plan, tax obligations, and Medicare premiums, consulting a professional often yields a high return on investment. Do not hesitate to seek expert guidance in the following scenarios:

- You are still working: If you claim survivor benefits before your FRA while continuing to work, you become subject to the Social Security earnings test. Earning over the annual limit will cause the SSA to withhold a portion of your benefits. A financial advisor can help you determine if claiming early makes sense based on your current salary.

- You receive a government pension: If you worked a government job where you did not pay into Social Security (such as certain teaching or municipal roles), the Government Pension Offset (GPO) could drastically reduce or completely eliminate your survivor benefits. An elder law attorney or specialized financial planner can help you navigate GPO calculations.

- You need to transition Medicare coverage: Income shifts after a spouse’s death can impact your Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amounts (IRMAA). A Medicare.gov counselor or a local State Health Insurance Assistance Program (SHIP) representative can assist you in filing an appeal to lower your premiums based on a life-changing event.

Immediate Steps to Claim Your Survivor Benefits

When you are ready to claim your benefits, the process requires gathering specific documentation and speaking directly with an SSA representative. Survivor benefits cannot currently be processed entirely online.

- Gather your documents: Locate your spouse’s death certificate (request multiple original copies from the funeral director), your marriage certificate, your birth certificate, and your spouse’s Social Security number.

- Call the SSA: Reach out to the Social Security Administration at 1-800-772-1213 to schedule an appointment. You can conduct this appointment over the phone or in person at your local SSA field office.

- Request a break-even analysis: During your appointment, ask the SSA representative to show you the exact payout amounts for claiming your survivor benefit now versus delaying it. Verify the figures for switching strategies if you also have your own earnings record.

- Update your bank information: Ensure the SSA has your correct individual routing and account numbers for future direct deposits, separate from any frozen or closed joint accounts.

Frequently Asked Questions About Survivor Benefits

Can I apply for Social Security survivor benefits online?

No. While you can apply for standard retirement or disability benefits online, the SSA requires you to apply for survivor benefits by phone or in person at a local office. This ensures the representative can verify your marriage and death certificates and discuss complex switching strategies.

How long does it take the SSA to process survivor benefits?

Processing times vary by field office, but typically take 30 to 60 days from the date of your application. Ensure you provide all requested original documents promptly to prevent administrative bottlenecks.

What if my spouse died before claiming their Social Security?

If your spouse died before filing for benefits, your survivor benefit is calculated based on the amount they earned up to the time of their death. If they died after reaching their Full Retirement Age but had not yet claimed, you will inherit the delayed retirement credits they accumulated up to their date of death.

Are Social Security survivor benefits taxable?

Yes, survivor benefits are subject to the same tax rules as standard Social Security benefits. Depending on your combined income (your adjusted gross income plus non-taxable interest plus half of your Social Security benefits), up to 85% of your survivor benefits may be subject to federal income tax.

Protecting Your Financial Future

Losing a partner forces you to navigate grief while simultaneously acting as your own chief financial officer. The rules surrounding Social Security survivor benefits are complex, but mastering them ensures you capture every dollar your spouse worked a lifetime to secure for your protection. Take the time to map out your claiming strategy, avoid the trap of cashing the final joint check, and leverage the ability to switch between benefit records to maximize your lifetime income.

Your most vital next step is to log into your personal “my Social Security” account online, review your own earnings statements, and schedule a consultation with a fiduciary advisor or SSA representative to lock in your strategy.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Medicare rules, Social Security benefits, and tax laws change regularly—verify current details at Medicare.gov, SSA.gov, or with a licensed professional.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.