Retiring is often framed as crossing a finish line, but the reality of leaving your career usually looks entirely different than the brochures suggest. You spend decades saving and anticipating a life of endless leisure, only to find that your actual day-to-day experience requires a massive emotional and financial adjustment. Whether you are caught off guard by the true cost of healthcare, struggling to find purpose without your professional identity, or surprised by how your relationship dynamics shift at home, the gap between retirement expectations and retirement reality is notoriously wide. By understanding where these common misconceptions lie, you can recalibrate your plans today, avoid expensive surprises, and build a more fulfilling, sustainable life after retirement.

1. Medicare Will Cover All Your Healthcare Needs

Many Americans approach age 65 assuming Medicare acts as a golden ticket to free healthcare; the reality involves significant out-of-pocket costs and complex coverage gaps. While Original Medicare provides excellent foundational coverage for hospital stays and doctor visits, it does not cap your annual out-of-pocket spending. Furthermore, routine dental work, vision exams, hearing aids, and most importantly, long-term custodial care are strictly excluded from Original Medicare coverage.

You must actively plan for monthly Part B premiums, which can increase based on your income level through a surcharge known as IRMAA (Income-Related Monthly Adjustment Amount). To protect your nest egg from catastrophic medical events, you will likely need to purchase supplemental coverage. Understanding the structural differences between your primary coverage options is a vital first step.

| Coverage Type | How It Works | Best Suited For |

|---|---|---|

| Original Medicare (Parts A & B) | Federal program covering hospital and medical insurance. Pays 80% of approved costs after deductibles. | Retirees who want maximum flexibility to see any doctor nationwide who accepts Medicare. |

| Medigap (Supplemental) | Private insurance bought alongside Original Medicare to pay the remaining 20% and cover copays. | Retirees with frequent medical needs who want predictable, fixed monthly healthcare costs. |

| Medicare Advantage (Part C) | Private alternative bundling Parts A, B, and usually D. Often includes dental/vision but uses provider networks. | Healthy retirees willing to use network doctors in exchange for lower monthly premiums and extra perks. |

Taking the time to research your options on the official Medicare.gov portal well before your 65th birthday ensures you do not miss critical enrollment windows or face lifetime late penalties.

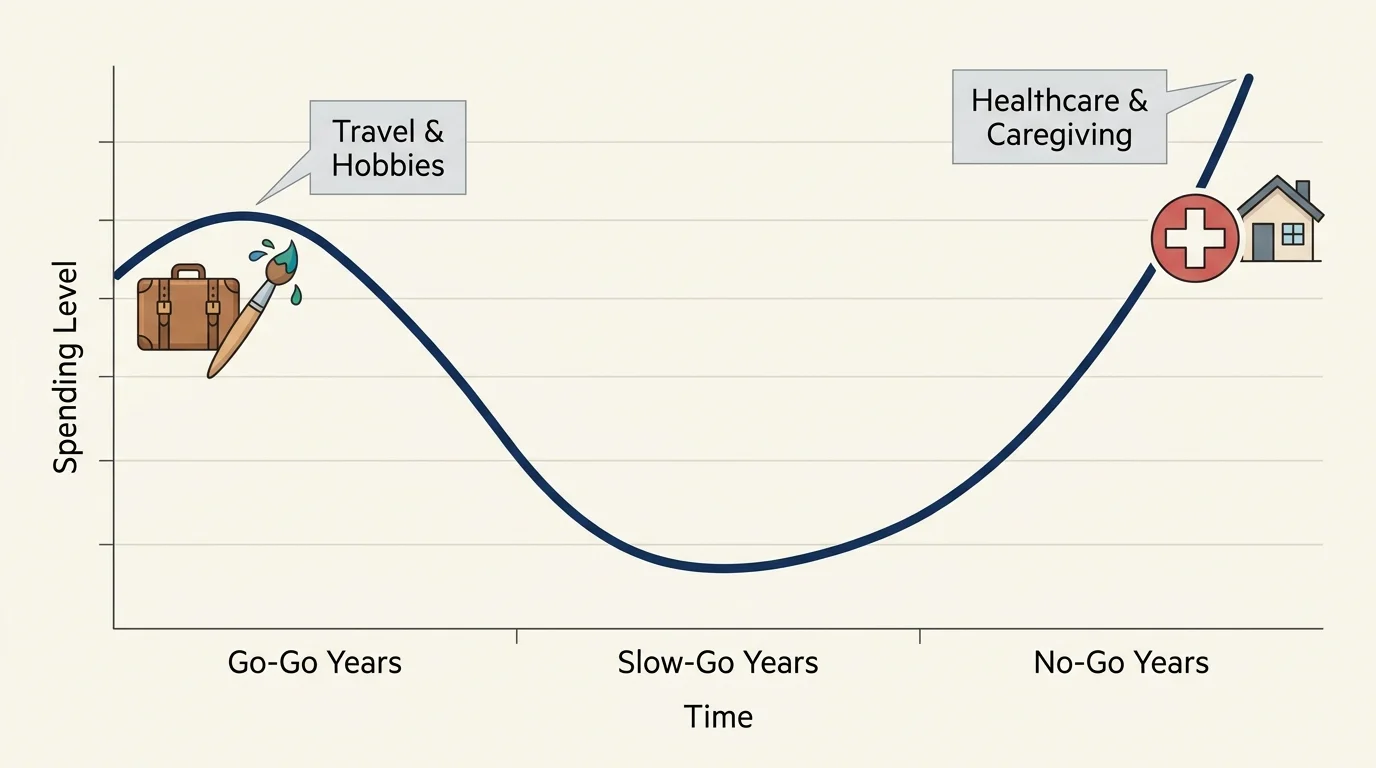

2. Your Living Expenses Will Plummet Immediately

Traditional financial advice often suggests you will only need 70 to 80 percent of your pre-retirement income once you stop working. This rule of thumb leads many to expect an immediate, drastic drop in their cost of living. In practice, retirement spending tends to resemble a “smile” curve over time.

During the early, active years of retirement—often called the “go-go” years—your spending might actually increase. With 40 to 50 extra hours of free time every week, you are more likely to travel, pursue expensive hobbies, dine out, and tackle major home renovations. As you age into the “slow-go” years, your discretionary spending typically dips. However, the curve swings back upward in your later “no-go” years as healthcare, mobility assistance, and caregiving expenses take precedence. Budgeting for a flat line of low expenses ignores the dynamic nature of how you will actually live.

3. Social Security Is Designed to Replace Your Paycheck

Viewing Social Security as a primary retirement income source is a dangerous miscalculation. The program was designed in the 1930s as a safety net to prevent elder poverty, not to fully fund a modern, comfortable lifestyle. For the average worker, Social Security replaces roughly 40 percent of pre-retirement earnings. If you are a high earner, that replacement percentage drops even lower.

Deciding exactly when to claim your benefits is one of the most consequential financial decisions you will make. Claiming at age 62 locks in a permanent reduction in your monthly check, while waiting until age 70 maximizes your lifetime monthly payout. Before making any decisions based on assumptions, you should pull your actual numbers using the Social Security Retirement Estimator to see precisely what your baseline guaranteed income will look like.

4. Endless Free Time Equals Endless Happiness

The honeymoon phase of retirement usually lasts anywhere from a few months to a year. Sleeping in, playing golf on a Tuesday, and ignoring the alarm clock feels incredibly liberating at first. Eventually, the novelty wears off, leaving a massive void where your professional identity, daily structure, and workplace socialization used to be.

A successful retirement requires deliberate lifestyle design. Without a career to dictate your schedule, you must become the architect of your own days. Retirees who thrive are those who intentionally cultivate new communities, volunteer, mentor, or engage in continuous learning. Moving away from a stressful job is not enough; you need a proactive vision for your future.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

5. Staying in Your Current Home Is the Easiest Option

Aging in place is a beautiful goal, but assuming your current family home will serve you well into your 80s and 90s is a common oversight. That sprawling two-story house with a large yard was perfect for raising children; it may become an isolating burden when you are dealing with mobility issues, rising property taxes, and endless maintenance.

True aging in place requires foresight and often significant financial investment. You must evaluate your home for safety: Can you easily install a walk-in shower? Are the doorways wide enough to accommodate a walker or wheelchair? Is the laundry room on the main floor? Furthermore, suburban homes can lead to severe social isolation if you eventually have to give up your driver’s license. Exploring community resources through the Eldercare Locator can help you evaluate whether modifying your current home or downsizing to a more accessible community is the smarter play.

6. Your Taxes Will Disappear When You Stop Working

One of the most unpleasant surprises for new retirees is realizing that the IRS still wants a share of their income. While you will no longer pay payroll taxes (FICA) on investment income, your traditional 401(k) and IRA withdrawals will be taxed as ordinary income. Because you deferred taxes when you contributed to these accounts, the government expects its cut when you take the money out.

Additionally, depending on your combined income, up to 85 percent of your Social Security benefits may be taxable at the federal level. You will also face Required Minimum Distributions (RMDs) starting at age 73 (or 75, depending on your birth year), which forces you to withdraw—and pay taxes on—a specific portion of your pre-tax retirement accounts annually, regardless of whether you actually need the cash. Strategic tax planning is just as critical in retirement as it was during your earning years.

7. You Can Always Pick Up Part-Time Work If Needed

Many pre-retirees bridge the gap in their financial plans with a simple assumption: “If I run low on money, I will just consult or get a part-time job.” While working during retirement can be incredibly rewarding and provides excellent supplemental income, relying on it as a guaranteed financial safety net is risky.

Health events, both your own and those of your spouse, can suddenly eliminate your ability to work. Furthermore, age discrimination in the hiring process, while illegal, remains a stubborn reality. Technology evolves rapidly, and stepping out of the workforce for even a few years can make re-entry difficult. If part-time work is part of your financial plan, secure those opportunities before you officially sever ties with your primary career.

8. You Will Effortlessly Shift from Saving to Spending

If you have spent 40 years diligently saving money, clipping coupons, and watching your portfolio grow, the psychological transition to withdrawing that money can be genuinely terrifying. Many retirees suffer from a scarcity mindset, irrationally hoarding their assets and depriving themselves of the experiences they saved for in the first place.

This reluctance to spend is rooted in the fear of outliving your money. To combat this, you need a highly structured, reliable withdrawal strategy—such as the classic 4% rule or a dynamic spending model—that gives you psychological permission to enjoy your wealth safely.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” — Robert Kiyosaki

9. Your Relationship Dynamics Will Remain Unchanged

Going from spending a few hours together in the evenings to being under the same roof 24/7 requires a significant period of adjustment for married couples. The Japanese even coined a term for this phenomenon: “Retired Husband Syndrome,” which describes the stress a wife experiences when her suddenly retired spouse disrupts her established daily routines.

Navigating this transition smoothly requires open, honest communication. You and your partner need to discuss your respective visions for retirement. Do you want to travel the country in an RV while your spouse wants to stay home and tend to the garden? Establishing boundaries, maintaining separate hobbies, and giving each other breathing room are essential steps for protecting your marriage during this massive life transition.

10. You Can Delay Long-Term Care Planning Until You Need It

The single biggest threat to a well-funded retirement is a prolonged need for long-term care. Statistics show that roughly 70 percent of adults surviving to age 65 will need some form of long-term care services before they die. Because Medicare does not pay for non-medical custodial care—such as help with bathing, dressing, and eating—the financial burden falls squarely on your shoulders.

Whether it is in-home care, an assisted living facility, or a dedicated memory care unit, the costs can easily exceed $100,000 per year. Delaying this conversation until a health crisis strikes removes your ability to choose the type of care you want. You should explore your options early, whether that involves purchasing a long-term care insurance policy, utilizing a life insurance hybrid product, or earmarking a specific portion of your portfolio for future medical needs.

Don’t Make These Mistakes

As you navigate your transition away from full-time work, keep an eye out for these frequent stumbling blocks:

- Claiming Social Security blindly: Do not file for benefits the moment you turn 62 just because you can. Evaluate your breakeven age, your spouse’s survivor benefits, and your tax situation first.

- Ignoring inflation: A fixed pension of $4,000 a month might sound great today, but historically, inflation halves the purchasing power of money every 20 to 25 years. Your portfolio must maintain enough growth-oriented investments to outpace rising costs.

- Underestimating life expectancy: If you make it to 65 in good health, there is a strong statistical probability that you or your spouse will live well into your 90s. Plan for a 30-year retirement, not a 15-year one.

- Making permanent decisions during the honeymoon phase: Selling everything to buy a sailboat or moving across the country to live near grandchildren might sound perfect on day one. Rent first, test the lifestyle, and wait a year before making irrevocable geographic or financial commitments.

When Professional Advice Is Worth It

While managing your own retirement is entirely possible, the complexity of tax optimization, Medicare enrollment, and estate planning often warrants professional guidance. A fee-only fiduciary financial advisor can help you build a tax-efficient withdrawal strategy and stress-test your portfolio against market downturns.

For healthcare decisions, consulting a State Health Insurance Assistance Program (SHIP) counselor provides free, unbiased assistance in navigating Medicare plan comparisons. Furthermore, an elder law attorney is invaluable when drafting durable powers of attorney, updating your living will, and structuring your assets to protect your spouse from the devastating costs of long-term care.

Frequently Asked Questions

How much of my pre-retirement income will I actually need?

Most financial professionals recommend replacing 70 to 80 percent of your pre-retirement income. However, your specific needs depend heavily on your retirement lifestyle, housing situation, and expected healthcare costs.

What is the biggest unexpected expense in retirement?

Healthcare and long-term care consistently rank as the largest surprise expenses. Even with comprehensive Medicare coverage, out-of-pocket costs for premiums, deductibles, dental care, and eventual custodial care can quickly deplete a retirement nest egg.

How do I emotionally prepare for retirement?

Emotional preparation involves separating your identity from your career well before your last day. You should build a schedule of meaningful activities, foster social connections outside of the workplace, and discuss daily routine expectations with your spouse proactively.

Take the time today to look honestly at your retirement strategy and identify which of these expectations might be steering you off course. Adjusting your sails now—whether by delaying Social Security, re-evaluating your housing plan, or simply talking to your spouse about daily routines—can turn potential retirement stress into genuine peace of mind. Your next chapter deserves to be built on reality, not just wishful thinking.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.