The classic vision of a hard-stop retirement at age 65 evaporated during the pandemic. Today, your retirement lifestyle requires a drastically different blueprint because inflation, shifting housing markets, and remote work have permanently rewritten the rules. You face an environment where semi-retirement is the norm, healthcare decisions carry unprecedented weight, and geographic freedom means you can age in place almost anywhere. Navigating this new reality means shedding outdated assumptions about how your post-career years should look. Understanding these nine fundamental shifts will help you protect your savings, optimize your Social Security benefits, and build a resilient daily routine that thrives regardless of what the economy or the world does next.

1. The Hard Stop at Age 65 is Now a Phased Transition

Historically, retirement was viewed as a cliff; you worked 40 hours a week until your 65th birthday, and then you never worked again. The rise of remote and hybrid work environments completely dismantled this expectation. Retirees now leverage flexible schedules to transition into a “phased retirement” or “returnment.” Many professionals negotiate part-time consulting roles with their former employers, keeping one foot in the workforce while reclaiming their time.

This gradual transition provides massive financial and psychological benefits. Continuing to earn even a modest income allows you to delay tapping into your investment portfolios, giving your assets more time to grow. Beyond the math, maintaining a part-time professional identity prevents the sudden loss of purpose that often derails new retirees. Working ten hours a week from your home office on your own terms provides structure without sacrificing your newfound freedom.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

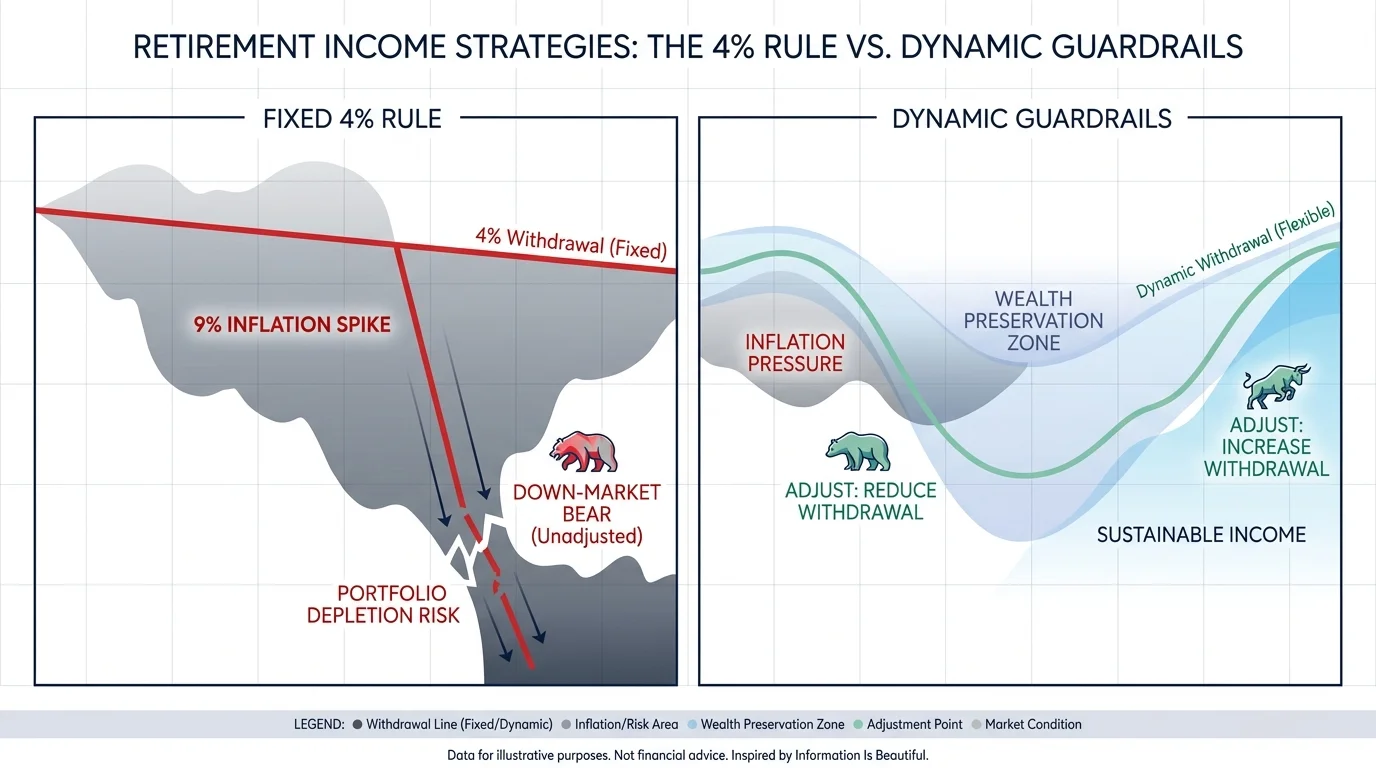

2. Assuming a 4% Withdrawal Rate is Infallible

For decades, financial planners championed the 4% rule: withdraw four percent of your portfolio in year one, adjust for inflation annually, and your money will last 30 years. The aggressive inflation spike of the early 2020s exposed the vulnerability of this rigid formula. If you rigidly increased your withdrawals to match nine percent inflation during a down market, you severely damaged your portfolio’s longevity.

Modern retirement income requires a dynamic withdrawal strategy. Retirees now use “guardrails”—flexible spending plans that adjust based on market performance. During a bull market, you might take a bonus withdrawal for a family vacation; during a bear market, you tighten discretionary spending and skip the inflation adjustment. Flexibility, rather than a mathematical absolute, is the new standard for preserving wealth.

3. Medicare Will Cover All Your Healthcare Needs

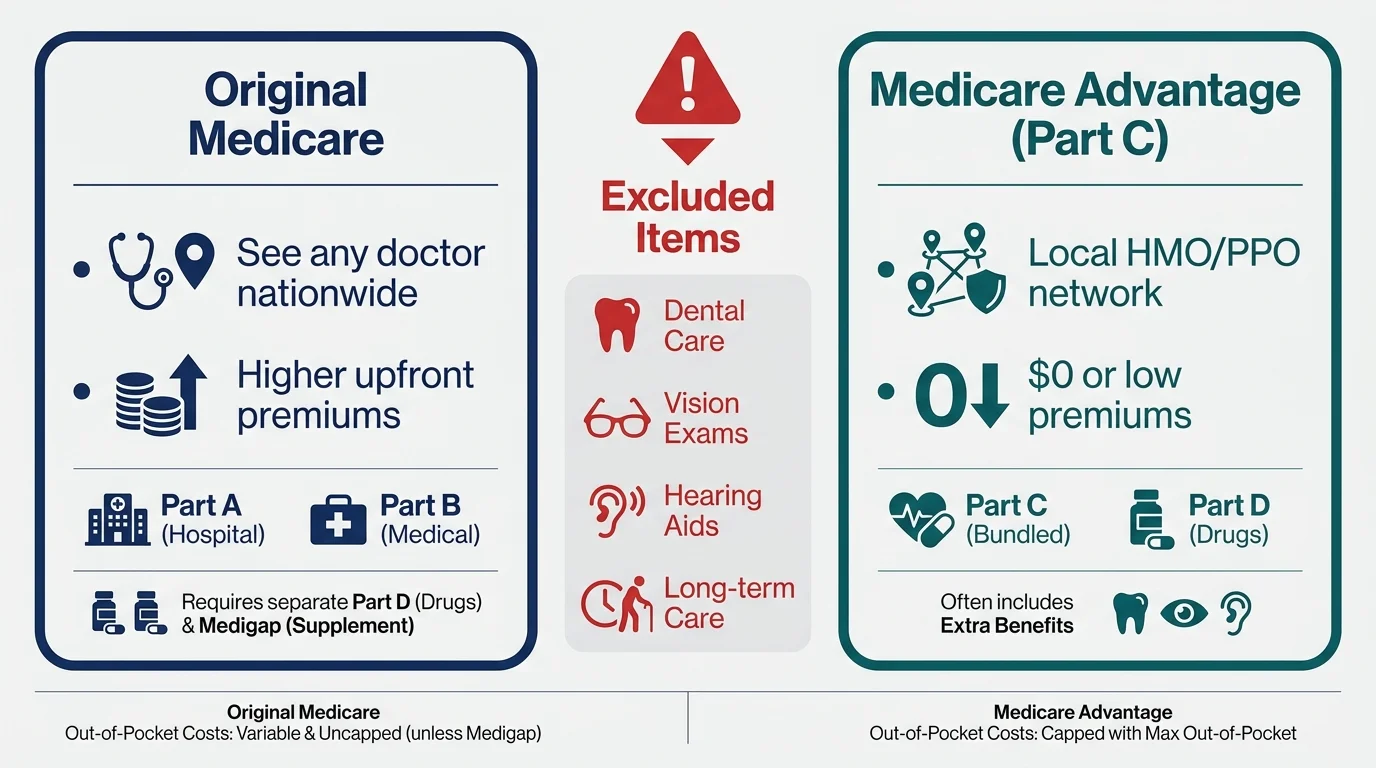

Pre-2020, many Americans viewed turning 65 as crossing the finish line into free, comprehensive healthcare. The reality is far more complex, and modern retirees understand that healthcare is often their largest single expense. Original Medicare does not cover routine dental care, vision exams, hearing aids, or long-term custodial care—critical needs for an aging population.

You must actively choose how you receive your benefits, and that choice dictates your out-of-pocket exposure. Understanding the fundamental differences between your options is critical before visiting Medicare.gov to enroll.

| Feature | Original Medicare (with Medigap) | Medicare Advantage (Part C) |

|---|---|---|

| Provider Choice | See any doctor nationwide who accepts Medicare. No referrals needed. | Must use local HMO/PPO network doctors. Referrals often required. |

| Monthly Premiums | Higher upfront premiums (Part B + Medigap + Part D). | Often $0 or low premium, but you still pay the Part B premium. |

| Out-of-Pocket Limits | Medigap covers most copays/coinsurance, making costs highly predictable. | Varies by plan; can be up to $8,850+ annually before 100% coverage kicks in. |

| Extra Benefits | None. You must buy separate dental/vision policies. | Often includes dental, vision, hearing, and gym memberships. |

4. The Sunbelt Migration is the Default Housing Plan

Selling the family home and migrating to Florida or Arizona used to be a retirement rite of passage. Today, skyrocketing home prices, volatile interest rates, and soaring property insurance costs in coastal states have interrupted the great Sunbelt migration. If you secured a 3% mortgage rate prior to 2022, walking away from it to finance a smaller home at a 7% rate rarely makes financial sense.

Instead, retirees are choosing to stay put and renovate. High-yield savings and localized tax breaks often make remaining in your current community the smartest financial move. When retirees do move, they are increasingly targeting climate-resilient midwestern and Appalachian college towns that offer robust healthcare networks, cultural amenities, and lower insurance burdens.

5. Social Security is Your Primary Income Engine

Treating Social Security as a comprehensive pension replacement is a dangerous modern trap. Decades ago, benefits could cover the bulk of a modest retirement lifestyle. Today, it is best viewed as longevity insurance—a foundational income floor that guarantees you will never be completely destitute, no matter how long you live.

Because every year you delay claiming past age 62 increases your monthly benefit by approximately 8%, optimizing your claiming strategy is more important than ever. If you have a family history of longevity, delaying until age 70 provides a guaranteed, inflation-adjusted return that no bond market can match. You can review your specific projections using the Social Security Retirement Estimator to map out your exact breakeven points.

6. Telehealth Was Just a Pandemic Fad

Virtual doctor visits were initially viewed as a temporary emergency measure. Today, telehealth is a permanent, foundational pillar of aging well. The ability to consult specialists, renew prescriptions, and manage chronic conditions via an iPad has revolutionized senior healthcare.

This technological shift drastically reduces the physical toll of frequent medical appointments. It also expands your geographic freedom. You no longer need to live within a 15-minute drive of your primary care physician if 70% of your appointments can be handled via secure video chat. Remote monitoring devices that track blood pressure, glucose levels, and heart rhythms now transmit data directly to your healthcare team, providing proactive care from your living room.

7. Assisted Living is the Inevitable Final Step

The vulnerabilities exposed in congregate care facilities during the early 2020s sparked a massive cultural shift toward aggressive “aging in place” strategies. Retirees are no longer waiting until a health crisis forces them into a nursing home; they are retrofitting their environments early to ensure they can remain independent indefinitely.

Transforming a standard house into a lifelong home requires specific, proactive modifications. Common upgrades include:

- Zero-threshold entryways: Eliminating steps at exterior doors and showers to accommodate walkers or wheelchairs.

- Main-floor living: Converting ground-floor offices into primary suites to bypass stairs entirely.

- Smart home integration: Installing voice-activated lighting, automated thermostats, and smart stoves that shut off automatically to prevent fires.

- Ambient monitoring: Using non-intrusive sensors that detect falls or irregularities in daily movement patterns without relying on wearable panic buttons.

If you need help finding reputable contractors or community resources for home modifications, the Eldercare Locator connects older adults with verified local support services.

8. Inflation is Just a Theoretical Threat

An entire generation of workers retired between 1990 and 2020 having never experienced structural inflation. The recent economic cycle permanently altered how retirees allocate their assets. Moving your entire nest egg into “safe” cash and bonds at age 65 is now recognized as a massive risk; while bonds protect your principal from market crashes, they leave you entirely exposed to purchasing power erosion.

Modern retirement portfolios must maintain a growth engine. Even at age 70, you might need your money to last another two decades. Maintaining a strategic allocation of equities ensures your wealth grows fast enough to buy the same basket of groceries, pay for the same utilities, and cover the inevitably higher healthcare costs ten years down the line.

9. Caregiving Only Flows Downward

The traditional expectation was that retirees would help pay for their grandchildren’s college or offer occasional babysitting. Post-2020, the “sandwich generation” dynamic has stretched. Retirees in their 60s are frequently finding themselves responsible for their own aging parents in their 90s, while simultaneously providing housing or financial support to adult children navigating expensive housing markets.

This multi-directional caregiving requires strict boundaries. You must secure your own financial oxygen mask before assisting family members. Co-signing large loans or draining your IRA to help an adult child buy a home jeopardizes your own long-term security. Open, honest family meetings about financial realities are no longer optional; they are a survival mechanism.

Errors That Cost Retirees Thousands

Navigating this modern retirement landscape is complex, and unforced errors carry severe financial penalties. Claiming Social Security at 62 simply out of fear that the system will go bankrupt locks in a permanent 30% reduction in your monthly income. Unless you have a terminal illness or absolutely no other income source, panicking into an early claim is mathematically destructive.

Another massive trap is ignoring Medicare IRMAA (Income-Related Monthly Adjustment Amount). If you sell a highly appreciated asset, do a massive Roth conversion, or take a massive portfolio withdrawal, that spike in your modified adjusted gross income can trigger surcharges that double or triple your Medicare Part B and Part D premiums two years later. Strategic tax planning is essential to keep your healthcare costs from ballooning unexpectedly.

When to Get Expert Help

You do not need an expert for every decision, but specific pivot points demand professional guidance. Transitioning from employer healthcare to Medicare is fraught with permanent penalty risks. Working with a State Health Insurance Assistance Program (SHIP) counselor ensures you don’t miss crucial enrollment windows. You can find free, unbiased counseling resources through the National Council on Aging (NCOA).

Financially, consider hiring a fee-only fiduciary planner three to five years before you plan to step away from full-time work. They will stress-test your portfolio against modern inflation rates, help structure tax-efficient withdrawal sequences, and ensure your estate documents protect your assets from long-term care events. If you are coordinating care for a spouse with cognitive decline, an elder law attorney becomes indispensable for navigating Medicaid look-back periods and asset protection trusts.

Frequently Asked Questions

Do I have to claim Social Security as soon as I stop working full-time?

No. Your decision to stop working and your decision to claim Social Security are entirely separate. Many retirees use their 401(k) or savings to bridge the gap from their retirement date until age 70, allowing their guaranteed Social Security benefit to grow to its maximum possible amount.

Can I work part-time while enrolled in Medicare?

Yes. Medicare eligibility is strictly based on age (65) or specific disabilities, not your employment status. You can work full-time or part-time while on Medicare. However, if your employer has fewer than 20 employees, Medicare becomes your primary insurance, making timely enrollment critical to avoid gaps in coverage.

Is aging in place actually cheaper than downsizing to a senior community?

Usually, yes, but it depends on the structural integrity of your home. A $20,000 main-floor bathroom renovation pays for itself in less than four months when compared to the average $5,500 monthly cost of an assisted living facility. However, if your home requires constant, expensive maintenance or lacks proximity to a strong healthcare network, the hidden costs of isolation might outweigh the financial savings.

Take an afternoon this week to log into your Social Security account and review your actual benefit estimates. Compare those numbers against your current spending, factoring in an honest assessment of what healthcare might cost you over the next decade. The landscape has changed, but with clear data and a flexible mindset, you can build a retirement strategy that thrives in this new era.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.