Maximizing your retirement income often means waiting to claim benefits, but delaying Social Security past age 70 offers zero financial return and could cost you around $144,000 in forfeited payments. The government stops awarding delayed retirement credits the month you hit your seventieth birthday. If you wait until age 74 because you are still working or do not need the cash right now, those monthly checks vanish forever. This monumental error happens frequently, draining hard-earned wealth from retirees who miss the claiming deadline. Understanding the mechanics of your Social Security strategy ensures you capture every dollar you deserve.

The Mechanics Behind the $144,000 Mistake

Retirement planning is filled with complex rules, yet one of the most absolute boundaries in the American retirement system is the age 70 cap on Social Security growth. For years, financial media and retirement planners drill a singular message into the minds of aging workers: delay your benefits as long as possible to secure the highest monthly payout. While patience is generally rewarded, treating Social Security like an endless growth asset is a critical miscalculation.

To understand exactly how this mistake costs retirees so much money, you must look at the actual mathematics of a delayed claim. Imagine you have a primary insurance amount—the baseline benefit you are entitled to at your full retirement age—that grows to exactly $3,000 per month by the time you reach age 70. This $3,000 represents the absolute ceiling of your personal benefit based on your earnings record. It will never grow organically again, aside from annual cost-of-living adjustments.

Suppose you decide to keep working until age 74. You earn a high salary, you feel healthy, and you mistakenly assume that keeping your benefits untouched will shield them from taxes while they continue to grow. Because you delayed claiming for 48 months past your seventieth birthday, you forfeit 48 individual checks of $3,000. By the time you finally file the paperwork at 74, you have permanently abandoned $144,000. The government will not retroactively pay you for those four missed years; at most, they offer a mere six months of retroactive payments under specific conditions. The remaining money simply reverts back to the trust fund.

This oversight occurs more frequently than you might think. Business owners, high-net-worth individuals, and professionals deeply engaged in their careers often push administrative retirement tasks down their priority list. Unfortunately, failing to file your application three months before your seventieth birthday turns a solid financial delay strategy into an irreversible financial loss.

How Delayed Retirement Credits Actually Work

Your Social Security strategy revolves around a specific chronological milestone known as your Full Retirement Age. Depending on the year you were born, this age lands somewhere between 66 and 67. If you claim benefits the exact month you reach this milestone, you receive 100 percent of the monthly payout calculated from your highest 35 years of indexed earnings.

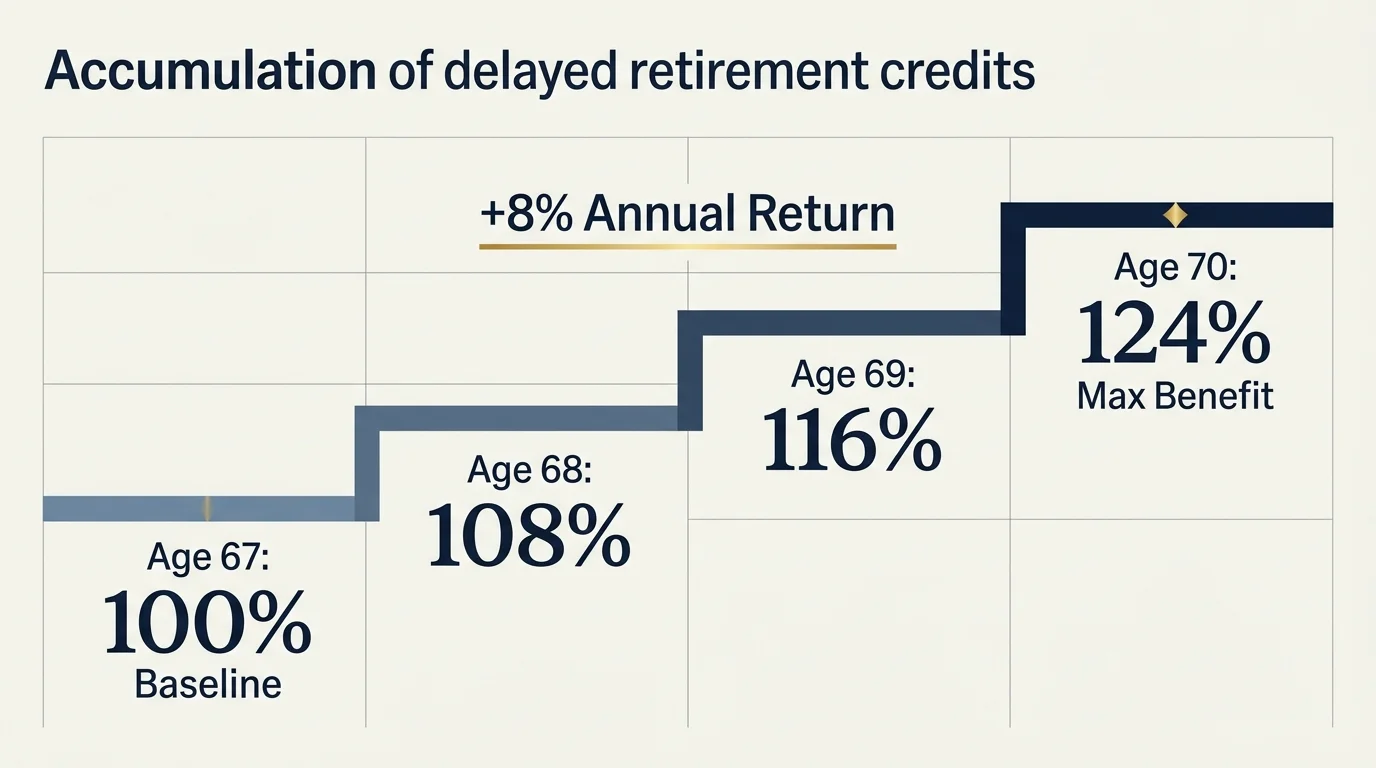

However, the Social Security Administration provides a powerful financial incentive for those who can afford to wait. For every single month you delay claiming past your full retirement age, you earn delayed retirement credits. These credits increase your eventual payout by two-thirds of one percent per month, which mathematically translates to exactly 8 percent per year.

In today’s economic environment, a guaranteed 8 percent annual return—backed by the federal government and adjusted for inflation—is completely unparalleled. Not even the most aggressive dividend stocks or high-yield bonds can offer that level of risk-free growth. If your full retirement age is 67 and you delay to 70, your monthly benefit permanently increases by 24 percent. If your baseline benefit was $2,000, waiting until 70 transforms that check into $2,480 before factoring in any inflation adjustments.

The crucial detail—the one that leads to the massive forfeiture of wealth—is that these 8 percent annual credits definitively expire the month you blow out the candles on your seventieth birthday cake. From that day forward, the only increases your check will ever see are the annual cost-of-living adjustments applied universally to all beneficiaries. Leaving the money unclaimed after this cutoff date provides zero structural advantage to your retirement income.

The Breakeven Reality of Your Social Security Strategy

Deciding exactly when to claim your benefits requires evaluating a concept known as the breakeven point. This is the specific age at which the total dollar amount received from a delayed, higher monthly benefit surpasses the total dollar amount you would have collected by claiming a smaller benefit earlier.

If you claim as early as possible at age 62, your monthly check faces a permanent reduction of up to 30 percent compared to your full retirement age amount. While the checks are smaller, you receive them for a much longer period. Delaying until age 70 results in significantly larger checks, but you miss out on eight full years of income that you could have been spending or investing.

For most Americans, the breakeven age falls roughly between 80 and 82. If you expect to live well past your early eighties due to excellent health and strong family longevity, delaying to age 70 is overwhelmingly the mathematically superior choice. You will ultimately draw tens of thousands of dollars more from the system over your lifetime. Conversely, if facing severe health challenges, claiming earlier ensures you extract maximum value from the system while you are still able to enjoy it.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

Evaluating this breakeven point requires brutal honesty about your personal health, your immediate cash flow needs, and your family’s financial legacy. It is a highly individualized calculation. You are betting against your own mortality, and how you place that bet directly impacts the financial security of your later decades.

Comparing Social Security Claiming Scenarios

To visualize how these different claiming ages impact your lifetime wealth, consider a hypothetical retiree whose full retirement age is 67, with a baseline benefit of $2,500 per month. This table illustrates the profound impact of claiming early, claiming at full retirement age, maximizing at 70, and making the critical error of waiting until 74.

| Claiming Age | Monthly Benefit Amount | Total Collected by Age 85 | Strategic Result |

|---|---|---|---|

| Age 62 | $1,750 (Reduced by 30%) | $483,000 | Provides immediate cash flow but yields the lowest lifetime total if you live a long life. |

| Age 67 (FRA) | $2,500 (100% of benefit) | $540,000 | The baseline approach; avoids early penalties but misses guaranteed 8% annual growth. |

| Age 70 | $3,100 (Maximized by 24%) | $558,000 | Secures the highest possible monthly check and provides maximum protection against outliving your money. |

| Age 74 (The Mistake) | $3,100 (Capped at age 70) | $409,200 | Permanently forfeits $148,800 in uncollected payments between ages 70 and 74 with absolutely zero benefit. |

Note: This table excludes annual cost-of-living adjustments (COLAs) to clearly illustrate the base mathematical differences between claiming ages.

As the data shows, waiting until 70 clearly provides the highest cumulative lifetime payout if you reach your mid-eighties. However, delaying past 70 brutally sabotages your total collected wealth. Those four lost years destroy the mathematical advantage of the delay strategy entirely.

Errors That Cost Retirees Thousands

Failing to file by age 70 is just one of many ways Americans inadvertently surrender their retirement benefits. Navigating the transition into your post-career life requires vigilance. Here are the most common unforced errors that can permanently damage your retirement income.

- Misunderstanding the Earnings Test: If you claim Social Security before your full retirement age while continuing to work, the government will withhold $1 in benefits for every $2 you earn above a specific annual limit. Many retirees claim early to supplement their income, only to find their benefits completely withheld because they earn too much. Once you reach full retirement age, this earnings penalty disappears entirely.

- Ignoring the Impact on Survivor Benefits: When one spouse passes away, the surviving spouse is entitled to the higher of the two monthly benefits. If the primary earner claims early at 62, they permanently reduce the survivor benefit they leave behind. Delaying to 70 is often described as the best life insurance policy you can buy for your spouse.

- Forgetting to Enroll in Medicare on Time: Medicare and Social Security are distinctly different programs, but their timelines overlap. Failing to enroll in Medicare Parts A and B during your Initial Enrollment Period at age 65 can result in permanent lifetime penalties, regardless of when you plan to claim Social Security. You can manage your enrollment directly through Medicare.gov.

- Improperly Suspending Benefits: Some retirees claim early, realize their mistake, and wish to pause their benefits. You can only suspend your benefits once you reach your full retirement age. Doing so allows your paused benefits to earn delayed retirement credits until age 70. Misunderstanding the strict rules surrounding suspension can lock you into a lower payment forever.

Understanding the Impact on Spousal Benefits

Couples face a much more complex matrix of decisions than single retirees. The rules governing spousal benefits often trip up even savvy financial planners. A spousal benefit allows a lower-earning spouse to collect up to 50 percent of the higher-earning spouse’s full retirement age benefit.

The most vital caveat regarding spousal benefits is that they do not earn delayed retirement credits. If you are claiming a benefit based entirely on your partner’s earnings record, your maximum payout caps out at your own full retirement age (66 or 67). Waiting until age 70 to claim a spousal benefit is a massive financial error because the payout stops growing at your full retirement age. You simply forfeit years of income for no reason.

This creates scenarios where spouses must stagger their claiming strategies. The lower-earning spouse might claim their benefit at full retirement age, while the higher-earning spouse delays until 70 to maximize the household’s total income and protect the eventual survivor benefit.

Navigating Taxes and Medicare Premiums

Your Social Security strategy does not exist in a vacuum; it directly collides with the IRS and the Medicare system. Depending on your total retirement income, up to 85 percent of your Social Security benefits may be subject to federal income tax. The IRS uses a formula called “provisional income” to determine this taxability, which includes half of your Social Security benefit plus your other sources of income, including tax-exempt municipal bond interest.

Because delaying to age 70 creates a larger monthly benefit, it also pushes a higher volume of dollars into your provisional income calculation. However, drawing down your pre-tax retirement accounts (like Traditional IRAs) during your sixties while you delay Social Security can systematically lower your required minimum distributions (RMDs) later in life, potentially creating a smoother tax ride in your eighties.

Furthermore, your Medicare Part B premiums are automatically deducted from your Social Security checks. If your income exceeds certain thresholds, you will be hit with the Income-Related Monthly Adjustment Amount (IRMAA), effectively raising the cost of your healthcare. Coordinating your withdrawals to avoid triggering IRMAA spikes is a delicate balancing act. You can find robust resources on managing these intertwined systems through the Consumer Financial Protection Bureau.

When to Get Expert Help

While standard claiming strategies work well for single individuals with straightforward work histories, certain circumstances absolutely demand professional guidance. You should consult a fee-only fiduciary financial advisor or a specialized Social Security claiming expert if your situation includes any of the following complexities.

First, if you are divorced but your marriage lasted 10 years or longer, you may be entitled to claim benefits based on your ex-spouse’s earnings record. The rules governing divorced spouse benefits are highly specific, especially regarding whether your ex-spouse has filed yet and how remarriage impacts your eligibility.

Second, if you spent part of your career working for a government agency or educational institution that did not withhold Social Security taxes, you may be subject to the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). These two provisions can aggressively slash your expected benefits, rendering standard online calculators completely inaccurate.

Finally, business owners and those with complex tax situations should work with an elder law attorney or CPA to structure their exit strategy. Properly timing the sale of a business alongside a Social Security claim requires precise tax engineering to avoid devastating tax brackets.

Frequently Asked Questions

Can I claim retroactive benefits if I wait past age 70?

If you file for benefits after age 70, the Social Security Administration will only pay up to six months of retroactive benefits. For example, if you apply at age 72, you will receive a lump sum for the past six months, but the preceding 18 months of benefits are permanently forfeited.

Does delaying my Social Security increase my spouse’s spousal benefit?

No. A spousal benefit is strictly based on 50 percent of the primary earner’s benefit at their full retirement age. The primary earner delaying until age 70 increases their own individual check and the potential survivor benefit, but it does not increase the living spousal benefit.

What happens to my benefits if I continue working full-time after age 70?

Once you reach the month of your full retirement age, the earnings test disappears entirely. You can earn an unlimited amount of income from a job or a business without any reduction to your Social Security benefits. By age 70, you are entirely free to work and collect your maximum benefit simultaneously.

Are Medicare enrollment and Social Security claiming linked?

They share administrative ties but have separate timelines. You are eligible for Medicare at age 65, and you must proactively enroll if you are not yet collecting Social Security. If you are already collecting Social Security at 65, Medicare Part A and Part B enrollment is generally automatic.

Actionable Steps to Finalize Your Retirement Income Plan

Securing your financial future requires moving from passive research to deliberate action. Start by creating or logging into your personalized account on the official federal portal to review your earnings record. Ensure there are no missing years of income, as your benefit is calculated using your highest 35 earning years. A zero in the calculation significantly drags down your primary insurance amount.

“The best time to plan for retirement was 20 years ago. The second best time is today.” — Proverb

Next, map out a specific timeline detailing exactly when you plan to step away from your career, when you need to activate Medicare, and the precise month you will file for Social Security. Set digital calendar reminders for yourself well in advance of your seventieth birthday. Remember, the goal of delaying benefits is to provide absolute financial security in your twilight years, but that security is only realized if you actively reach out and claim what is rightfully yours before the clock runs out.

Do not let administrative oversight drain your wealth. Take control of your timeline today, consult with professionals if your situation involves divorce or government pensions, and ensure you file the necessary paperwork precisely when your maximum benefit is reached.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.