The four-bedroom house where you raised a family holds decades of memories, but maintaining empty rooms and sprawling lawns often becomes a drain on your energy and retirement nest egg. Holding onto a property that no longer fits your daily life forces you to spend valuable time and money on upkeep rather than enjoying your hard-earned freedom. Recognizing the right moment to transition to a more manageable living situation preserves your wealth and protects your independence. If you find yourself cleaning rooms you never use or dreading the annual property tax bill, evaluating your housing needs can unlock significant capital and drastically improve your quality of life during your golden years.

1. Home Maintenance Has Become a Physical and Financial Burden

Homeownership requires relentless effort. Mowing the lawn, cleaning the gutters, painting the exterior, and repairing appliances take physical tolls that often become harder to manage as you age. When you find yourself exhausted by weekend chores or paying expensive contractors for tasks you once handled yourself, your house has shifted from a sanctuary to a liability.

Downsizing retirement living spaces directly cuts these obligations. Moving into a smaller home or a community where a homeowners association handles exterior maintenance gives you your time back. You worked for decades; you should spend your retirement enjoying your hobbies, traveling, or relaxing with family, not climbing ladders to fix a leaky roof or shoveling heavy snow off a driveway.

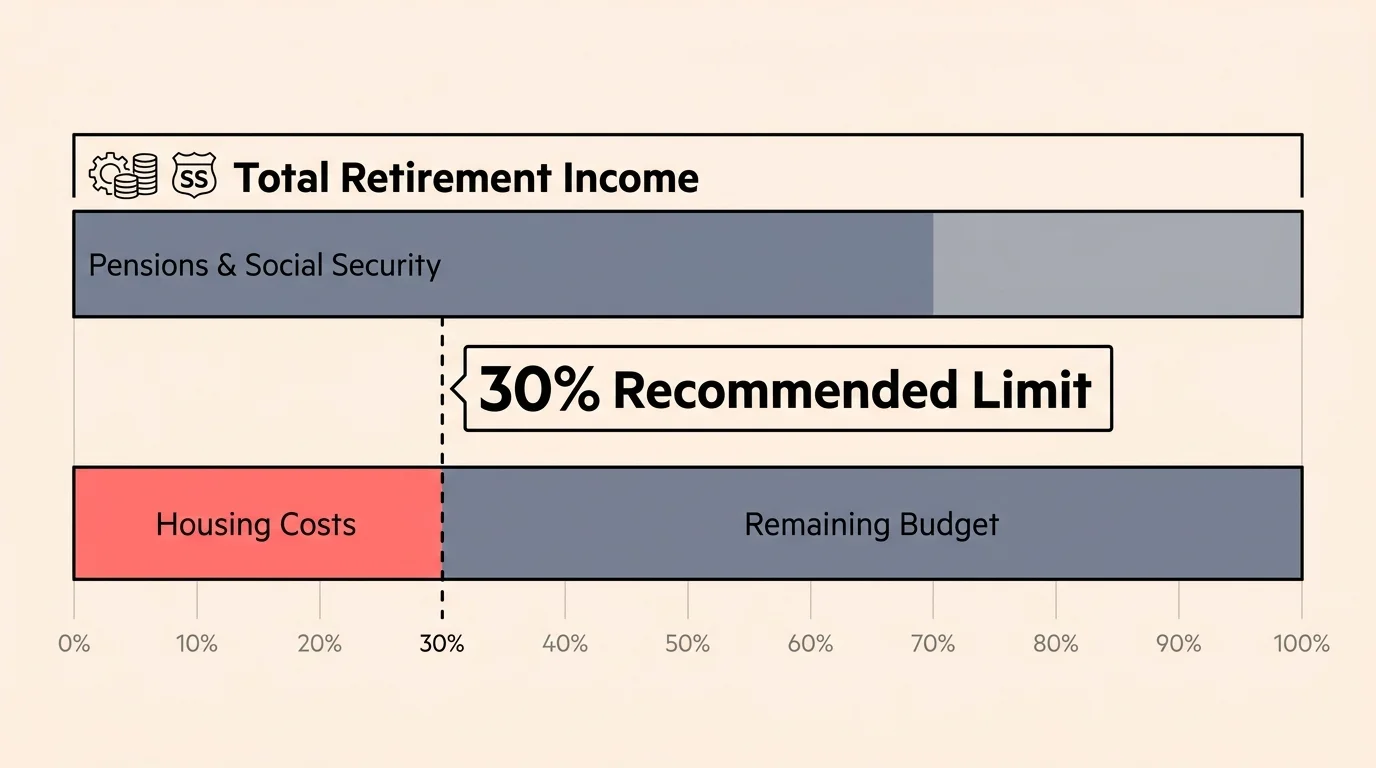

2. Your Housing Costs Exceed 30 Percent of Your Retirement Income

Financial planners generally suggest keeping your total housing costs—including mortgage payments, property taxes, insurance, and utilities—under 30 percent of your gross income. Once you transition to a fixed income from Social Security, pensions, and retirement withdrawals, adhering to this rule becomes paramount. If your housing expenses consume a larger piece of your monthly budget, you risk depleting your retirement savings prematurely.

Downsizing offers a straightforward solution to balance your budget. By securing a less expensive property, you reduce your monthly overhead and free up cash flow for healthcare, daily living expenses, and leisure activities. If you want to review how housing impacts your overall financial stability, the Consumer Financial Protection Bureau (CFPB) offers excellent resources for managing your retirement budget and planning for long-term expenses.

3. Unused Rooms Are Collecting Dust and Clutter

Walk through your house and honestly assess how many rooms you use daily. Most retirees spend 90 percent of their time in the kitchen, living room, and primary bedroom. Those extra guest rooms, formal dining rooms, and finished basements sit empty, yet you still pay to heat, cool, and clean them. Heating and cooling empty square footage wastes hundreds of dollars annually.

Furthermore, unused rooms tend to become magnets for clutter. Spare bedrooms quickly transform into storage units for old furniture, seasonal decorations, and grown children’s childhood belongings. Downsizing forces you to evaluate your possessions and keep only what truly adds value to your life. Choosing smaller homes retirees actually need eliminates the physical and financial waste of maintaining a museum to your past.

4. Navigating Your Home Feels Less Safe

Mobility changes over time, and a house with steep stairs, narrow hallways, or high-step bathtubs can suddenly present severe safety hazards. A single fall can drastically alter your retirement trajectory. If you find yourself avoiding the basement, holding tightly to handrails, or feeling anxious about navigating your own bathroom, your home no longer supports your physical needs.

Retrofitting an older, multi-level home with chair lifts, walk-in tubs, and widened doorways often costs tens of thousands of dollars, and these modifications rarely add resale value to the property. Moving to a single-story home or an accessible apartment provides a safer environment without the stress of endless renovations. The National Institute on Aging provides comprehensive guidelines on fall prevention and accessible living options for seniors.

5. You Want to Unlock Home Equity to Fund Your Lifestyle

Your home likely represents a massive portion of your net worth. While having a paid-off mortgage provides emotional security, that trapped equity does not generate income to pay for groceries, gas, or vacations. Selling a large property and buying a less expensive home allows you to pocket the difference.

You can invest this surplus cash to generate reliable monthly income, bolstering your Social Security and pension payments. Smart retiree home decisions often revolve around liquidity. Converting illiquid real estate into an income-producing portfolio ensures you never have to worry about outliving your money. Accessing this capital gives you the freedom to fund healthcare needs, assist grandchildren with college tuition, or simply enjoy a higher daily standard of living.

6. You Feel Isolated in Your Current Neighborhood

Neighborhoods evolve. The families you raised children alongside may have moved away, replaced by busy young professionals who are rarely home during the day. If you feel isolated or disconnected from your immediate community, staying in your current house might negatively impact your mental and physical health. Social connection acts as a critical pillar of healthy aging.

Moving to an active adult community, a condominium complex, or a walkable urban neighborhood instantly surrounds you with peers. These environments naturally foster friendships, shared activities, and a sense of belonging that sprawling suburban subdivisions often lack. Having neighbors nearby also provides a vital safety net in case of emergencies.

7. Property Taxes and Insurance Premiums Are Spiking

Even if you paid off your mortgage years ago, you never truly stop paying for your house. Local governments periodically reassess property values, leading to escalating property tax bills. Simultaneously, home insurance premiums continue to surge nationwide due to increased building costs and severe weather events. You have zero control over these mandatory expenses.

If rising taxes and insurance premiums create anxiety every time you check the mail, downsizing can provide immediate relief. Moving to a smaller property—or relocating to a state with more favorable tax policies and lower insurance risks—protects your fixed income from unpredictable inflation. Shrinking your footprint directly shrinks your exposure to municipal tax hikes.

8. Travel and Leisure Are Your Top Priorities

Many Americans dream of spending their retirement traveling the country in an RV, visiting grandchildren across the nation, or exploring international destinations. However, leaving a large house vacant for weeks or months generates constant worry. You must arrange for lawn care, stop the mail, monitor the thermostat, and constantly worry about burst pipes or break-ins.

Downsizing to a condo or a townhome unlocks a highly desirable retirement lifestyle. Knowing a community association handles the exterior maintenance and neighbors are right next door allows you to lock your front door and head to the airport with complete peace of mind. A smaller, low-maintenance property enables the nomadic lifestyle many retirees crave.

9. The Idea of a Fresh Start Sounds Appealing

Sometimes the most compelling reason to move requires no financial spreadsheet or physical assessment. You simply crave a new chapter. Staying in the same house for forty years can make your routine feel stagnant. Moving presents a tremendous opportunity to reinvent your daily life.

You can choose a location closer to cultural centers, the beach, or your family. A new, smaller space allows you to redecorate, declutter, and curate an environment that reflects who you are today, rather than who you were twenty years ago.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

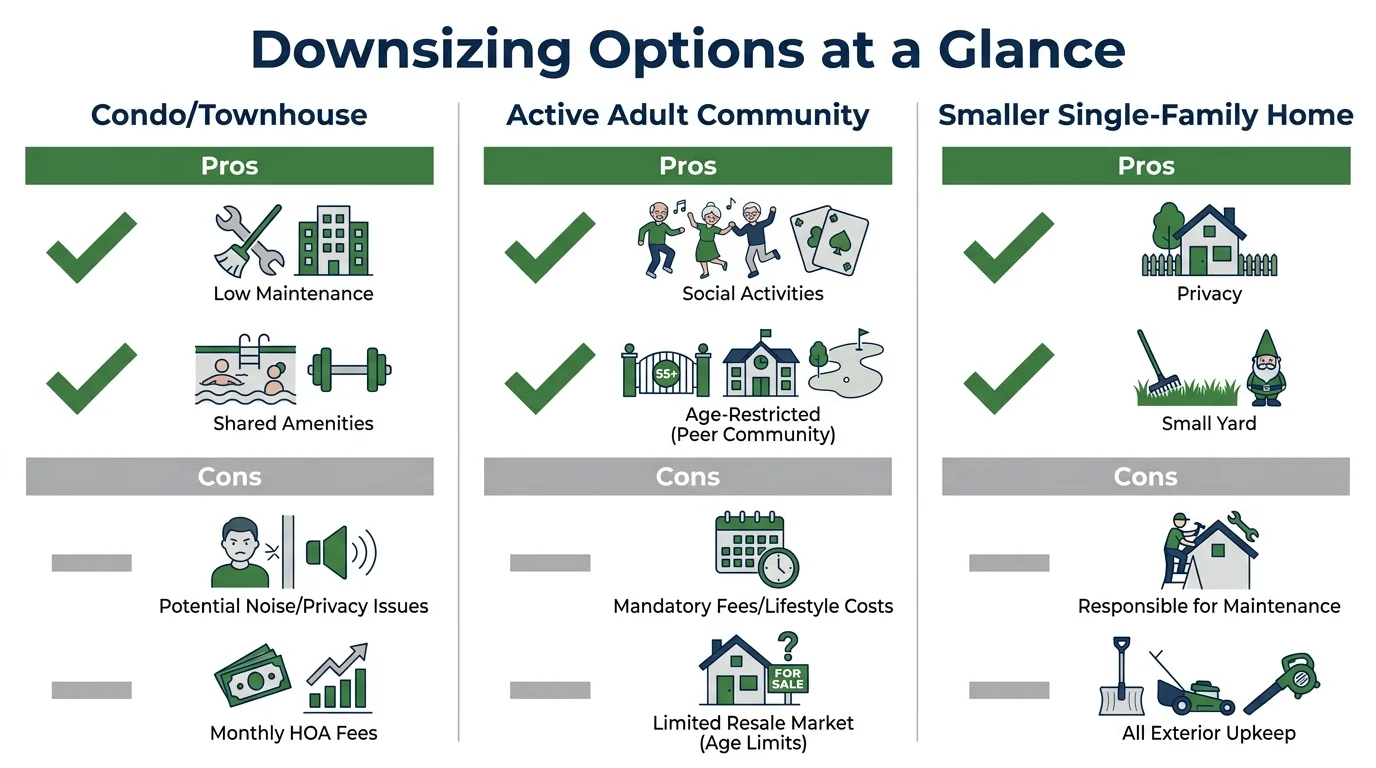

Comparing Your Downsizing Options

Once you decide to move, you face several distinct housing choices. Review the table below to understand which environment aligns best with your goals.

| Housing Type | Primary Benefits | Potential Drawbacks | Best Suited For |

|---|---|---|---|

| Single-Story Home | No stairs; full independence; private outdoor space; complete control over property. | You remain responsible for all exterior maintenance and repairs. | Retirees who want privacy and enjoy light gardening but need a safer floor plan. |

| Condo or Townhome | Exterior maintenance covered; often includes amenities like pools or gyms; easier to lock and leave. | Monthly HOA fees can increase; less privacy; shared walls; association rules restrict modifications. | Frequent travelers who want zero exterior chores but desire homeownership. |

| Active Adult (55+) Community | Built-in social network; age-restricted; extensive recreational activities and clubs. | Higher association fees; lacks multi-generational diversity; location may be far from city centers. | Social retirees seeking community engagement and peer interaction. |

| Continuing Care Retirement Community (CCRC) | Guaranteed transition to assisted living or nursing care if needed; high level of services. | Substantial upfront buy-in fees; high monthly costs; complex contracts requiring legal review. | Planners who want to secure their long-term medical care without moving again. |

Don’t Make These Mistakes When Downsizing

Moving is stressful, and the emotional weight of leaving a long-time family home can lead to poor decisions. Protect your assets and your sanity by avoiding these common missteps:

- Underestimating Moving and Closing Costs: Real estate agent commissions, staging costs, minor repairs to prepare your home for sale, and professional movers can easily consume 8 to 10 percent of your home’s sale price. Factor these expenses into your budget before calculating your net profit.

- Rushing the Decluttering Process: Trying to sort through decades of memories in a single weekend leads to burnout and regret. Start decluttering six months before you plan to list your home. Tackle one room at a time, starting with the least sentimental spaces like the garage or guest bathroom.

- Trying to Keep Oversized Furniture: The sprawling sectional sofa and massive formal dining table rarely fit in a modern downsized space. Measure your new floor plan carefully. Sell or donate bulky furniture and invest in pieces scaled appropriately for your new home.

- Waiting Until a Health Crisis Forces the Move: Downsizing on your own terms empowers you to choose your ideal location and handle the logistics at your own pace. If you wait until an injury or illness occurs, your family will have to make rushed decisions on your behalf, often resulting in fewer choices and higher costs.

When Professional Advice Is Worth It

Navigating the sale of your largest asset while planning for decades of retirement living requires precision. While you can manage much of the downsizing process independently, certain situations warrant expert guidance.

Consult a fiduciary financial advisor to determine exactly how to invest the proceeds from your home sale. An advisor helps structure these funds to generate monthly income while protecting against market volatility and inflation. If your home has appreciated significantly over the decades, work with a tax professional to understand potential capital gains taxes. Although the IRS offers exclusions for primary residences, exceeding those limits can trigger hefty tax bills.

Additionally, an elder law attorney proves invaluable if you are considering moving into a Continuing Care Retirement Community (CCRC). These communities require complex, binding contracts that dictate future healthcare costs and refund policies. An attorney ensures you understand your rights and obligations before you sign away a significant portion of your net worth.

Frequently Asked Questions About Downsizing in Retirement

Will selling my home affect my Medicare premiums?

It certainly can. If you realize a massive capital gain from selling your home, that profit counts toward your Modified Adjusted Gross Income (MAGI). If your income spikes for the year, you may trigger the Income-Related Monthly Adjustment Amount (IRMAA), which increases your Medicare Part B and Part D premiums. The official Medicare website provides current IRMAA thresholds. You should consult a tax advisor to explore strategies for minimizing this impact.

How do I handle decades of accumulated possessions?

Take a systematic approach. Sort items into four categories: keep, sell, donate, and trash. If an item does not serve a functional purpose in your new, smaller home and does not hold deep sentimental value, let it go. For large collections or valuable antiques, consider hiring a professional estate sale company to manage the pricing and selling process for you.

Does downsizing always save money?

Not necessarily. While moving to a smaller space usually reduces utility bills and property taxes, hidden costs can offset these savings. Purchasing a condo might introduce high monthly Homeowners Association (HOA) fees or special assessments. Furthermore, if you move to a higher cost-of-living state to be near grandchildren, your daily expenses could increase. Always run a comprehensive budget comparing your current costs against projected costs in the new location.

Your Next Steps

Evaluating your living situation represents a massive step toward securing your financial future and enhancing your daily comfort. Begin by tracking your exact housing expenses over the next month, including utilities, maintenance, and taxes. Then, schedule a tour of a few different senior housing options in your area—even if you are not ready to move today. Seeing tangible alternatives demystifies the process and helps you envision the freedom a simpler lifestyle provides.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.