Trading your snow shovel for a beach chair sounds like the ultimate reward after decades of hard work, but the reality of living by the ocean often clashes with the vacation fantasy. When you only visit a beach town for a week in July, you miss the systemic infrastructure issues, seasonal isolation, and hidden financial drains that permanent residents face year-round. Identifying coastal retirement red flags before you sell your family home can save you from a costly geographic mistake that jeopardizes your fixed income. We compiled the most pressing beach retirement risks so you can evaluate whether that oceanfront condo is a sound investment or a financial trap disguised as a permanent vacation.

Red Flag 1: Unpredictable and Skyrocketing Insurance Premiums

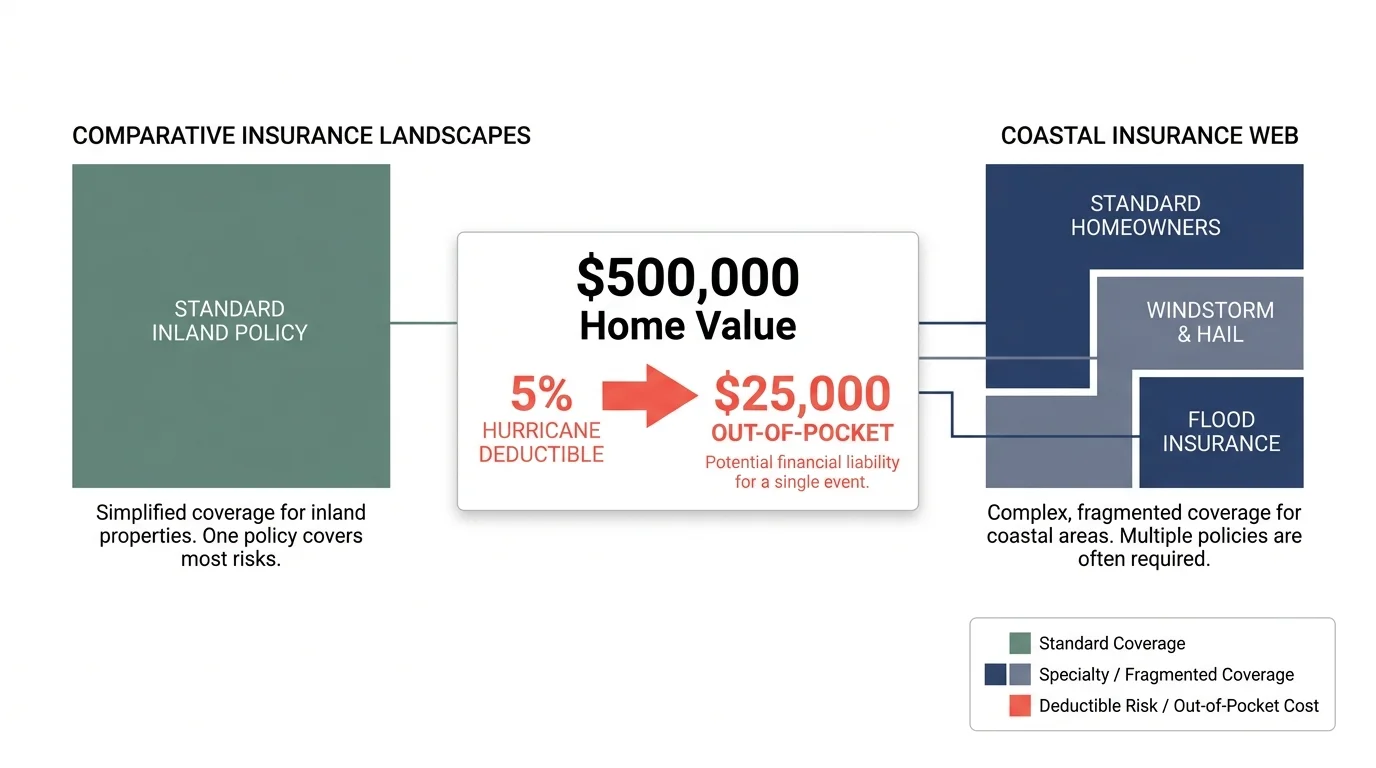

Perhaps the most immediate threat to a fixed-income retirement budget is the volatile nature of coastal property insurance. Inland homeowners typically purchase a single, comprehensive policy that covers fire, theft, and basic weather damage. When you move to the coast, that unified approach splinters into a complex web of required, expensive policies.

Many coastal states now allow insurance providers to exclude windstorm and hail damage from standard policies; you must purchase a separate windstorm policy with its own distinct deductible. Furthermore, these deductibles are rarely flat rates. Instead, they are calculated as a percentage of your home’s total insured value. If your coastal home is insured for $500,000 and carries a 5% hurricane deductible, you must pay $25,000 out of pocket before your coverage kicks in. This completely alters your emergency fund requirements.

Additionally, standard homeowners insurance never covers flood damage. You will need a separate policy through the National Flood Insurance Program (NFIP) or a private carrier. In recent years, risk-rating updates have caused premiums in low-lying coastal areas to double or triple. If you are touring properties and the real estate agent dismisses insurance costs as a minor detail, consider that a glaring warning sign.

Red Flag 2: The Silent Destruction of Saltwater Corrosion

Salt air is notoriously corrosive; it degrades building materials and mechanical systems at an alarming rate. Most retirees fail to factor this accelerated depreciation into their monthly budget, assuming their home maintenance costs will mirror what they paid in the suburbs.

Consider your heating, ventilation, and air conditioning (HVAC) system. A standard exterior condenser unit in a mild, inland climate might easily last fifteen years. On the coast, constant exposure to salt spray can rot the aluminum fins and copper coils in fewer than five years. Unless you invest in specialized, factory-applied anti-corrosion coatings—which add significantly to the upfront cost—you will replace major appliances much more frequently.

The corrosion extends beyond appliances. Exterior paint peels faster, exposed metal fixtures rust within months, window seals degrade, and even vehicles parked outside suffer from accelerated undercarriage rust. These coastal living challenges require constant vigilance and a robust home maintenance budget.

| Maintenance Item | Typical Inland Lifespan | Expected Coastal Lifespan | Coastal Replacement Cost Impact |

|---|---|---|---|

| HVAC Condenser | 12–15 years | 5–8 years | High (Requires specialized coastal coatings) |

| Exterior Paint | 7–10 years | 3–5 years | Moderate (Requires frequent pressure washing and touch-ups) |

| Outdoor Metal Fixtures | 15+ years | 2–4 years | Low to Moderate (Must use marine-grade stainless steel) |

| Asphalt Shingle Roof | 20–25 years | 12–15 years | High (Subject to high wind degradation) |

Red Flag 3: Inadequate Specialized Healthcare Infrastructure

Idyllic beach communities often look perfect on paper until you experience a medical emergency. Many coastal towns are geographically isolated—situated on barrier islands, peninsulas, or at the end of long, two-lane highways. While these towns usually have an urgent care center to handle tourists’ sunburns and minor scrapes, they frequently lack comprehensive hospital systems and specialized geriatric care.

As you age, access to cardiologists, neurologists, and orthopedic specialists becomes paramount. If your chosen retirement destination requires a two-hour drive across a toll bridge to reach a major medical center, you are taking a significant risk. During the busy summer season, that two-hour drive can easily turn into a four-hour ordeal due to tourist traffic.

You must also verify how a relocation affects your health coverage. If you utilize a Medicare Advantage plan, moving to a new county or state means you will likely have to switch plans. Rural coastal counties often have fewer plan choices and narrower provider networks than major metropolitan areas. Before making any commitments, use the official Medicare Plan Finder to confirm that your preferred doctors are in-network and that specialized care is readily available.

Red Flag 4: The Transient Nature of the Neighborhood

A thriving community provides vital emotional support during retirement. Unfortunately, many picturesque beach towns are dominated by short-term vacation rentals. Purchasing a home in a neighborhood with a high density of Airbnb or VRBO properties introduces a host of quality-of-life issues.

Instead of building lasting relationships with neighbors who look out for one another, you may find yourself surrounded by a rotating cast of weekend vacationers. This transient environment often brings excessive noise, parking disputes, and a general lack of respect for community property. When winter arrives, the tourists leave, and those vibrant neighborhoods can quickly transform into dark, isolating ghost towns.

Before purchasing, investigate the local zoning laws and Homeowners Association (HOA) covenants. Communities that mandate minimum rental periods—such as 30 or 90 days—tend to foster a much more stable environment for full-time retirees.

Red Flag 5: The Physical Toll of Extreme Weather Evacuations

Preparing for a severe storm is exhausting work. Installing heavy storm shutters, securing outdoor furniture, sandbagging doors, and packing up your valuables requires a level of physical stamina that naturally diminishes as we age. In your sixties, boarding up windows might feel like a manageable chore; in your late seventies, it can become a dangerous physical strain.

Evacuation itself presents significant logistical hurdles. Securing hotel rooms inland, sitting in miles of gridlocked traffic, and dealing with the anxiety of not knowing if your home will survive takes a massive psychological toll. If your coastal retirement plan lacks a clear, realistic strategy for managing storm preparation and evacuation as your mobility decreases, you are ignoring one of the most critical coastal retirement warning signs.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

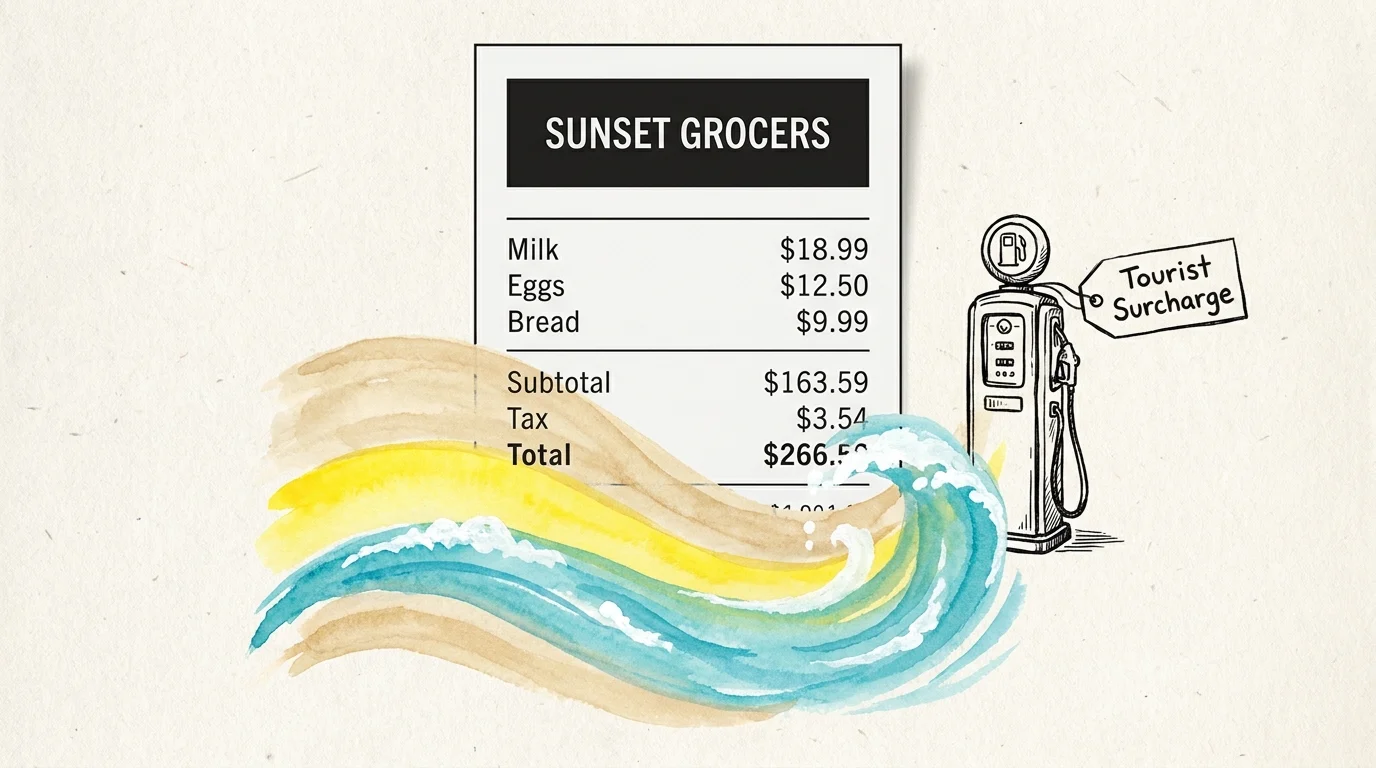

Red Flag 6: Surging Costs of Everyday Living

Beach towns are essentially captive markets. Transporting goods to coastal areas—especially islands—costs distributors more in fuel and logistics, and those expenses are passed directly to the consumer. You will likely notice that groceries, gasoline, and basic household supplies carry a noticeable markup compared to inland communities.

Furthermore, coastal municipalities rely heavily on property taxes and sales taxes to fund infrastructure projects, beach renourishment, and emergency services. As sea levels rise and infrastructure demands increase, local governments frequently levy special assessments or raise property taxes to cover the shortfalls. These rising costs can aggressively squeeze a fixed income, leaving less room for travel, hobbies, and leisure. For guidance on building a resilient retirement budget, the Consumer Financial Protection Bureau (CFPB) offers excellent resources for forecasting future expenses.

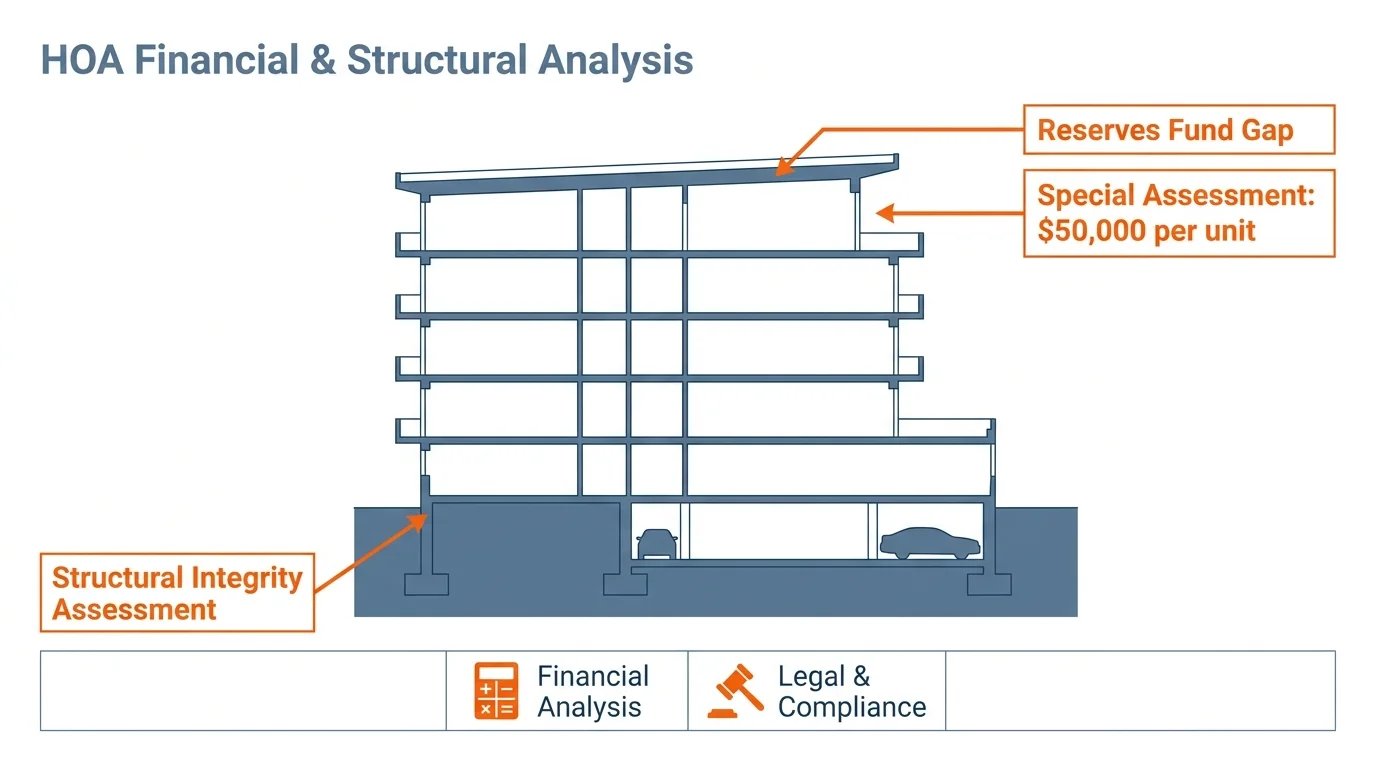

Red Flag 7: Looming HOA Financial Crises

Many retirees opt for coastal condominiums to avoid exterior maintenance, but this convenience often hides significant financial peril. Older beachfront condo buildings face intense structural wear and tear from constant salt exposure and extreme weather. If the HOA board has historically kept monthly dues artificially low by deferring necessary maintenance, a massive financial reckoning is inevitable.

Recent changes in state laws—particularly following building collapses—now require older condos to undergo rigorous structural inspections and fully fund their reserve accounts. If you buy into a building that has ignored these realities, you could be hit with a special assessment totaling tens of thousands of dollars just to repair balconies, roofs, or concrete pilings. Always demand the most recent reserve study and board meeting minutes before making an offer.

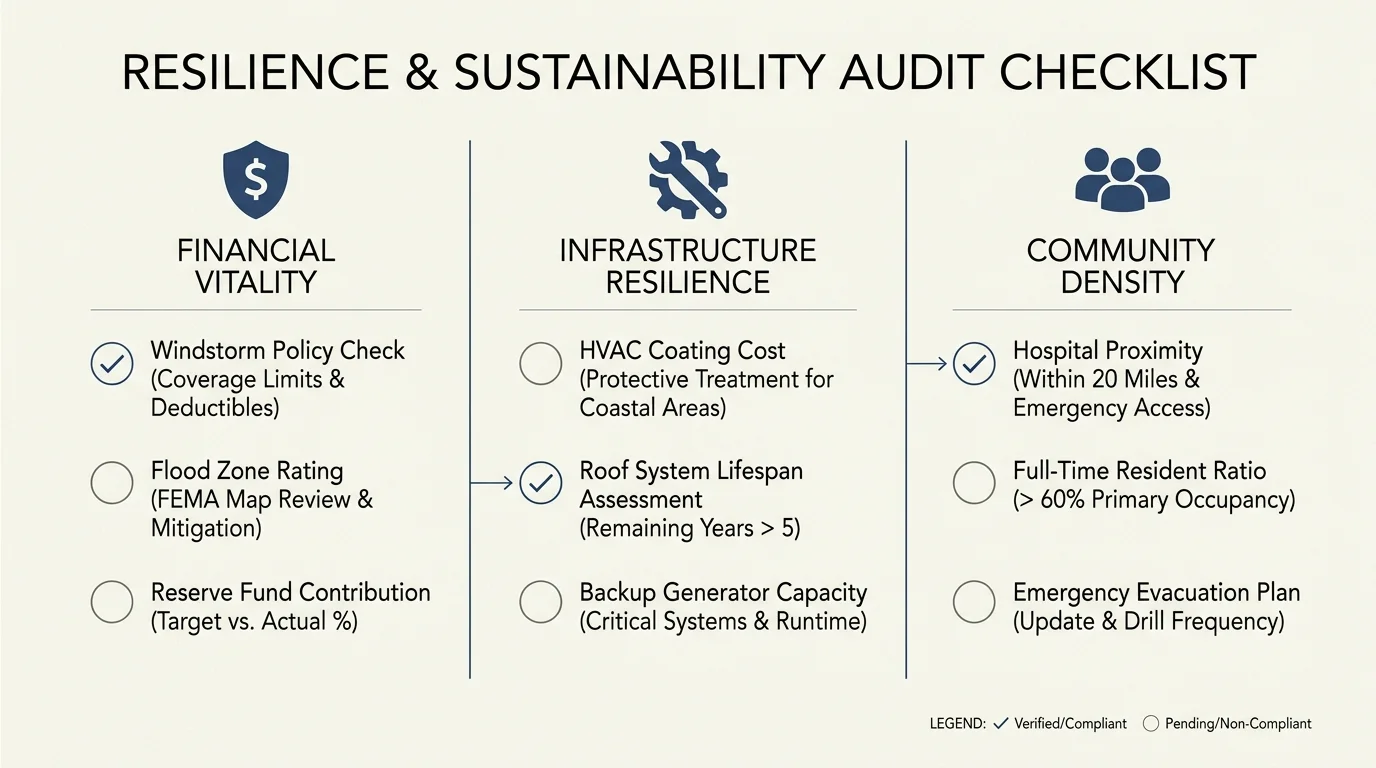

The Coastal Retirement Location Checklist

Before you commit to a beach town, evaluate the location using this practical retirement location checklist to ensure the area supports your long-term goals:

- Check the Evacuation Route: Drive the primary inland route during a busy weekend to gauge traffic flow and measure the distance to safe lodging.

- Audit Medical Facilities: Map the distance to the nearest Level 1 trauma center and confirm the presence of full-time specialists (cardiology, oncology, neurology) within a 30-minute drive.

- Review Insurance Availability: Call three independent insurance brokers to get written estimates for wind, flood, and primary homeowners coverage.

- Analyze Short-Term Rental Laws: Review municipal ordinances regarding vacation rentals to ensure your block won’t become a commercial hotel zone.

- Investigate Elevation: Use local topographical maps to verify the exact elevation of the property above sea level, as this dictates flood insurance requirements.

- Inspect HOA Health: For condos or managed communities, demand the last three years of budgets, reserve studies, and pending special assessment disclosures.

Don’t Make These Coastal Buying Mistakes

The enthusiasm of buying a beach house often overrides common sense. The single largest mistake prospective retirees make is buying a property based solely on their experiences during peak vacation season. Visiting a town in July tells you nothing about what the community feels like in dreary February.

Never purchase a permanent retirement home in a coastal community without renting there during the off-season first. Committing to a three-month winter rental allows you to experience the authentic daily life of a resident. You will discover which restaurants actually stay open, whether the local grocery store maintains its inventory, how harsh the winter winds can be, and what the local healthcare system looks like when it isn’t overwhelmed by tourists.

Another common misstep is underestimating the cost of bringing visitors to you. Many retirees move to the beach assuming their children and grandchildren will visit constantly. However, if the nearest major airport is three hours away and flights are expensive, your family may not visit as often as you envision, leading to unexpected feelings of isolation.

When Professional Advice Is Worth It

Relocating across state lines or shifting from a suburban to a coastal environment involves complex financial and healthcare logistics. This is a transition where professional guidance pays for itself.

A fiduciary financial advisor can stress-test your retirement portfolio against the higher inflation rates and insurance costs typical of coastal living. If you are navigating changes to your health coverage, reach out to your State Health Insurance Assistance Program (SHIP). These federally funded counselors provide free, unbiased guidance on navigating Medicare networks in your new zip code. You can find local aging resources and counselors through the Eldercare Locator.

Finally, consulting an elder law attorney in your destination state ensures your estate planning documents, advance directives, and power of attorney paperwork comply with local statutes, which vary significantly across jurisdictions.

Frequently Asked Questions About Beach Retirements

What are the hidden costs of coastal living?

Beyond standard living expenses, coastal residents must budget for accelerated maintenance due to salt air, specialized anti-corrosion HVAC systems, higher insurance premiums (including separate wind and flood policies), potential evacuation costs, and increased property tax assessments to fund municipal coastal infrastructure projects.

How does moving to the beach affect my Medicare coverage?

If you have Original Medicare (Parts A and B) paired with a standardized Medicare Supplement (Medigap) plan, your coverage travels with you to any doctor in the U.S. who accepts Medicare. However, if you have a Medicare Advantage (Part C) plan, you must live within the plan’s specific service area. Moving out of that area triggers a Special Enrollment Period, requiring you to select a new plan available in your coastal zip code.

Are property values in coastal towns beginning to drop due to climate risks?

The real estate market is highly localized. While high-demand luxury markets remain robust, some highly vulnerable, low-lying coastal areas are seeing slower appreciation and increased inventory as buyers become wary of exorbitant insurance costs and flood risks. Thoroughly researching historical price trends in your specific target neighborhood is essential.

Taking the time to evaluate these red flags doesn’t mean you must abandon your dream of living by the water; it simply means you are approaching the transition with your eyes wide open. Thorough preparation ensures you choose a community that offers true peace of mind rather than constant financial anxiety. Take the next step by drafting a preliminary coastal budget today, factoring in the inflated insurance and maintenance costs, to see how the numbers align with your projected income.

Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.