Stepping into retirement feels like landing in a foreign country where you thought you spoke the language, only to realize the daily rhythms are completely different. A stark retirement reality check waits for Americans transitioning from a structured career into an open-ended future. You might anticipate endless golf games, quiet mornings, and a permanently relaxed schedule, but unexpected retirement life requires active management of your identity, healthcare, and social networks. Navigating this shift takes more than just a robust savings plan. Understanding these surprise retirement truths early allows you to build a resilient, fulfilling second act that actually matches your evolving needs, replacing outdated expectations with practical, empowering realities.

1. The Loss of Professional Identity Hits Harder Than Anticipated

For decades, your job title served as a shorthand for your identity. When you meet someone new, the first question they ask is usually, “What do you do?” Answering that question with “I am retired” occasionally feels like stepping off a cliff without a parachute. Many successful professionals severely underestimate the psychological weight of losing their daily purpose, influence, and structured environment.

Without a defined role, days can blur together into an unfulfilling stretch of free time. The solution requires proactive reinvention. Treat your transition not as an ending, but as a pivot toward activities that provide intrinsic value rather than external validation. You need daily routines that challenge your intellect and keep you engaged with the community around you. Whether you mentor young professionals, start a small consulting business, or dedicate yourself to a long-delayed passion project, establishing a new core identity protects your mental health during this vulnerable transition period.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

2. Medicare Is Far More Complex Than Simply Turning 65

A common retirement expectation versus reality involves healthcare coverage. Many Americans assume that turning 65 means a seamless, cost-free transition into government-provided healthcare. The reality involves a labyrinth of enrollment windows, coverage gaps, and ongoing premium costs that catch even diligent planners off guard.

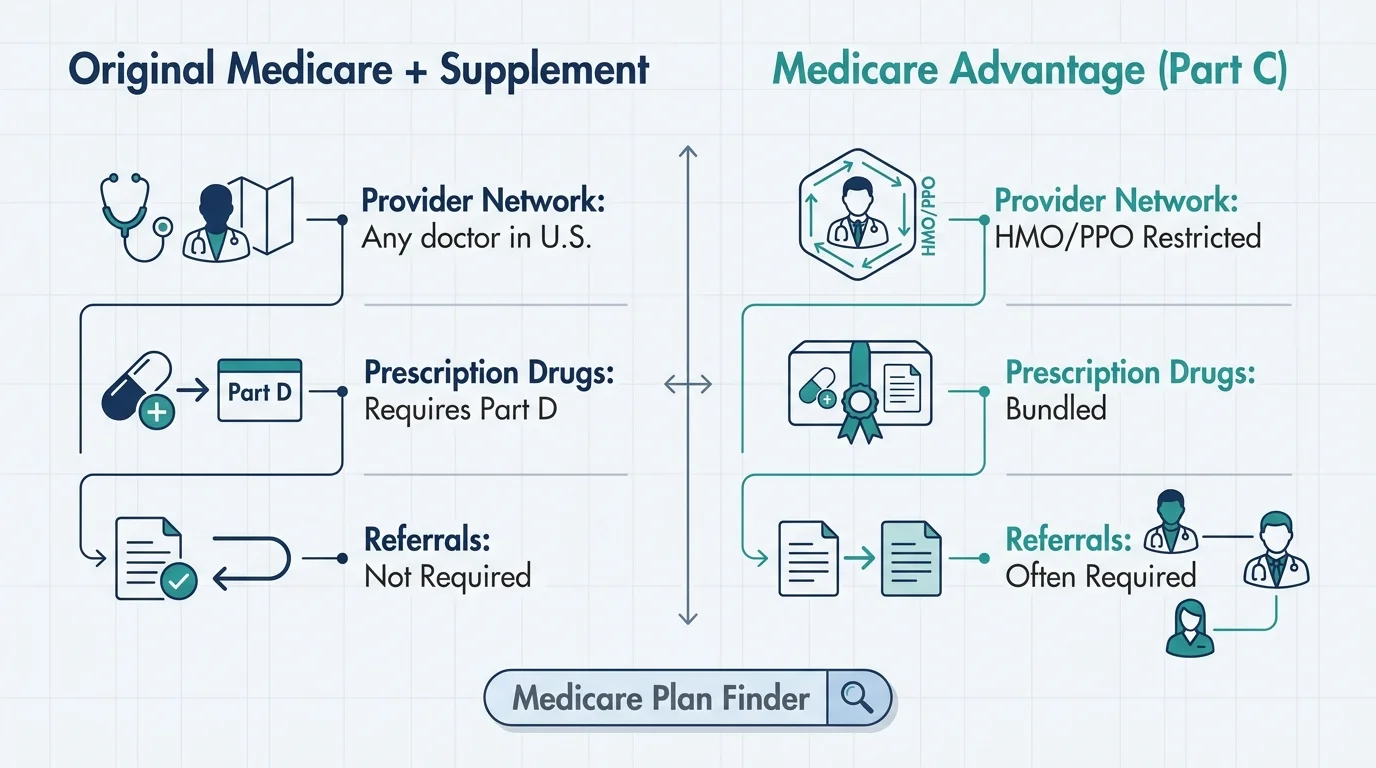

Medicare does not cover everything. You still face premiums for Part B, potential surcharges based on your income (IRMAA), deductibles, and co-pays. Furthermore, dental, vision, and long-term care fall outside traditional Medicare coverage entirely. Choosing between Original Medicare with a Supplement plan and a Medicare Advantage plan dictates your healthcare access and costs for the rest of your life. Navigating this successfully requires thorough research and a clear understanding of your personal medical needs.

| Coverage Feature | Original Medicare (Parts A & B) + Supplement | Medicare Advantage (Part C) |

|---|---|---|

| Provider Network | Any doctor or hospital in the U.S. that accepts Medicare. | Restricted to HMO or PPO networks; out-of-network costs more. |

| Out-of-Pocket Limits | No built-in limit, but Medigap policies cover most leftover costs. | Annual out-of-pocket maximum protects against catastrophic costs. |

| Prescription Drugs | Requires purchasing a separate Part D standalone plan. | Often bundled directly into the Advantage plan. |

| Referrals to Specialists | Not required. You can see specialists directly. | Often required by the primary care physician. |

Before you make a final decision, use the official Medicare Plan Finder to compare estimated annual costs based on the specific medications you currently take.

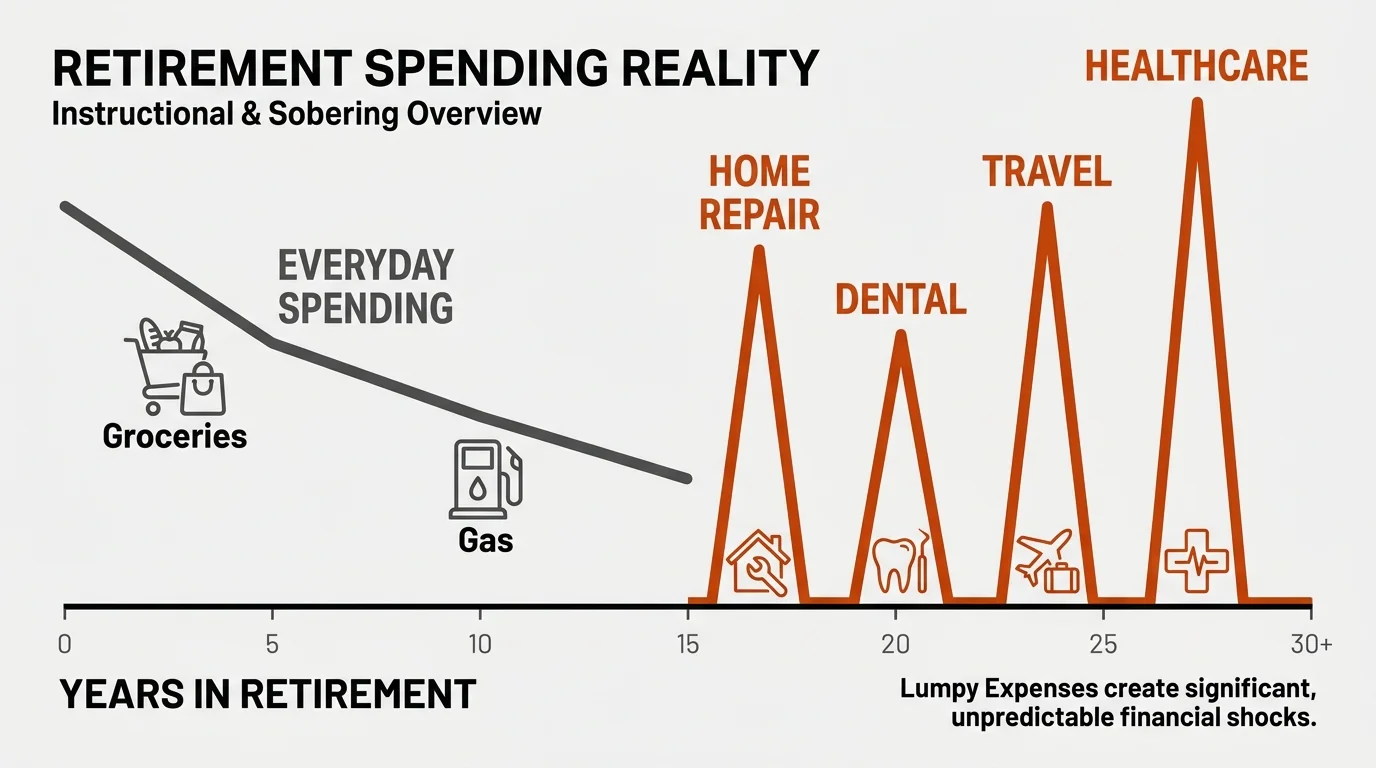

3. Everyday Spending Drops, But “Lumpy” Expenses Skyrocket

Financial planners often suggest that you will need 70 to 80 percent of your pre-retirement income to maintain your lifestyle. While commuting costs, dry cleaning, and payroll taxes vanish, other expenses expand to fill the void. Retirees frequently encounter what economists call “lumpy” expenses—irregular, large-ticket costs that disrupt monthly cash flow.

During your initial “go-go” years, travel budgets often triple as you finally take the trips you delayed during your working years. You also spend significantly more time in your home, which accelerates the realization that you need a new roof, an updated HVAC system, or a remodeled kitchen. Furthermore, out-of-pocket medical events—such as unexpected dental implants or hearing aids—can wipe out a month’s cash flow in a single afternoon. Maintaining a dedicated emergency fund, completely separate from your daily checking account, remains just as vital in retirement as it was during your career.

4. Social Connections Require Intentional Daily Effort

The workplace provides a built-in social network. You chat by the coffee machine, collaborate on projects, and share frustrations with colleagues. Once you leave that environment, your social circle shrinks dramatically unless you actively maintain it. The National Institute on Aging warns that social isolation represents a severe health risk for older adults, comparable to smoking or obesity.

Do not wait for people to invite you out. You must become the organizer. Schedule weekly breakfasts with former colleagues, join local hobby groups, or volunteer at community organizations. Many retirees find deep satisfaction in structured volunteer work because it provides social interaction, a predictable schedule, and a renewed sense of purpose. Building a new, localized network of friends outside of your previous career takes time, but it serves as the foundation for a vibrant retirement.

5. The “Honeymoon Phase” Fades After the First Year

When you first step away from your career, retirement feels like an extended, glorious vacation. You sleep in, tackle projects around the house, and enjoy the sheer lack of deadlines. Psychologists call this the “honeymoon phase.” However, this euphoria rarely lasts longer than a year. Once the novelty of having nothing to do wears off, a period of disenchantment frequently sets in.

Surviving this dip requires establishing a new baseline routine. Humans thrive on rhythm and predictability. Structure your weeks to include specific days for fitness, socializing, household management, and personal hobbies. Setting micro-goals—such as learning a new language, mastering a specific cooking technique, or walking a certain number of miles each week—gives your days shape and prevents the malaise that stems from endless, unstructured time.

6. Couples Must Renegotiate Their Shared Space and Time

If you and your spouse both retire, you suddenly face an extra 40 to 50 hours a week in each other’s presence. The dynamic shift can strain even the strongest marriages. One spouse may expect to spend all their free time together, while the other desperately craves independent activities. Small quirks that previously went unnoticed suddenly become daily irritations when you occupy the same house 24/7.

Successful retired couples explicitly discuss their boundaries. You do not need to eat every meal together or share every hobby. Give each other permission to maintain independent friendships and solitary routines. Having separate spheres of interest actually gives you more to talk about when you reconvene at the end of the day. Treat this new phase of your relationship as a partnership that requires conscious recalibration.

7. Housing Needs Shift Toward Accessibility, Not Just Downsizing

Many pre-retirees assume they will sell their large family home and buy a smaller condo to reduce maintenance. However, the reality of aging demands a focus on accessibility rather than just square footage. A smaller home with a steep driveway, narrow hallways, and a second-floor master bedroom quickly becomes a physical burden.

If you plan to age in place, evaluate your current or future home through the lens of universal design. Look for single-story living, walk-in showers with grab bars, lever-style door handles, and ample task lighting. Addressing these physical needs early prevents forced relocations during a health crisis. For guidance on modifying your home or finding appropriate community resources, the National Council on Aging (NCOA) provides excellent checklists for maintaining independence safely.

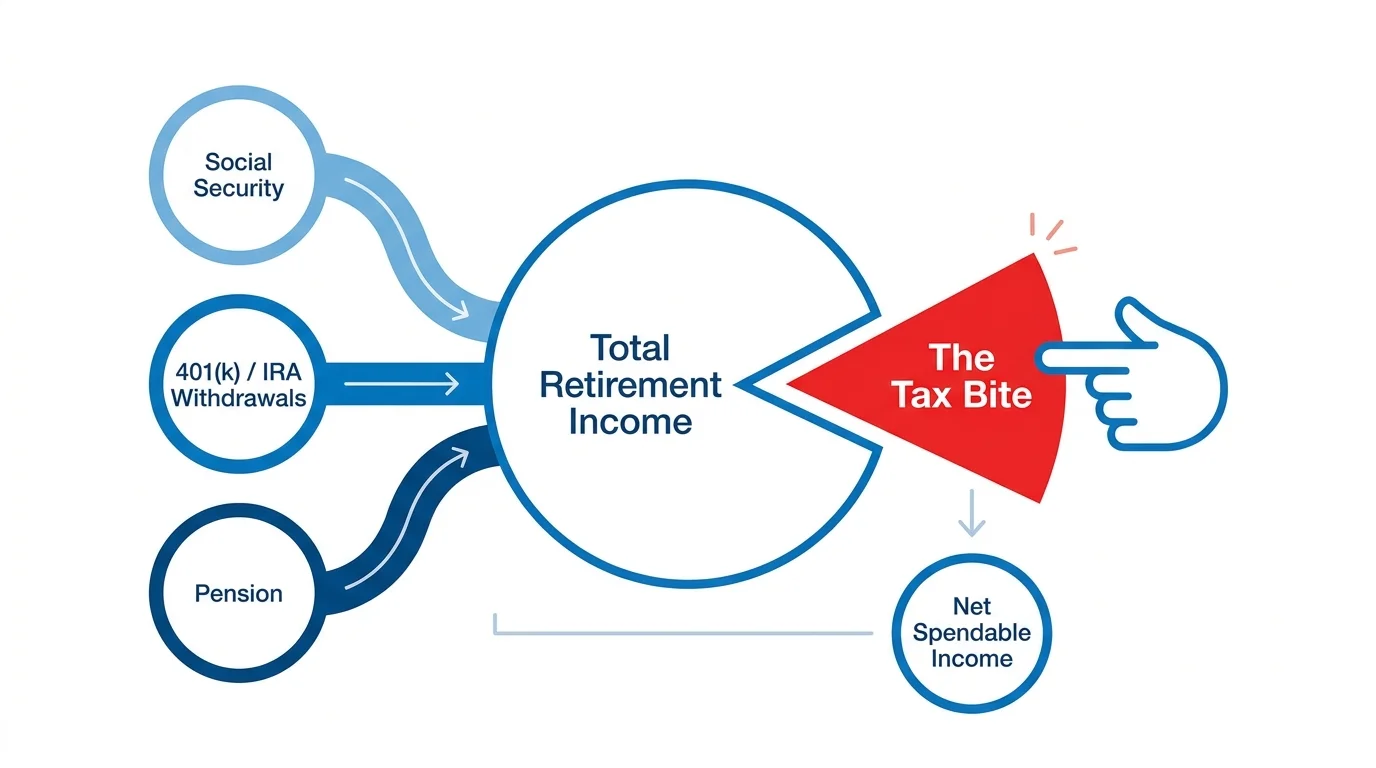

8. Taxes Do Not Disappear Once You Stop Working

One of the harshest surprise retirement truths is the realization that the IRS still demands a sizable cut of your income. Depending on your combined income, up to 85 percent of your Social Security benefits may be subject to federal income tax. Furthermore, every dollar you pull from a traditional 401(k) or IRA gets taxed as ordinary income.

As you reach your 70s, Required Minimum Distributions (RMDs) force you to withdraw specific amounts from your pre-tax accounts, whether you need the money or not. These forced withdrawals can push you into a higher tax bracket and trigger Medicare premium surcharges. Strategic tax planning—such as executing Roth conversions during low-income years prior to taking Social Security—can save you tens of thousands of dollars over your lifetime. Proactive tax management shifts from a once-a-year April annoyance to a year-round strategic necessity.

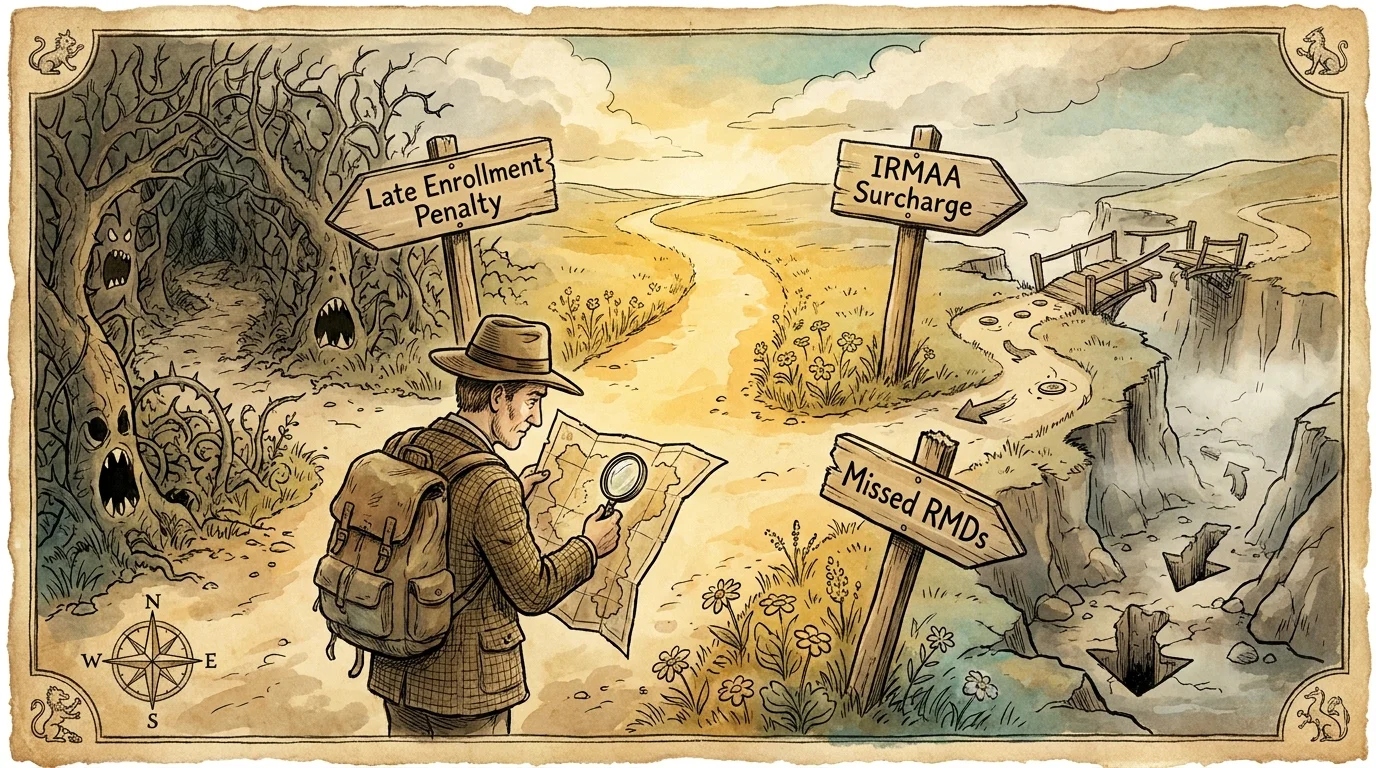

Errors That Cost Retirees Thousands

Navigating the transition out of the workforce involves making irrevocable decisions. A single misstep regarding benefits or investments can permanently lower your standard of living. Avoid these common, costly mistakes:

- Missing Your Medicare Initial Enrollment Period: If you fail to sign up for Medicare Part B when you are first eligible (and do not have qualifying employer coverage), you face a permanent late enrollment penalty that increases your monthly premiums for the rest of your life.

- Claiming Social Security Blindly: Filing for Social Security exactly at age 62 permanently reduces your monthly check by up to 30 percent compared to waiting for your Full Retirement Age. Use the Social Security Retirement Estimator to map out the exact breakeven points for your specific claiming strategy.

- Investing Too Conservatively: Shifting your entire portfolio into cash and bonds the day you retire exposes you to massive inflation risk. A 30-year retirement requires a growth component to ensure your purchasing power keeps pace with the rising cost of living.

- Ignoring Long-Term Care Risks: Assuming that Medicare or standard health insurance will pay for a nursing home or an in-home aide leaves your family financially vulnerable. Medicare only pays for short-term, rehabilitative care, not chronic custodial care.

When to Get Expert Help

You do not have to untangle the complexities of retirement alone. Because the stakes are so high, consulting with specialized professionals often yields a massive return on investment. Consider engaging an expert in the following scenarios:

Work with a fiduciary financial advisor three to five years before your target retirement date. They help you run cash flow projections, determine a safe withdrawal rate, and create a tax-efficient strategy for tapping your various accounts. Ensure the advisor operates strictly as a fiduciary, meaning they are legally obligated to put your financial interests above their own commissions.

Engage a State Health Insurance Assistance Program (SHIP) counselor when you approach age 65. These federally funded, unbiased counselors help you decode the overwhelming pile of Medicare marketing materials. They provide free, localized advice to help you select a plan that covers your specific doctors and prescriptions.

Finally, consult an elder law attorney to establish your durable power of attorney, advance healthcare directives, and estate plan. Having legally binding documents in place ensures your wishes are respected and protects your family from agonizing decisions if you experience a severe medical event.

Frequently Asked Questions

How long does it typically take to adjust to retirement?

Psychologists and retirement coaches suggest that it takes between one and three years to fully adjust to retirement. The first year is often dominated by the “honeymoon phase” of relaxation and travel, followed by a period of disorientation. By the third year, most retirees have established a fulfilling daily routine, a solid social network, and a comfortable financial rhythm.

Is it normal to feel depressed or anxious after retiring?

Yes, experiencing a sense of grief, anxiety, or mild depression is entirely normal. You are mourning the loss of your professional identity, your work-based friendships, and your structured routine. Acknowledge these feelings rather than burying them. If feelings of sadness persist or interfere with your ability to enjoy daily life, speaking with a therapist who specializes in life transitions provides vital support.

What is the most common unexpected expense in retirement?

Healthcare costs, specifically out-of-pocket dental work, hearing aids, and long-term care, frequently shock new retirees. Additionally, home maintenance spikes as aging housing systems require replacement. Retirees also frequently underestimate how much they will spend on travel and dining out during their initial active years.

Can I work part-time without losing my Social Security benefits?

Yes, but the rules depend on your age. If you have reached your Full Retirement Age (FRA), you can earn unlimited income without any reduction in your Social Security benefits. However, if you claim benefits before your FRA and continue working, the Social Security Administration will temporarily withhold a portion of your benefits if your earnings exceed a specific annual limit. Once you reach FRA, your monthly benefit is recalculated upward to account for the months benefits were withheld.

Your retirement journey belongs entirely to you. By discarding outdated expectations and confronting the realities of healthcare, taxes, and daily purpose head-on, you position yourself to thrive. Take an hour this week to evaluate your current trajectory; map out your intended daily routines and review your healthcare options. Active preparation today guarantees peace of mind tomorrow.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.