Claiming Social Security too early costs the average American household tens of thousands of dollars in lifetime income. The choices you make at the claiming window are largely irrevocable, locking you into a financial reality for the rest of your retirement. Many retirees look back with regret, wishing they had understood the long-term impact of their choices before filing the paperwork. By examining the actual missteps of those who have already navigated the system, you can protect your future income stream. From misunderstanding spousal benefits to ignoring the tax implications of working while claiming, these real-world lessons offer a roadmap for maximizing your payout. Learn from their hindsight to secure the foundation of your financial independence.

Mistake 1: Claiming at 62 Because “Tomorrow Isn’t Promised”

The earliest age you can claim Social Security retirement benefits is 62. For many people, the temptation to start collecting a check immediately is overwhelming. Human nature drives us to take cash in hand rather than wait for a larger future payout. Retirees often justify this decision by citing their health, family longevity, or a general distrust in the government’s ability to maintain the program.

While the fear of passing away before collecting your “fair share” is entirely valid, making a purely emotional decision ignores the mathematical reality of longevity risk. If you make it to age 65 in reasonably good health, statistical averages dictate you will likely live into your mid-80s. When you claim at 62, you accept a permanent reduction in your monthly benefit—up to 30% compared to waiting for your Full Retirement Age (FRA). Worse, you forfeit the delayed retirement credits that increase your benefit by 8% for every year you delay past your FRA up to age 70.

Consider the impact on a hypothetical monthly benefit. The table below illustrates how drastically your claiming age alters your permanent baseline income, assuming a Full Retirement Age of 67 and an unreduced benefit of $2,000 per month.

| Claiming Age | Percentage of Full Benefit | Monthly Payout | Annual Income |

|---|---|---|---|

| Age 62 | 70% | $1,400 | $16,800 |

| Age 67 (FRA) | 100% | $2,000 | $24,000 |

| Age 70 | 124% | $2,480 | $29,760 |

Retirees who claimed at 62 frequently report feeling the financial squeeze in their late 70s and 80s. As inflation degrades purchasing power and out-of-pocket medical expenses climb, that permanently reduced check fails to keep up. Before filing early, consult the Social Security Administration (SSA) calculators to determine your specific break-even point—the age at which delaying benefits results in more total lifetime wealth. For most healthy adults, that break-even age lands between 78 and 82.

Mistake 2: Failing to Coordinate Spousal and Survivor Benefits

Married couples face a complex set of claiming strategies. A common and catastrophic error occurs when both spouses view their Social Security decisions in a vacuum, focusing solely on their individual benefit amounts. This oversight ignores the powerful survivor benefit rules built into the system.

When one spouse passes away, the surviving spouse inherits the larger of the two Social Security checks, and the smaller check disappears. Therefore, the claiming decision of the higher earner permanently dictates the maximum income available to the surviving widow or widower.

Imagine a couple, Robert and Susan. Robert is the primary earner. Tired of the corporate grind, he retires and claims Social Security at 62, accepting a 30% reduction. Susan has a smaller earnings history. Years later, Robert passes away. Susan’s survivor benefit is now permanently capped at Robert’s reduced rate. By claiming early, Robert essentially took a pay cut that his wife will have to live with for the rest of her life.

Retirees often wish they had coordinated their strategy by having the lower earner claim early to bring income into the household, while the higher earner delays until age 70. This approach maximizes the guaranteed, inflation-protected survivor benefit. Ensuring your spouse is financially secure after you are gone is one of the most compelling reasons to delay the higher earner’s claim.

Mistake 3: Triggering the Earnings Test and Tax Traps

Retirement is no longer a hard stop at age 65. Many Americans transition into consulting, part-time work, or gig economy roles. A shocking number of early claimants discover too late that working while drawing Social Security before Full Retirement Age carries severe financial penalties.

If you claim benefits before your FRA and continue to work, you will run into the Retirement Earnings Test. The SSA sets an annual earnings limit. If your earned income exceeds this threshold, the government withholds $1 in benefits for every $2 you earn above the limit. In the year you reach FRA, the rules are slightly more lenient, withholding $1 for every $3 earned, up to the month your birthday occurs. Once you reach Full Retirement Age, the earnings test disappears entirely, and you can earn millions without a single dime being withheld from your Social Security check.

The withheld money is not gone forever—the SSA recalculates your benefit once you reach FRA to account for the withheld months, slightly increasing your future checks. However, retirees relying on that immediate cash flow are often blindsided when their monthly deposits suddenly stop.

Beyond the earnings test, retirees frequently stumble into the “tax torpedo.” Social Security benefits are subject to federal income tax based on a formula called “provisional income.” To calculate your provisional income, add the following together:

- Your Adjusted Gross Income (AGI), which includes wages, pensions, and traditional IRA withdrawals

- Any non-taxable interest (such as municipal bond interest)

- 50% of your Social Security benefits

If your provisional income exceeds certain IRS thresholds, up to 85% of your Social Security benefits become taxable. Retirees who pull large sums from traditional 401(k)s or sell significant assets often inflate their provisional income, unexpectedly forcing their Social Security benefits into a taxable bracket. Careful tax planning—such as utilizing Roth IRA conversions in your early 60s—can help mitigate this burden.

Mistake 4: Assuming Social Security Will Cover Everything

Social Security was designed to replace roughly 40% of the average worker’s pre-retirement income. It was never intended to be the sole source of funding for your golden years. Yet, a substantial portion of Americans enter their 60s relying almost entirely on this single income stream.

Retirees who lean entirely on the government program often face a harsh awakening regarding healthcare costs. Medicare Part B premiums are deducted directly from your Social Security check. When the government announces an annual Cost of Living Adjustment (COLA) for Social Security, Medicare premiums typically rise in tandem. Often, the increase in Medicare costs absorbs the majority of the COLA increase, leaving your net check practically unchanged despite soaring grocery and utility bills.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

To avoid this trap, you must cultivate multiple streams of income. Treat Social Security as the foundation of your house, not the entire structure. Pensions, annuities, investment portfolios, Health Savings Accounts (HSAs), and part-time work provide the walls and roof required to weather economic storms. Organizations like the AARP provide excellent resources for evaluating your entire financial landscape rather than viewing your government benefits in isolation.

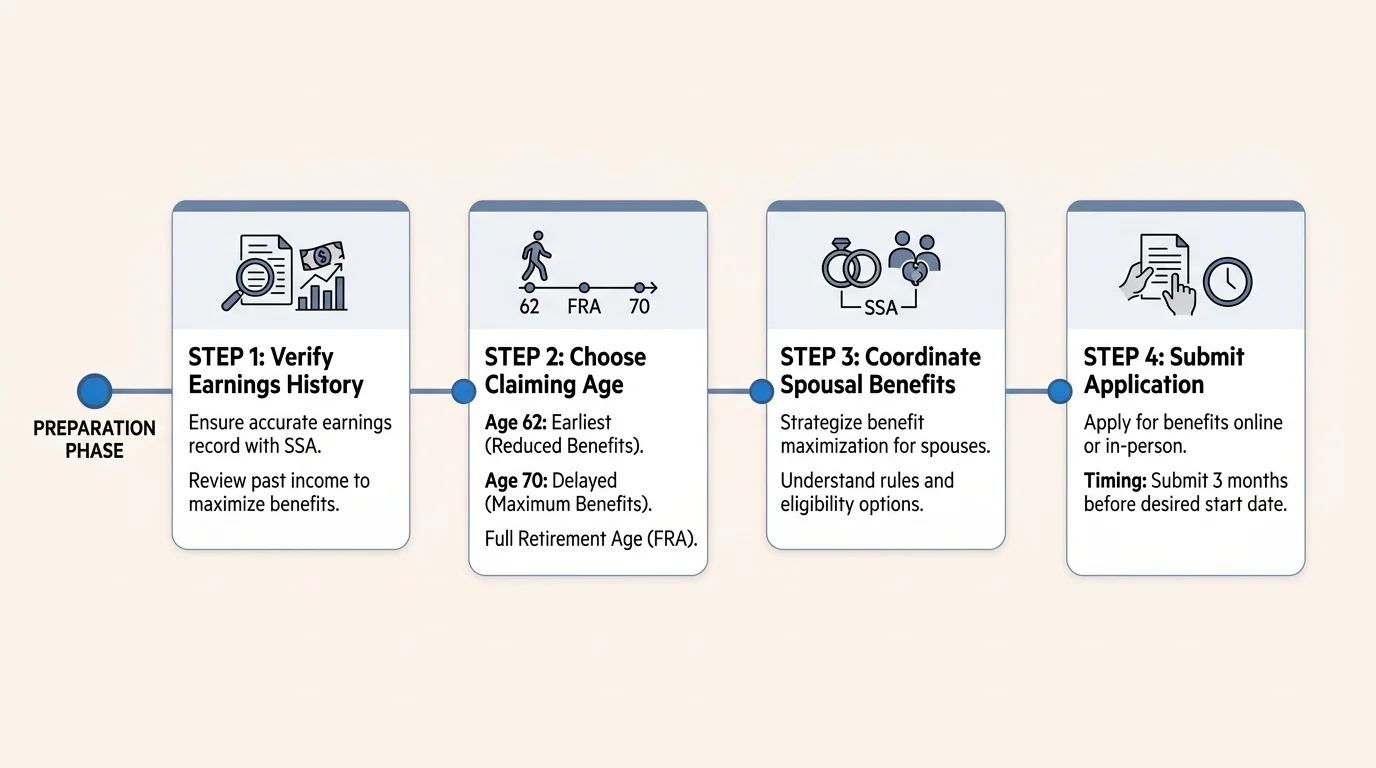

Costly Mistakes to Avoid During the Application Process

Beyond the grand strategies of when to claim, retirees frequently stumble over administrative hurdles that cost them dearly. Avoid these procedural errors as you approach your filing date:

Failing to verify your earnings record. Your benefit amount relies entirely on your highest 35 years of indexed earnings. If the SSA has incorrect data—perhaps a former employer failed to report income, or a name change confused the system—your payout will shrink. Create a “my Social Security” account online and review your annual earnings statement. Correcting errors is much easier while you still have the W-2s and tax returns, rather than attempting to prove your income three decades later.

Failing to claim eligible ex-spouse benefits. If you were married for at least 10 years, have been divorced for at least two years, and are currently unmarried, you might be entitled to benefits based on your ex-spouse’s work record. Claiming this benefit has zero impact on your ex-spouse or their new partner. Many divorced retirees leave money on the table simply because they prefer not to reopen old wounds or remain unaware of the rule.

Messing up Medicare timing. While full retirement age for Social Security varies, Medicare eligibility begins strictly at age 65 for most Americans. If you delay Social Security past 65, you must still proactively enroll in Medicare. Missing your Initial Enrollment Period can trigger lifetime late enrollment penalties and leave you exposed to devastating medical bills.

Don’t DIY These Decisions

Social Security claiming strategies represent a high-stakes puzzle with irreversible consequences. While educating yourself is critical, executing the plan without professional oversight is risky. The rules governing survivor benefits, Government Pension Offsets (GPO), and the Windfall Elimination Provision (WEP) are notoriously opaque.

If you have a complex scenario—such as a pension from employment that did not pay into Social Security, multiple marriages, a disabled child, or a massive age gap between spouses—seek expert guidance. Consult a fiduciary financial advisor or a specialized Social Security claiming strategist. Additionally, you can utilize free resources provided by the Consumer Financial Protection Bureau (CFPB) to map out your retirement timelines. Paying a professional for a few hours of tactical planning often yields tens of thousands of dollars in optimized lifetime benefits.

Frequently Asked Questions About Social Security Claims

Can I change my mind after I claim Social Security?

Yes, but you only get one chance. If you claim benefits and regret it, you can execute a “Withdrawal of Application” within the first 12 months of your claim. However, you must repay every cent you and your family received during that time, including Medicare premiums deducted from your checks. Once the 12-month window closes, your decision is largely permanent.

Does my ex-spouse claiming benefits reduce my own payout?

No. If your ex-spouse claims a divorced spousal benefit based on your earnings record, it does not reduce your benefit, nor does it reduce the benefit of your current spouse if you have remarried.

What is the maximum Social Security benefit possible?

The maximum benefit changes annually. To reach the absolute maximum, a worker must earn at or above the Social Security wage base limit for at least 35 years and delay claiming until age 70. For context, the maximum monthly benefit for someone retiring at age 70 in 2024 was nearly $4,873, though extremely few workers qualify for this amount.

Securing Your Retirement Future

Navigating the Social Security landscape requires a blend of mathematical analysis and honest self-assessment. Take the time to project your long-term needs, coordinate with your spouse, and account for the taxation of your benefits. Do not let the fear of the unknown push you into a hasty, irreversible decision at age 62. Download your earnings statement today, run the calculators, and map out a strategy that protects your purchasing power into your 80s and beyond. Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: July 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.