Leaving your career for a sunny beach sounds like the perfect reward, but the reality of retirement frequently involves unexpected plot twists. From fluctuating healthcare costs to the emotional toll of an empty calendar, popular retirement expectations often clash with reality and lead to frustrating retirement regrets. Many well-intentioned strategies—like downsizing to save cash or assuming you will easily find part-time work—frequently fall short. Recognizing these common retirement planning errors before you hand in your notice allows you to pivot and protect your nest egg. By examining where standard plans go wrong, you can construct a resilient lifestyle that thrives even when your roadmap takes a sudden detour.

1. Assuming Downsizing Will Instantly Slash Your Expenses

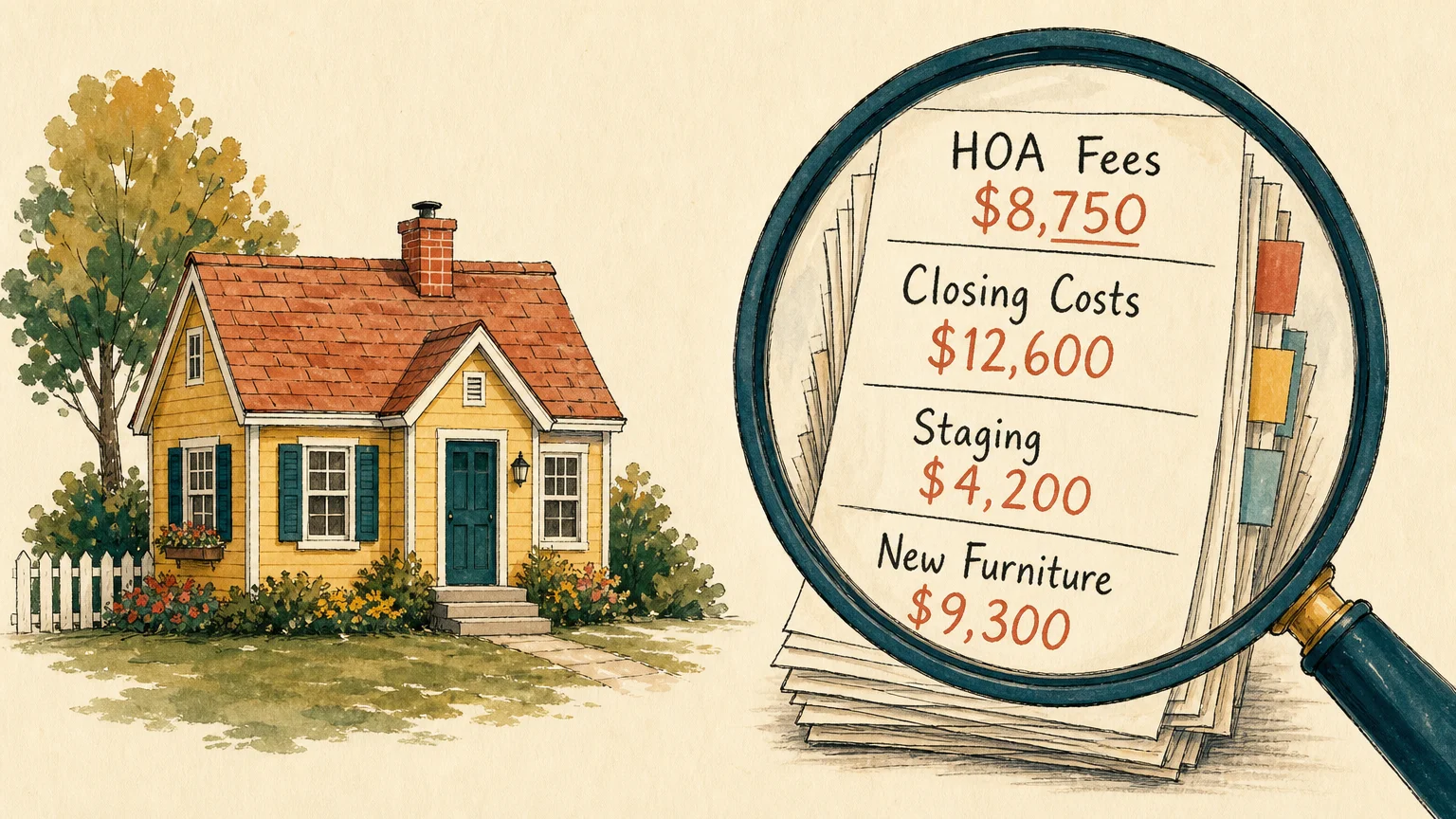

Trading your four-bedroom family house for a sleek two-bedroom condo seems like a foolproof way to unlock equity and reduce your monthly bills. In theory, a smaller footprint means lower utility bills, reduced property taxes, and a hefty deposit into your brokerage account. The reality of downsizing often proves far more complicated and expensive than retirees anticipate.

Preparing a home for top-dollar sale requires upfront cash for repairs, staging, and painting. Once you sell, you lose a significant percentage to real estate commissions, closing costs, and moving expenses. If you relocate to a 55-plus community or a maintenance-free condominium, hefty Homeowners Association (HOA) fees can quickly consume the money you saved on property taxes. Furthermore, replacing your current furniture to fit a smaller floor plan requires a surprisingly large budget.

The better approach: Run a comprehensive break-even analysis before planting a “For Sale” sign in your yard. Calculate exactly how much cash you will walk away with after all transaction costs, and compare your current annual housing expenses against the projected costs of your new location—including those unpredictable HOA assessments.

2. Planning to Work Part-Time on Your Own Terms

Many pre-retirees envision a smooth transition into their golden years by leaving their stressful corporate roles to consult, freelance, or work a low-stress job at a local garden center. This phased approach to retirement sounds brilliant for supplementing your income while maintaining a sense of purpose.

Unfortunately, the job market does not always cooperate with your retirement lifestyle. Age discrimination, while illegal, remains a stubborn barrier in the hiring process. You might also find that “low-stress” retail or service jobs require long hours on your feet, which can aggravate physical ailments. Beyond market factors, life events frequently intervene; you might need to stop working entirely to care for an ailing spouse or manage your own sudden health crisis.

The better approach: Treat projected part-time income as a bonus rather than a load-bearing pillar of your financial plan. Secure your foundational expenses using guaranteed income sources like Social Security, pensions, and conservative portfolio withdrawals.

3. Expecting Medicare to Cover Every Medical Need

Transitioning to Medicare at age 65 provides vital health security, but assuming this federal program functions like an all-inclusive platinum corporate health plan is one of the most dangerous retirement planning errors you can make.

Original Medicare (Parts A and B) covers hospital stays and outpatient care, but it features substantial gaps. It does not cover routine dental exams, cleanings, extractions, or dentures. It excludes routine vision care and hearing aids—all of which become increasingly necessary as you age. Most critically, Medicare does not pay for long-term custodial care, such as assistance with bathing, dressing, or extended stays in an assisted living facility. Relying on Medicare to fund a potential multi-year stay in a nursing home will rapidly drain your life savings.

The better approach: Budget specifically for healthcare premiums, deductibles, and out-of-pocket costs. Utilize the official Medicare website to compare Medigap policies or Medicare Advantage plans that can help cap your out-of-pocket expenses. Additionally, build a distinct strategy for funding potential long-term care, whether through insurance products, hybrid life policies, or dedicated savings.

4. Relocating Hundreds of Miles Away for Lower Taxes

Fleeing a high-tax state for a region with zero state income tax is a classic retirement move. Chasing tax efficiency makes mathematical sense, but uprooting your life solely for tax benefits often results in deep personal dissatisfaction.

States with no income tax must generate revenue elsewhere. You might escape state income taxes only to face astronomical property taxes, exorbitant sales taxes, or high vehicle registration fees. Financial considerations aside, the social cost of moving frequently derails this plan. Leaving behind decades-long friendships, trusted doctors, and your established community can lead to profound isolation. If your children and grandchildren live in your home state, you will likely spend the money you saved on taxes on expensive, exhausting flights back and forth to visit them.

The better approach: Rent a home in your desired tax-friendly state for three to six months during the worst weather season before making a permanent move. Test the local healthcare infrastructure, build a preliminary social network, and determine if the tax savings genuinely justify the disruption to your life.

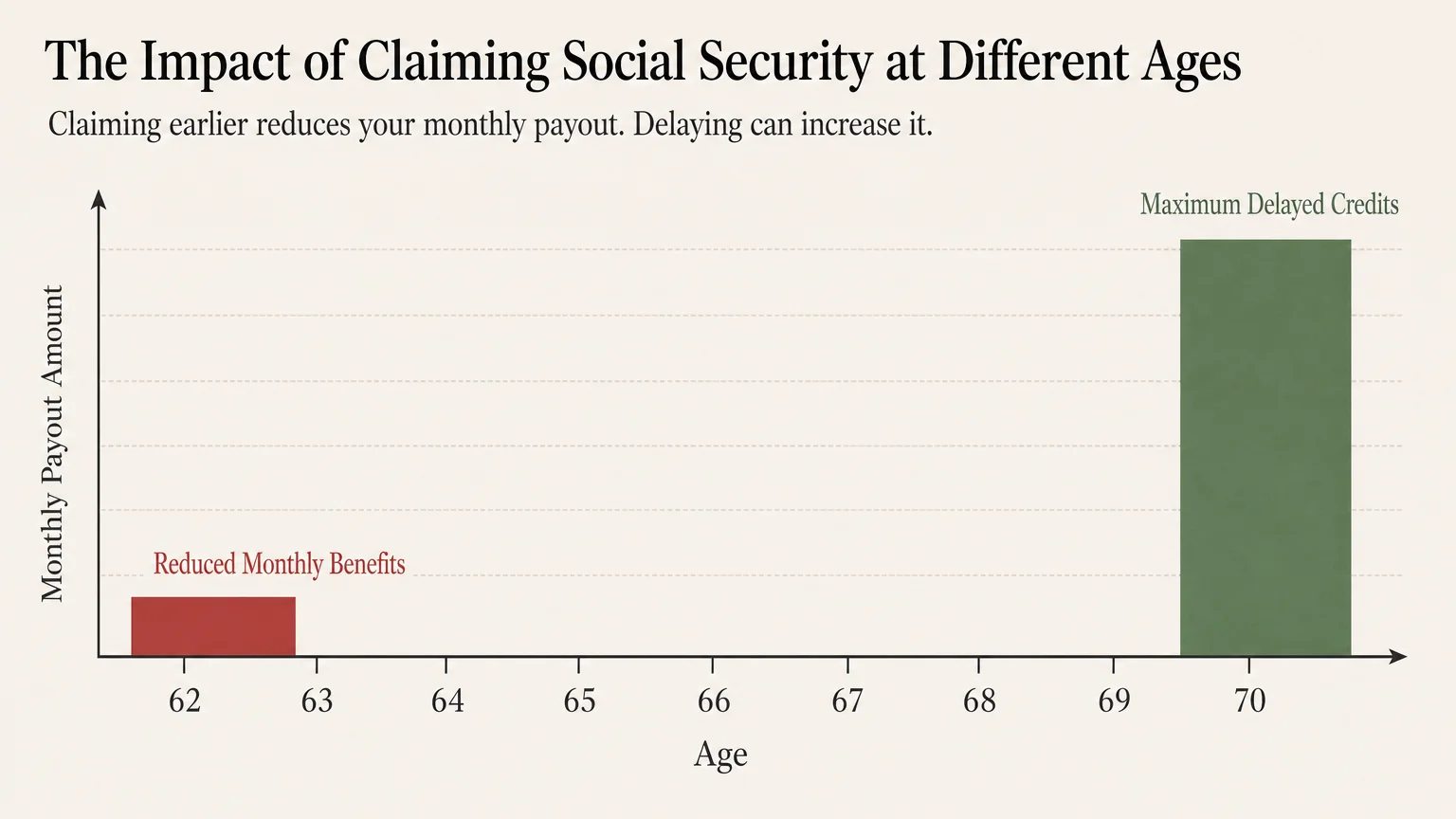

5. Claiming Social Security Early to “Outsmart” the System

Many retirees rush to claim Social Security at age 62, operating under the fear that the system will go bankrupt or believing they can invest the early payments and beat the government’s math. While claiming early is sometimes necessary due to health or job loss, doing it simply to outsmart the system frequently backfires.

When you claim at 62, you lock in a permanent reduction in your monthly benefit—up to 30% less than what you would receive at your Full Retirement Age (FRA). Furthermore, for every year you delay claiming past your FRA up to age 70, your benefit increases by a guaranteed 8% annually. In today’s volatile financial markets, finding a guaranteed, risk-free 8% return is virtually impossible. Investing early benefits rarely overcomes this mathematical hurdle, especially when factoring in the sequence of returns risk during market downturns.

The better approach: Evaluate your longevity history and portfolio strength. If you are in good health, tapping your investments early to allow your Social Security benefit to grow until age 70 often provides superior long-term protection against inflation and longevity risk. Use the Social Security Retirement Estimator to calculate your exact payout scenarios.

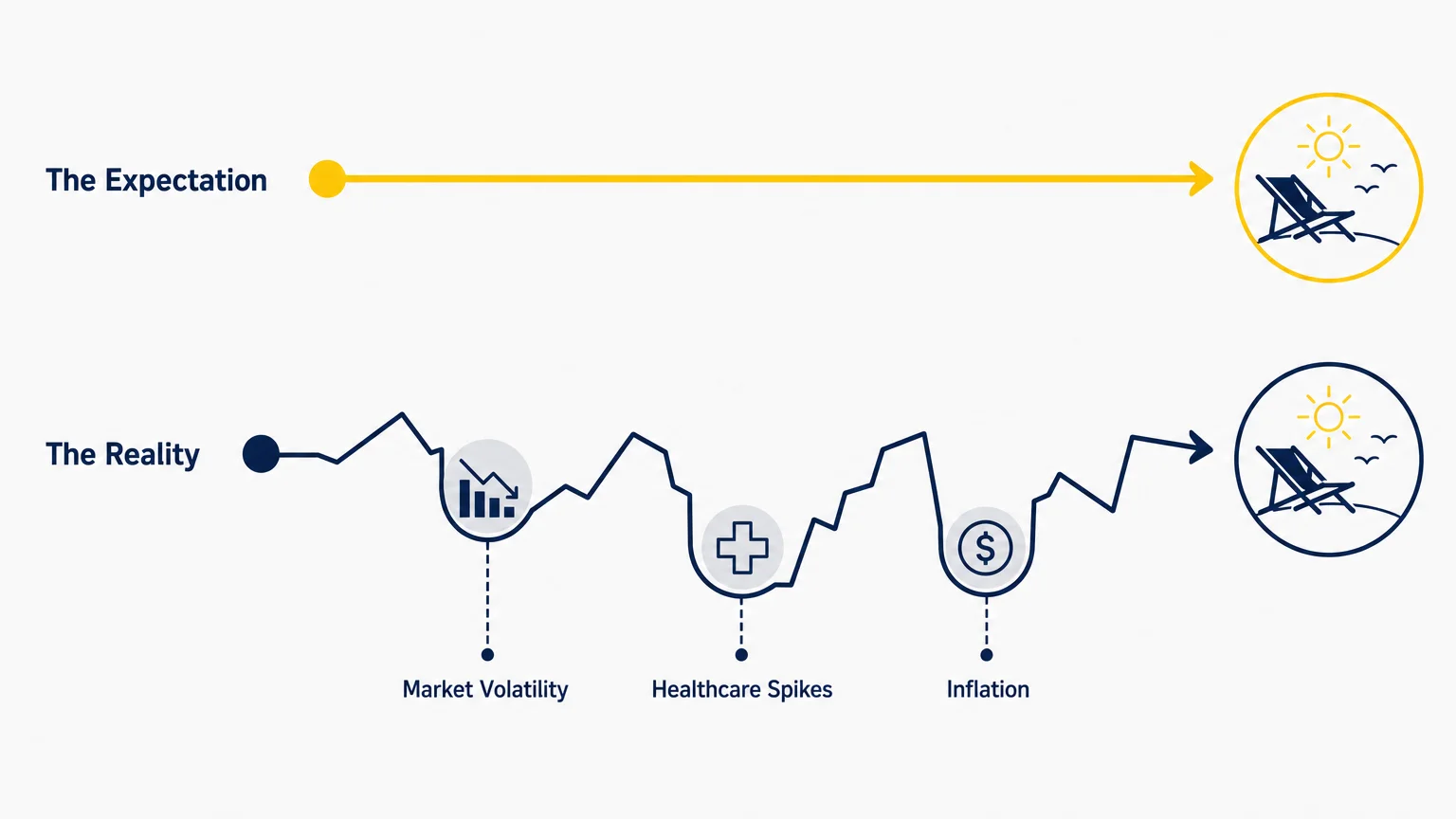

Comparing Expected Retirement Scenarios With Reality

Understanding the gap between expectation and reality helps you build contingencies into your plan. Here is a breakdown of how common strategies unfold.

| Retirement Strategy | The Expectation | The Common Reality |

|---|---|---|

| Moving to a 55+ Community | Cheaper living with resort-style amenities and endless socializing. | High HOA fees, strict community rules, and hidden assessment costs. |

| Delaying Travel Until Retirement | Spending the first ten years constantly touring the globe. | Travel burnout, sudden health limitations, and rising travel inflation. |

| Living Solely on Yield | Paying all bills using only stock dividends and bond interest. | Yields fail to keep pace with inflation, requiring principal withdrawals. |

| Aging in Place | Staying in the two-story family home forever without issues. | Mobility declines make stairs dangerous; home maintenance becomes exhausting. |

6. Scheduling Constant Travel During the “Go-Go” Years

Financial planners often divide retirement into three phases: the “Go-Go” years, the “Slow-Go” years, and the “No-Go” years. Recognizing that health and energy are finite, many new retirees pack their first five years with aggressive travel itineraries—cruises, European tours, and cross-country RV road trips.

This sprint approach frequently leads to travel burnout. Living out of suitcases, dealing with airport delays, and constantly sleeping in unfamiliar beds can exhaust even the most enthusiastic adventurer. Moreover, front-loading your retirement with luxury travel drains your portfolio during its most vulnerable phase. Withdrawing large sums during your early retirement years magnifies the damage if the stock market experiences a concurrent downturn.

The better approach: Pace your adventures. Alternate major international trips with affordable, localized travel. Establish a dedicated travel fund separate from your primary living expenses, ensuring your core financial security remains untouched regardless of your itinerary.

7. Relying Entirely on Adult Children for Care

Some seniors skip purchasing long-term care insurance or establishing a robust medical fund, assuming their adult children will simply take them in and provide care when their health declines. This expectation places a crushing emotional, physical, and financial burden on the next generation.

Your children likely have full-time careers and children of their own. Providing round-the-clock assistance for an aging parent disrupts their earning potential and creates severe family friction. Medical needs like dementia care, transferring a parent from a bed to a wheelchair, or managing complex medication schedules require specialized professional training that family members simply do not possess.

The better approach: Take control of your own aging process. Explore resources through the Eldercare Locator to understand the local support systems available in your community. Plan financially for home health aides, assisted living, or modifications to your home so you can maintain your independence without turning your children into full-time caregivers.

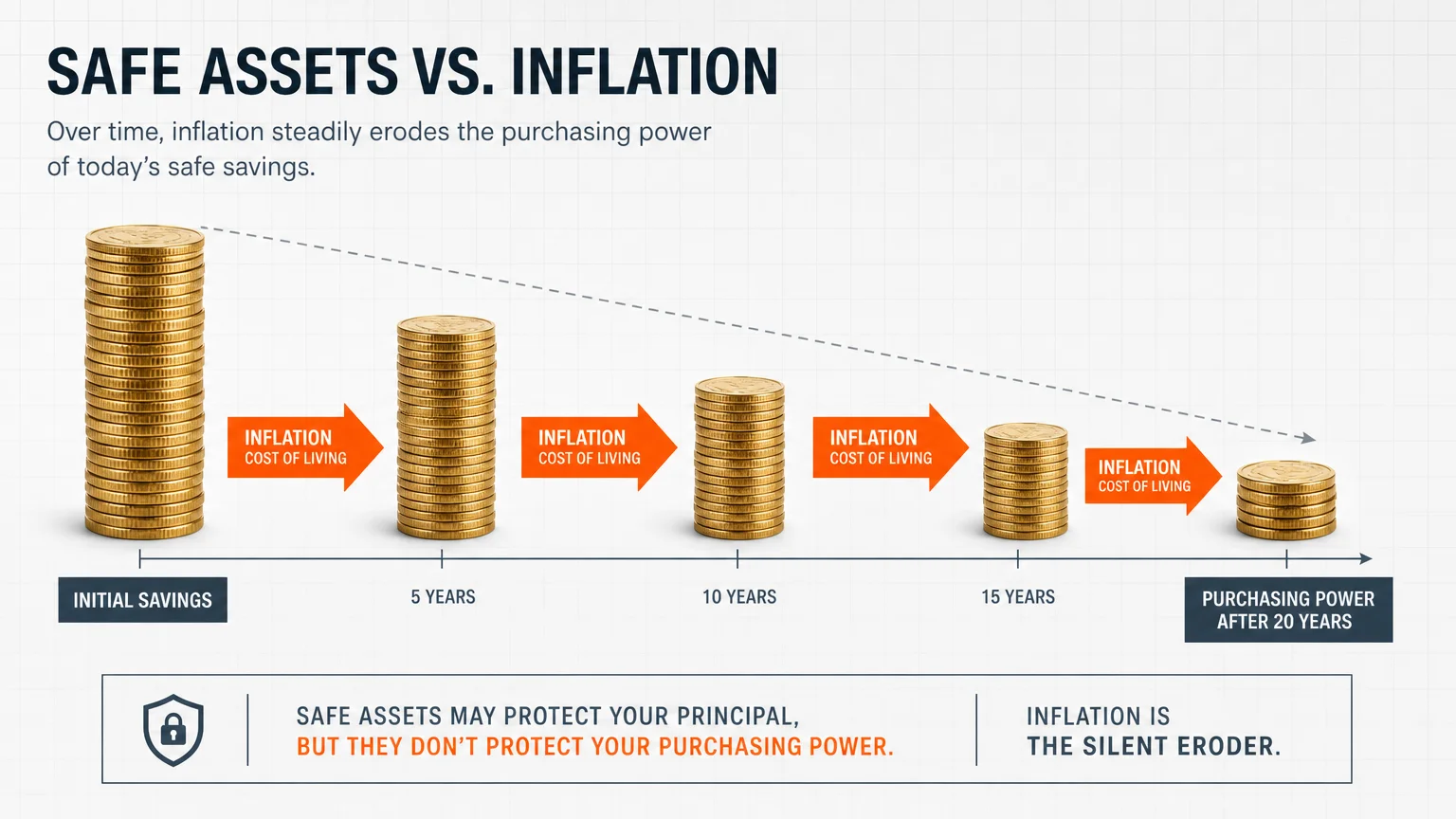

8. Moving Your Entire Portfolio into “Safe” Assets

As the final day of work approaches, the fear of a stock market crash drives many retirees to liquidate their equity positions and move everything into cash, certificates of deposit (CDs), and fixed-income bonds. Protecting your principal feels like the smart, conservative choice.

In reality, inflation is a silent portfolio killer. Over a 20-to-30-year retirement, the cost of groceries, utilities, and medical care will double or even triple. If your money sits entirely in low-yield “safe” assets, your purchasing power steadily erodes. You might not lose a dime of your principal, but you will slowly go broke because your money buys less every single year.

The better approach: Maintain a balanced portfolio that includes equities for long-term growth alongside bonds and cash for short-term stability. A common strategy involves keeping two to three years of living expenses in highly liquid, safe accounts to weather market drops, while leaving the rest invested to outpace inflation.

9. Treating Every Day Like a Weekend

When you first retire, discarding the alarm clock and sipping coffee on the porch for three hours feels glorious. Winging your daily routine works beautifully for the first few months—often referred to as the retirement honeymoon phase. Eventually, the novelty of doing nothing wears off, leaving a profound void.

A career provides more than just a paycheck; it delivers structure, social interaction, a sense of identity, and daily problem-solving challenges. Without a plan to replace those psychological benefits, retirees frequently slip into depression, experience cognitive decline, or suffer from relationship strain as they crowd their spouse’s space.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

The better approach: Draft a lifestyle business plan. Schedule regular volunteer shifts, enroll in continuing education classes, join local clubs, or establish a strict physical fitness routine. Treat your hobbies and social engagements with the same respect and punctuality you gave your career.

Don’t Make These Mistakes

To ensure your hard-earned savings translate into a fulfilling and secure future, actively avoid these widespread retirement planning errors:

- Ignoring Required Minimum Distributions (RMDs): Forgetting to withdraw funds from your traditional IRAs and 401(k)s at the required age triggers severe IRS penalties. Map out your RMD strategy early.

- Underestimating Longevity: Actuarial tables show that if a healthy couple reaches age 65, there is a high probability at least one will live into their 90s. Plan your finances for a 30-year timeframe, not just 15 years.

- Failing to Communicate With Your Spouse: If you envision a quiet life gardening and your spouse expects to travel 200 days a year, conflict is inevitable. Sync your visions before the paychecks stop.

- Supporting Adult Children Indefinitely: Co-signing loans or continually funding your adult children’s lifestyles jeopardizes your own financial survival. You can borrow for a house or education, but you cannot borrow for retirement.

When Professional Advice Is Worth It

While many Americans manage their wealth through sheer grit and self-education, navigating the transition into retirement involves irreversible decisions that benefit immensely from professional oversight.

Engage a fee-only fiduciary financial advisor to pressure-test your withdrawal strategy against historical market data and sequence of returns risk. When it comes to healthcare, do not blindly pick a Medicare plan based on a television commercial; consult a local State Health Insurance Assistance Program (SHIP) counselor who provides free, unbiased guidance tailored to your specific prescriptions and preferred doctors. Finally, working with an elder law attorney is vital for establishing durable powers of attorney, healthcare directives, and protective trusts, ensuring your wishes are honored if you lose cognitive capacity.

Frequently Asked Questions About Retirement Expectations

Why do so many retirees regret moving to a new state?

Many retirees relocate based strictly on financial metrics like property tax rates or weather, ignoring the massive emotional impact of leaving their social support network. Once the honeymoon phase of the new location wears off, the isolation and the expense of traveling back to see family often lead to buyer’s remorse.

Can I reverse my Social Security decision if I realize I claimed too early?

Yes, but only under strict conditions. You have exactly one opportunity to withdraw your Social Security application, and you must do so within 12 months of your initial claim. Furthermore, you must repay every dollar you and your family members received from the SSA. Once repaid, you can reapply later for a higher benefit amount.

Does Medicare pay for assisted living facilities?

No. This is one of the most persistent and dangerous myths in retirement planning. Medicare covers medical care, such as doctor visits, hospitalizations, and short-term rehabilitation. It does not cover the custodial care provided in assisted living facilities or memory care units. You must fund these expenses out-of-pocket, through long-term care insurance, or by qualifying for Medicaid after exhausting your assets.

How much of my portfolio is safe to withdraw each year?

The traditional benchmark has been the “4% Rule,” which suggests withdrawing 4% of your initial portfolio value and adjusting for inflation annually. However, given modern longevity and fluctuating bond yields, many experts now recommend a more dynamic withdrawal strategy, starting closer to 3.3% to 3.8% and adjusting your spending downward during bear markets to preserve capital.

Stepping into retirement is a monumental achievement, but success requires treating it as an active, evolving phase of life rather than a static finish line. Take the time today to review your housing, healthcare, and income strategies against the realities outlined above. Adjusting your expectations now prevents painful financial corrections later, allowing you to genuinely enjoy the freedom you have worked so hard to build.

Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: June 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.