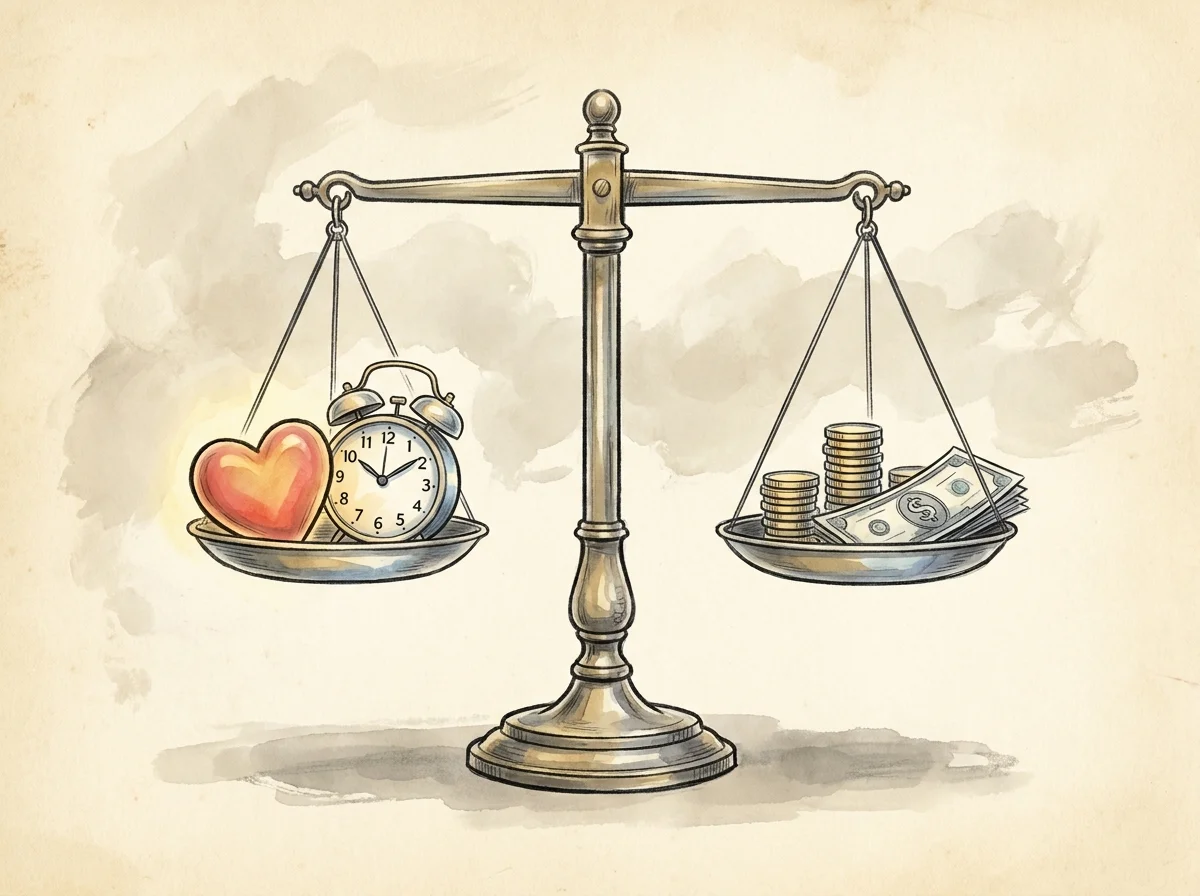

Many retirees discover their favorite pastimes organically evolve into reliable streams of extra income. Spending forty hours a week at a demanding career leaves little room for creative pursuits, but retirement finally provides the canvas to master skills you genuinely enjoy. What starts as a casual weekend woodworking project, a sprawling backyard garden, or a knack for restoring vintage furniture can quickly attract paying customers without the stress of a traditional job. Monetizing a passion project gives your days rewarding structure while providing financial padding to offset rising healthcare and daily living costs. By transforming your natural talents into a low-stress side hustle, you create an ideal balance between purposeful engagement and financial security.

The Financial Power of Purposeful Play

Finding a productive rhythm after leaving the workforce requires intention. Without the structured routine of a 9-to-5, days can easily blur together. Transforming an enjoyable activity into a small-scale business venture offers a compelling reason to get out of bed, learn new systems, and interact with your community.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

Retirement hobbies do much more than pass the time. Research consistently shows that staying mentally and socially engaged delays cognitive decline and improves overall well-being. Organizations like AARP frequently highlight how older adults who maintain active, goal-oriented routines report higher levels of life satisfaction. When you add a financial incentive to an activity you already love, you create a sustainable model for healthy aging.

9 Retirement Hobbies That Turn Into Extra Income

You do not need to invent the next big tech startup to generate a meaningful side income. The best retirement side hustles leverage existing skills and require minimal upfront investment. Here are nine popular pastimes that frequently transition into profitable ventures.

1. Woodworking and Custom Crafting

Working with your hands provides immediate, tangible satisfaction. Many retirees spend years accumulating tools and building furniture for their own homes. Once your house is full, selling your creations becomes the logical next step. Smaller items like custom end-grain cutting boards, turned wooden bowls, birdhouses, and personalized signs sell exceptionally well at local craft fairs, farmers’ markets, and online platforms. The key is focusing on high-quality, repeatable designs that do not require massive amounts of heavy lifting or expensive exotic woods.

2. Gardening and Plant Propagation

If you have a green thumb, your backyard can become a reliable source of extra cash. Specialty nurseries charge premium prices for established houseplants, yet propagating plants like Monstera, Pothos, or rare succulents costs almost nothing. Beyond houseplants, you can sell heirloom tomato seedlings in the spring, fresh cut flower arrangements in the summer, or organic vegetables to your neighbors. This hobby keeps you physically active and outside, providing essential vitamin D and moderate exercise.

3. Photography

You no longer need a darkroom to make money from photography. If you enjoy hiking with your DSLR or mirrorless camera, your nature shots can be sold on stock photography websites. Alternatively, you can offer localized services. Real estate agents constantly need reliable photographers to shoot new property listings. Families frequently look for affordable portrait photographers for holiday cards or graduation pictures. Because you control your booking schedule, you only take on the assignments that fit your desired pace.

4. Writing, Copyediting, and Proofreading

If you spent your career writing reports, drafting grants, or simply harboring a love for language, the freelance writing market offers endless opportunities. Small businesses need help writing blog posts, crafting newsletters, and updating their website copy. If writing from scratch feels too daunting, copyediting and proofreading provide a steady alternative. The major advantage of this side hustle is absolute geographical freedom; you can edit a manuscript from your living room couch or the balcony of a cruise ship.

5. Baking and Specialty Food Preparation

Nearly every state now has “cottage food laws” that allow individuals to sell baked goods prepared in their home kitchens directly to consumers. If you are famous in your family for your sourdough bread, custom decorated sugar cookies, or specialty jams, there is likely a local market eager to buy them. Retirees often partner with local independent coffee shops to supply daily pastries, or they set up dedicated stalls at weekend community markets.

6. Pet Care and Dog Walking

Animal lovers find immense joy in pet sitting, and it happens to be a highly lucrative service. Young professionals and busy families constantly need reliable people to walk their dogs during the workday or watch their pets while they travel. As a retiree, your flexible schedule makes you the perfect candidate. Signing up on established apps connects you with local clients instantly. Beyond the extra income, daily dog walking guarantees you hit your daily step count, directly benefiting your cardiovascular health.

7. Restoring Antiques and Flipping Furniture

The thrill of the hunt drives this popular hobby. Scouring estate sales, thrift stores, and garage sales for undervalued furniture allows you to flex your creative muscles. A solid wood dresser with peeling veneer might cost twenty dollars; with a few hours of sanding, some fresh paint, and modern hardware, it can easily sell for hundreds on local community boards. Upcycling keeps quality furniture out of landfills while putting profit directly into your pocket.

8. Tutoring and Music Instruction

Patience and lifetime experience make retirees excellent teachers. If you play the piano, guitar, or violin, offering weekly lessons to neighborhood children provides a steady, predictable income stream. If academics are more your speed, tutoring students in math, history, or reading—either in-person or via video call—allows you to shape the next generation. Passing down your knowledge brings a profound sense of legacy and purpose to your weekly routine.

9. Consulting and Mentoring

Sometimes the most lucrative hobby is simply offering your career expertise on your own terms. Former executives, accountants, HR professionals, and engineers often transition into freelance consulting. Instead of managing a massive team and attending pointless corporate meetings, you get to parachute into companies, solve specific problems, and leave. You dictate your hourly rate and choose exactly how many hours a week you want to engage.

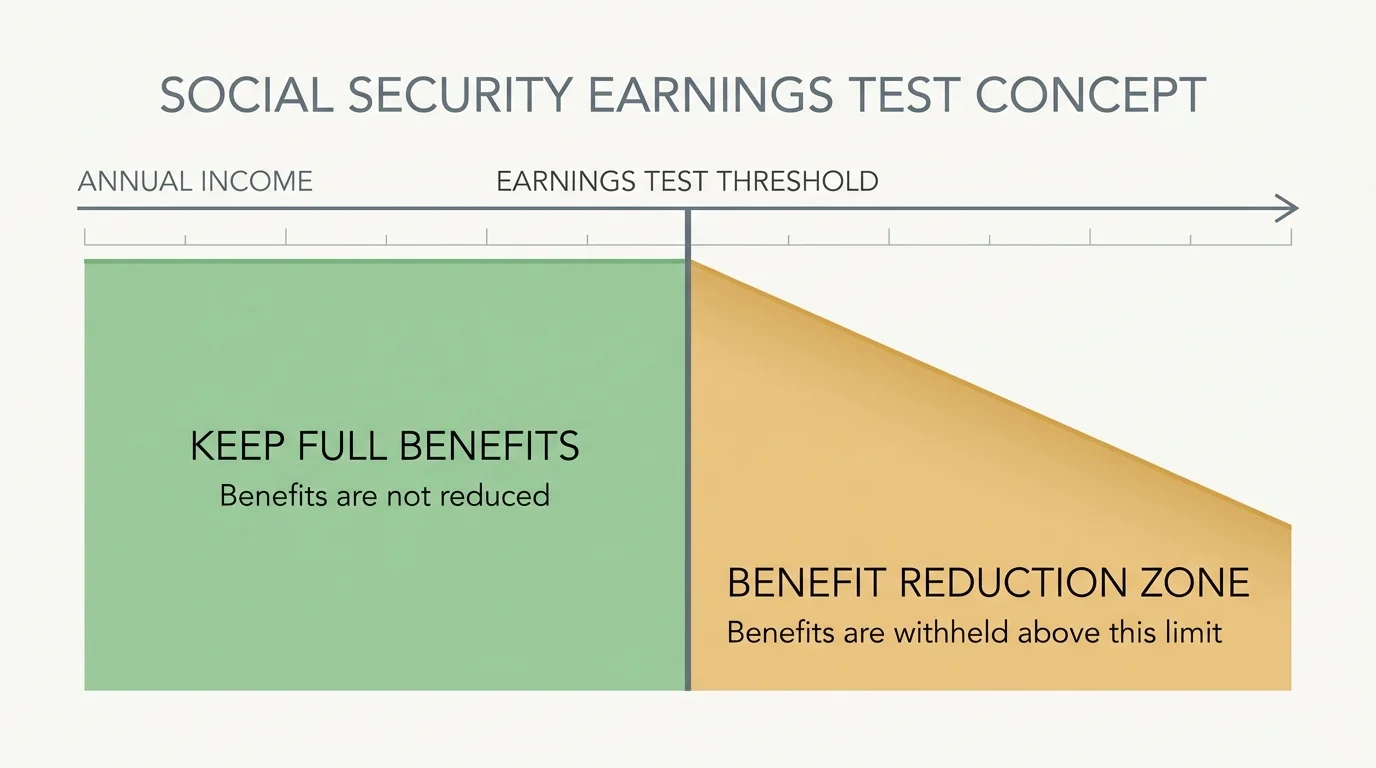

How Extra Income Affects Your Social Security Benefits

Before launching your new venture, you must understand how earning money impacts your retirement benefits. If you have already claimed Social Security but have not yet reached your Full Retirement Age (FRA), the Social Security Administration (SSA) enforces an earnings limit. Earning too much from your side hustle can temporarily reduce your monthly benefit check.

The rules depend entirely on your age relative to your FRA. Here is how the earnings test generally applies:

| Your Age Status | How the Earnings Test Works | Impact on Benefits |

|---|---|---|

| Under Full Retirement Age (Entire Year) | Subject to the standard annual earnings limit. | $1 in benefits is withheld for every $2 you earn above the annual limit. |

| The Year You Reach Full Retirement Age | Subject to a higher limit, counting only earnings before your birthday month. | $1 in benefits is withheld for every $3 you earn above the limit. |

| Month of Full Retirement Age and Beyond | No earnings limit applies. | You can earn unlimited income with zero reduction to your Social Security benefits. |

It is important to note that withheld benefits are not lost forever. Once you reach Full Retirement Age, the SSA recalculates your benefit amount upward to account for the months they withheld payments. However, managing cash flow during those early retirement years requires careful planning if your side hustle takes off faster than expected.

Costly Mistakes to Avoid

Turning a hobby into a business introduces new logistical hurdles. Avoid these common pitfalls to ensure your extra income remains a blessing rather than a burden:

- Blurring personal and business finances: The moment you start accepting money for your hobby, open a separate, free checking account. Commingling funds makes tax season a nightmare and makes it impossible to know if you are actually turning a profit.

- Ignoring self-employment taxes: When you work a traditional job, your employer pays half of your Medicare and Social Security taxes. As a self-employed hobbyist, you are responsible for the full amount (often called the self-employment tax). Set aside roughly 25 to 30 percent of your profits to cover federal, state, and self-employment tax liabilities.

- Overinvesting in equipment early on: Prove your concept before emptying your savings. Do not buy a commercial-grade baking oven until you have consistently sold out of goods made in your standard kitchen. Let your business profits fund your equipment upgrades.

- Failing to check local zoning and licensing: Operating a small business out of your home may require a basic municipal license or adherence to HOA guidelines. A quick call to your local county clerk can save you from unexpected fines.

Don’t DIY These Decisions

While you can absolutely manage the day-to-day operations of your hobby independently, the financial architecture behind it requires professional oversight. The line between a “hobby” and a “business” is strictly defined by the Internal Revenue Service. If the IRS classifies your activity as a hobby, you generally must report the income, but you cannot deduct the expenses used to generate that income. If it is classified as a business, you can deduct legitimate expenses (like supplies, specialized tools, or a portion of your home internet) to lower your tax burden.

Consult a Certified Public Accountant (CPA) or a qualified tax professional during your first year of generating income. They will help you establish proper bookkeeping habits and determine if you qualify to open a solo 401(k) or SEP IRA. Reviewing the IRS Retirement Plans guidelines with a professional ensures you maximize your legal tax advantages while staying fully compliant.

Frequently Asked Questions

Do I have to pay taxes on money I make from my retirement hobby?

Yes. Any net earnings generated from a hobby or side business are considered taxable income by the IRS. You must report this income on your annual tax return. If your net earnings exceed a certain low threshold (typically $400 for self-employment), you will also owe self-employment tax, which covers your Medicare and Social Security contributions.

Can I contribute to an IRA using the money I make from my side hustle?

Yes, and this is one of the biggest hidden benefits of working in retirement. To contribute to a Traditional or Roth IRA, you must have “earned income.” Pension payouts, Social Security checks, and investment dividends do not count as earned income. However, the profit from your side hustle does count, allowing you to continue growing your tax-advantaged retirement accounts.

Will my side hustle income increase my Medicare premiums?

It is possible. Medicare Part B and Part D premiums are tied to your Modified Adjusted Gross Income (MAGI) from two years prior. This is known as the Income-Related Monthly Adjustment Amount (IRMAA). If your new business is highly profitable and pushes your income over the specific IRMAA thresholds, you may face higher Medicare premiums down the road. A tax professional can help you manage your deductions to mitigate this risk.

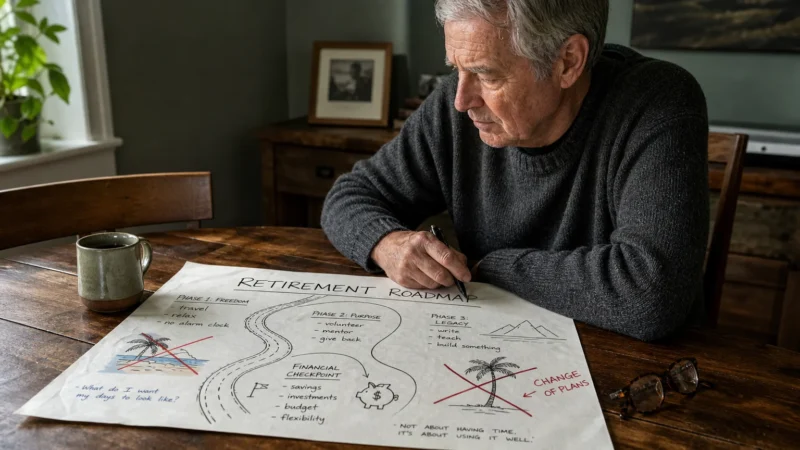

Taking the leap from amateur enthusiast to paid professional injects fresh energy into your retirement years. Start small, focus on the joy of the craft, and let the income grow organically. Whether you use the extra cash to fund a dream vacation, spoil your grandchildren, or simply create a wider buffer against inflation, monetizing your passions proves that your most productive and fulfilling years may still be ahead of you. Track your earnings carefully, consult a tax professional to optimize your setup, and enjoy the rewards of working entirely on your own terms.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.