Selling the family home to retire on the beach sounds like the ultimate American dream, but trading snow shovels for seashells often comes with devastating financial surprises. Many retirees flock to idyllic shorelines without realizing that soaring insurance premiums, hidden property taxes, and overtaxed healthcare infrastructure can drain a nest egg in record time. Before you pack up and head for the coast, you need to understand the true cost of paradise. Uncovering the hidden pitfalls of the nation’s most popular coastal retirement towns can save you from making a relocation mistake that jeopardizes your financial security and peace of mind during your golden years.

Myrtle Beach, South Carolina: The Healthcare Infrastructure Squeeze

Myrtle Beach consistently ranks among the top coastal retirement towns due to its affordable housing, world-class golf courses, and favorable tax climate for seniors. However, this massive influx of retirees has created a severe strain on local infrastructure—specifically specialized healthcare.

While the area offers plenty of primary care clinics and urgent care centers, securing an appointment with an in-network geriatric specialist, neurologist, or cardiologist often requires months of waiting. When dealing with complex age-related health conditions, many retirees find themselves driving two hours to Charleston or crossing state lines to receive prompt, high-level care. This distance becomes a significant burden if you lose your ability to drive or require frequent treatments. Furthermore, the summer tourist season gridlocks the local roads, turning a standard pharmacy run or doctor visit into an exhausting, hours-long ordeal.

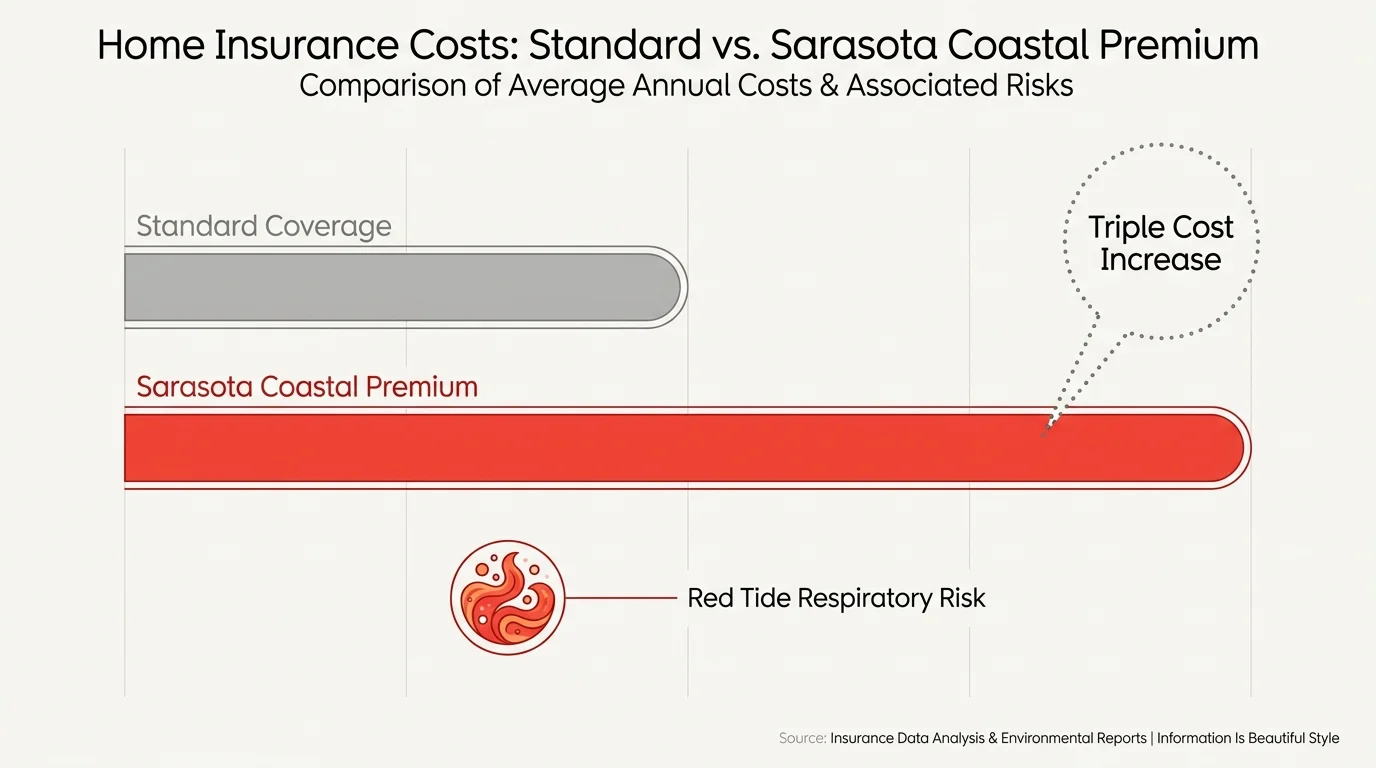

Sarasota, Florida: The Insurance Premium Shock

Known for its vibrant arts scene and pristine white-sand beaches, Sarasota attracts retirees looking for a sophisticated coastal lifestyle. Unfortunately, living on the Gulf Coast exposes you to some of the most volatile homeownership costs in the country. The frequency and severity of recent storms have sent Florida’s property insurance market into a tailspin.

Retirees who budgeted carefully for fixed housing costs find their plans shattered by homeowners and flood insurance premiums that can double or triple over a single year. In many coastal neighborhoods, insurers are simply pulling out of the market altogether, forcing residents onto state-backed plans that offer less coverage for more money. Beyond the financial beach retirement risks, Sarasota frequently battles severe red tide blooms. These toxic algae blooms release airborne toxins that cause severe respiratory irritation, trapping seniors indoors for weeks at a time and completely negating the benefits of oceanfront living.

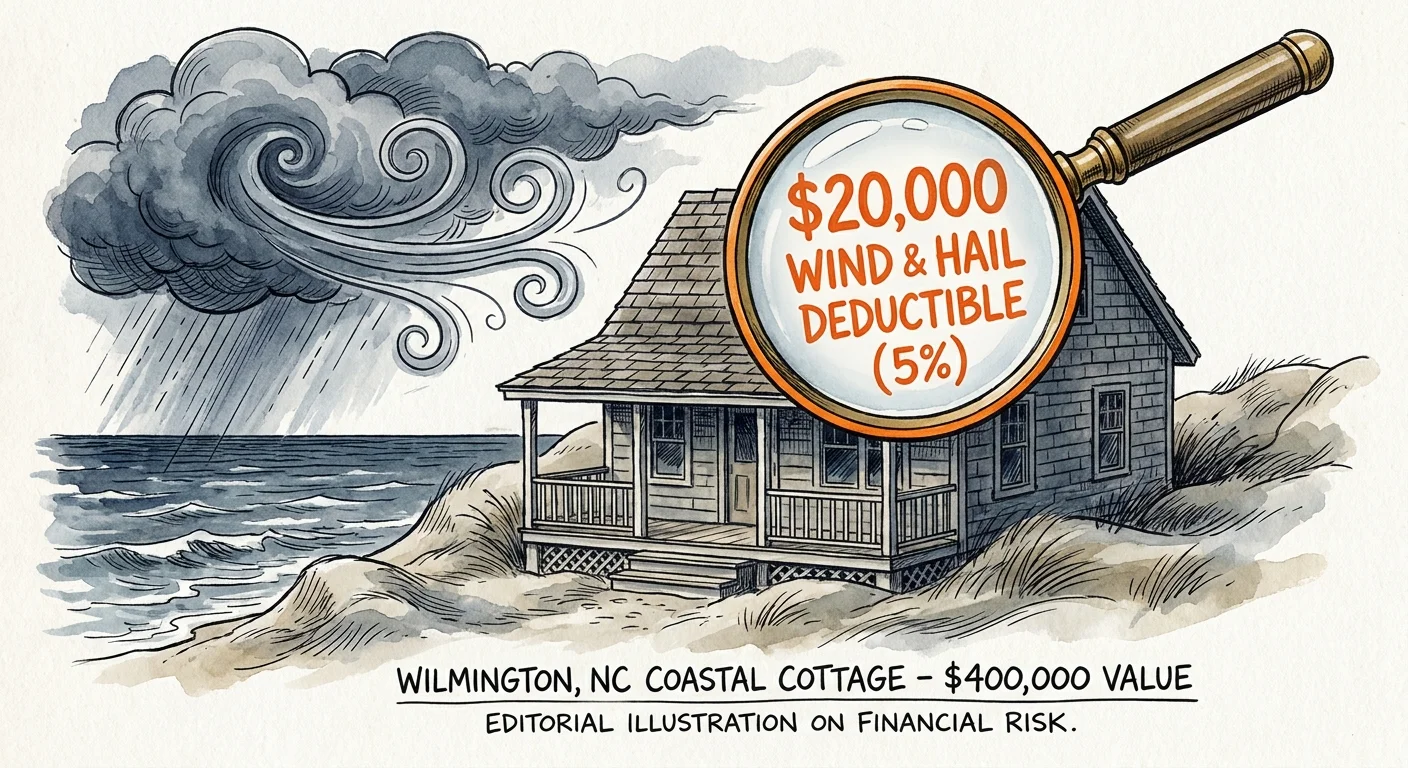

Wilmington, North Carolina: The Hurricane Corridor Tax

Wilmington offers a charming historic downtown, a moderate climate, and a lower cost of living compared to traditional Florida destinations. Yet, this historic port city sits directly in the path of the Atlantic hurricane corridor.

The hidden pitfall here lies in the specialized insurance deductibles. Most homeowners insurance policies in hurricane-prone areas include a separate wind and hail deductible, typically calculated as a percentage of your home’s total insured value rather than a flat dollar amount. If your home is insured for $400,000 and you have a 5% windstorm deductible, you must pay $20,000 out of pocket before your insurance covers a dime of hurricane damage. For retirees living on a fixed income, a single severe storm can wipe out an entire emergency fund. When considering a retirement relocation coast destination like Wilmington, you must factor large, unpredictable cash reserves into your financial plan.

Galveston, Texas: The Erosion and Evacuation Toll

Galveston Island boasts rich history, a laid-back atmosphere, and proximity to Houston’s world-class medical facilities. It appears perfect for seniors who want beach living without sacrificing big-city amenities. However, Galveston is a barrier island actively battling severe coastal erosion and extreme weather vulnerability.

Living on a barrier island means living with the constant threat of mandatory evacuations. As you age, evacuating becomes significantly more physically taxing and mentally stressful. Securing your home, sitting in hours of gridlocked traffic on the single interstate bridge connecting the island to the mainland, and securing pet-friendly hotel accommodations out of state drains both your energy and your wallet. Additionally, the oppressive summer humidity exacerbates joint pain and heart conditions, making outdoor activities nearly impossible from June through September.

Rehoboth Beach, Delaware: The Off-Season Ghost Town

Delaware is a well-known tax haven for retirees. The state boasts no sales tax, low property taxes, and no tax on Social Security benefits. Rehoboth Beach, the jewel of the Delaware coast, draws thousands of retirees eager to maximize their income.

The coastal living downsides here are twofold: exorbitant real estate entry prices and severe seasonal isolation. To enjoy Delaware’s low taxes in Rehoboth Beach, you must first navigate a housing market driven sky-high by wealthy vacation-home buyers from Washington D.C. and Philadelphia. Once you purchase a home, you must prepare for the dramatic off-season shift. From November to April, many local restaurants, pharmacies, and specialty shops close their doors completely. The bustling summer community transforms into a quiet, cold, and often isolating winter landscape, which can rapidly accelerate feelings of loneliness and depression among aging adults.

Gulf Shores, Alabama: The Tourism Overload

Gulf Shores provides beautiful emerald waters and a relatively low cost of living, making it an attractive alternative to pricier Florida towns. But Gulf Shores was built for tourists, not for residents aging in place.

The town’s infrastructure prioritizes short-term rentals and vacation entertainment over senior community services. Navigating a town with limited public transportation, few comprehensive senior centers, and an infrastructure heavily skewed toward the hospitality industry makes aging in place incredibly difficult. During peak season, the population swells exponentially, straining local resources. If you eventually require in-home caregiving or assisted living support, you will find a severe shortage of qualified healthcare workers, as the local labor market is heavily concentrated in tourism and hospitality. Before choosing a heavily touristed area, check local resources using the Eldercare Locator to ensure long-term support exists.

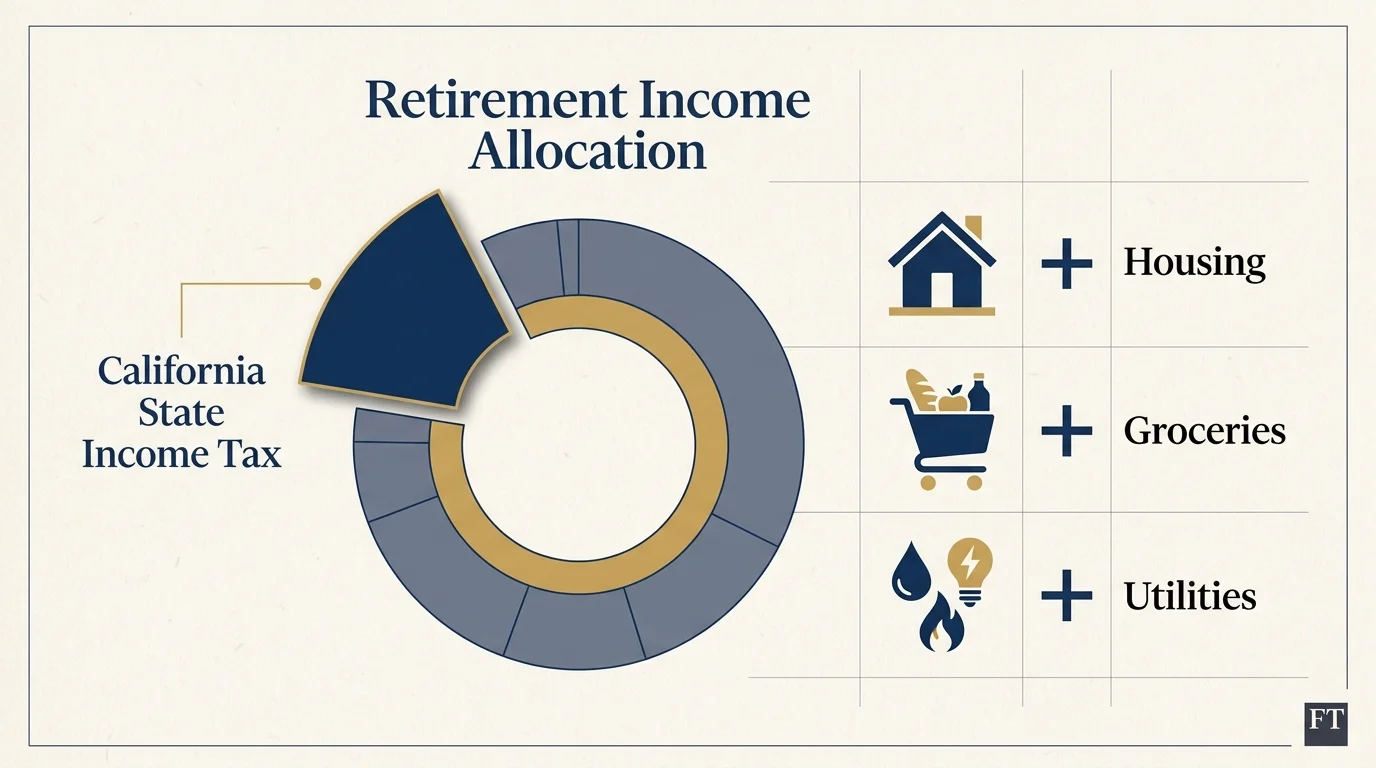

Santa Barbara, California: The Taxation and Cost of Living Trap

With its Mediterranean climate, stunning mountains, and beautiful coastline, Santa Barbara is often viewed as the ultimate luxury retirement destination. The pitfalls here are strictly financial, yet they ruin more retirement plans than any storm.

California’s high state income tax, massive gasoline taxes, and exorbitant base cost of living create a relentless drain on fixed incomes. Even if you hold substantial retirement assets, the day-to-day cost of goods in Santa Barbara will erode your purchasing power faster than almost anywhere else in the country. Furthermore, the secondary risks of coastal living in Southern California—specifically wildfires and mudslides in the coastal hills—result in astronomical insurance premiums or outright policy cancellations. Relocating here without a massive, heavily padded financial buffer is a surefire path to outliving your savings.

Costly Mistakes to Avoid

Relocating for retirement requires more than just hiring a moving truck; it requires strategic foresight. Falling in love with a vacation destination and buying a home there without running a harsh financial stress test is one of the most common coastal retirement mistakes.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

To protect your nest egg and your well-being, actively avoid these major missteps:

- Buying Without Renting First: Never buy a retirement home in a coastal town without spending at least four consecutive weeks there during the worst part of the year. Renting during a humid, crowded August or a desolate, freezing February reveals the town’s true livability.

- Ignoring Aging-in-Place Architecture: Coastal building codes often require homes to be elevated on pilings to mitigate flood risks. While a two-story raised beach house offers great views today, navigating 20 outdoor wooden stairs will become a nightmare if you eventually face mobility issues or require a wheelchair.

- Miscalculating Medicare Advantage Networks: If you use a Medicare Advantage (Part C) HMO plan, your network is localized. Moving to a new state or a rural coastal town often means your current plan will not travel with you. You must verify that your new zip code offers robust, affordable plan options with in-network specialists.

- Failing to Stress-Test the Budget: Calculate your budget assuming property taxes will rise by 5% annually and homeowners insurance will rise by 15% annually. If your fixed income cannot absorb those projected increases, the location is too risky.

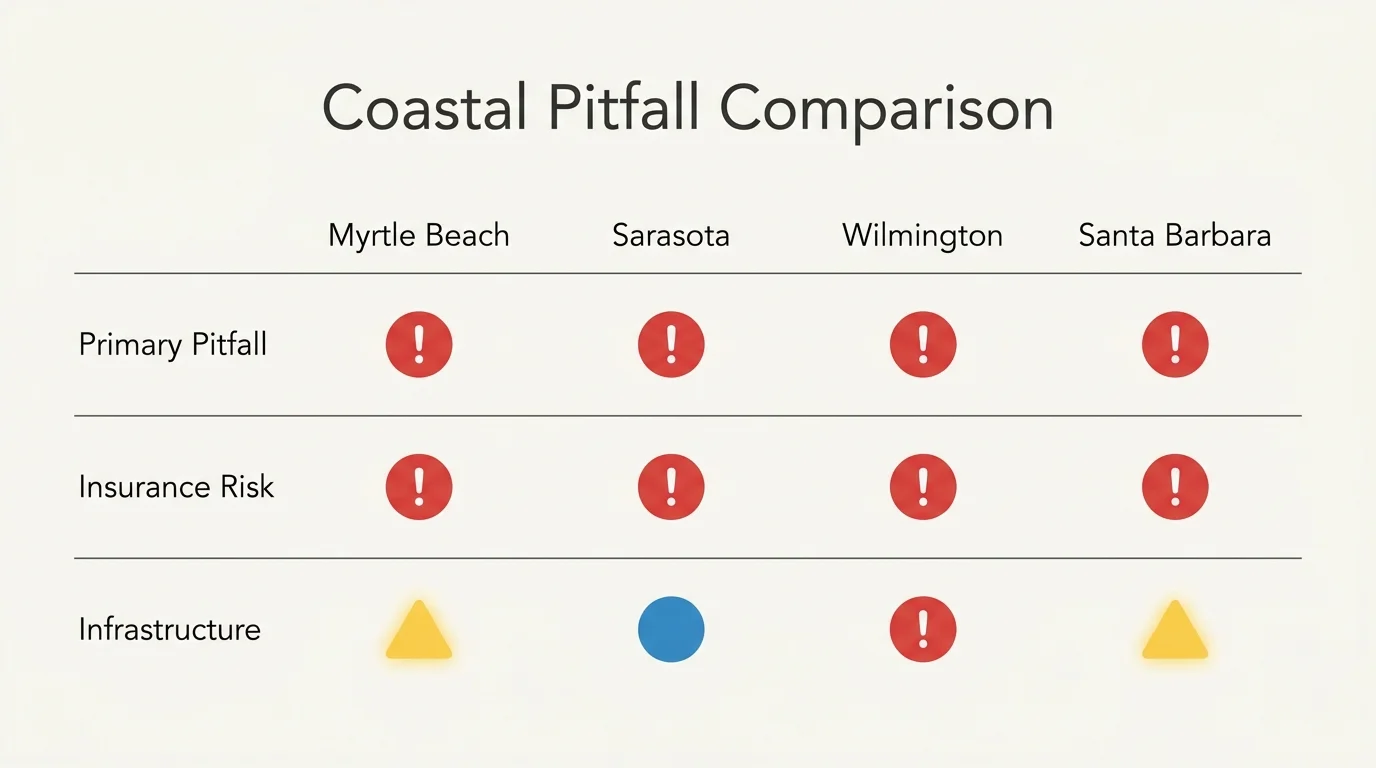

Comparing the Hidden Costs of Coastal Living

When evaluating these destinations, you must weigh the primary draw against the long-term risk. Use this breakdown to align your relocation choices with your physical and financial needs.

| Coastal Town | Primary Draw | Biggest Hidden Pitfall | Risk Level for Fixed Incomes |

|---|---|---|---|

| Myrtle Beach, SC | Low taxes, affordable housing | Overburdened healthcare system | Moderate |

| Sarasota, FL | Arts, culture, pristine beaches | Exploding insurance costs & red tide | High |

| Wilmington, NC | Historic charm, moderate climate | Massive wind/hail insurance deductibles | Moderate |

| Galveston, TX | Proximity to Houston, relaxed vibe | Erosion and stressful evacuations | High |

| Rehoboth Beach, DE | Zero sales tax, low property tax | High entry prices & winter isolation | Low to Moderate |

| Gulf Shores, AL | Low cost of living, emerald waters | Lack of aging-in-place infrastructure | Moderate |

| Santa Barbara, CA | Perfect climate, luxury lifestyle | Extreme taxation and cost of living | Very High |

Don’t DIY These Decisions

Moving across state lines in retirement triggers a cascade of legal, tax, and healthcare changes. Attempting to navigate these complexities alone often results in missed deadlines and harsh financial penalties.

Before you commit to a coastal move, consult an elder law attorney to update your estate planning documents. Advance directives, power of attorney forms, and living wills are governed by state law; the documents you drafted in Ohio may not be fully recognized or easily executed in Florida or South Carolina.

Additionally, speak with a fee-only fiduciary financial advisor to optimize your withdrawal strategy around your new state’s tax laws. A qualified advisor helps you model out worst-case scenarios regarding out-of-pocket healthcare costs and property insurance spikes. For comprehensive, unbiased guidance on managing your money as you transition into retirement, utilize free educational resources from the Consumer Financial Protection Bureau (CFPB).

Frequently Asked Questions

Does Medicare cover out-of-state care if I split my time between a coastal home and my primary residence?

Original Medicare (Part A and Part B) covers you anywhere in the United States at any doctor or hospital that accepts Medicare. However, if you have a Medicare Advantage plan (Part C), you are generally restricted to a local network of providers. If you become a “snowbird,” you must look for a Medicare Advantage plan with a visitor/travel benefit or consider switching to Original Medicare with a Medigap policy for nationwide flexibility. Always review your options thoroughly via AARP or the official Medicare website.

How much should I budget for coastal property insurance in retirement?

Budgeting for coastal property insurance requires extreme caution. In high-risk states like Florida, Texas, and coastal Carolinas, seniors should budget at least double the national average for homeowners insurance, plus an additional $1,000 to $3,000 annually for a separate flood insurance policy. Most importantly, you must maintain a liquid emergency fund capable of covering a 2% to 5% hurricane deductible on your home’s total insured value.

What happens to my Social Security benefits if I move to a different state?

Your federal Social Security base benefit amount does not change when you move to a new state. However, your net income might change based on state taxes. While the federal government taxes Social Security benefits above certain income thresholds, state laws vary wildly. Some states fully exempt Social Security from state income tax, while others tax a portion of it. Use the resources provided by the Social Security Administration (SSA) to manage your address updates and direct deposits.

Are there coastal retirement towns with low hurricane risks?

If you want ocean proximity with minimal hurricane risk, you have to look outside the Atlantic and Gulf coasts. The Pacific Northwest—such as coastal towns in Oregon or Washington—offers beautiful shorelines with virtually zero hurricane risk, though you trade warm waters for a cooler, wetter climate. Alternatively, retiring near the Great Lakes provides a “coastal” lifestyle (boating, beaches, water views) without the extreme tropical storm threats.

Choosing a coastal retirement town requires you to look past the beautiful sunsets and evaluate the unglamorous realities of aging. A successful relocation hinges on your willingness to research local healthcare availability, realistically model extreme weather costs, and plan for your future mobility needs.

Take the time to rent a property in your desired town during its most difficult season. Test the infrastructure, verify your insurance estimates, and talk to locals who have lived there year-round. Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.