Retiring to endless leisure sounds brilliant until you realize a permanent vacation quickly loses its shine. A retirement career pivot transforms restless hours into a source of income, social connection, and renewed purpose. Instead of merely filling time, stepping back into the workforce on your own terms lets you leverage decades of expertise without the grinding stress of climbing a corporate ladder. Whether you want to fund extra travel, delay tapping your investment portfolio, or simply engage your mind with fresh challenges, taking on a new role offers tremendous benefits. If your days feel too quiet and your energy demands an outlet, you are likely ready to redefine your next chapter through meaningful work.

1. Your Hobbies No Longer Provide Enough Stimulation

Many Americans cross the finish line of their primary careers with visions of playing golf four days a week, tending to an immaculate garden, or finally finishing that stack of novels on the nightstand. The first few months—often called the honeymoon phase of retirement—deliver exactly what you expect. You decompress, sleep in, and tackle your leisure activities with genuine enthusiasm.

Eventually, a subtle shift occurs. Activities that once felt like a well-earned escape begin to feel like obligatory ways to pass the time. Hobbies are inherently consumptive; they absorb your time and money, which is perfectly fine in moderation. However, human beings are wired for productivity. When you spend forty years solving complex problems, managing teams, or building projects, transitioning to a life entirely devoid of output can leave you feeling intellectually restless. If you find yourself staring at your fishing gear or knitting needles with a sense of apathy, your brain is actively signaling that it requires a more demanding challenge.

2. You Miss the Daily Camaraderie of the Workplace

Work provides a built-in social ecosystem. For decades, your professional life supplied a steady stream of casual interactions, collaborative problem-solving, and shared goals. You likely did not realize how much you relied on breakroom banter, quick check-ins with colleagues, or client conversations to fulfill your daily quota for human connection.

Once you exit the workforce, that vibrant social network shrinks dramatically. You must suddenly manufacture every social interaction, coordinating lunches and scheduling phone calls just to hear another voice. Social isolation poses a severe risk for seniors, accelerating both physical and mental decline. The National Institute on Aging consistently highlights the health benefits of maintaining strong social ties as we age. Returning to work—even for just ten to fifteen hours a week—instantly reinstates a network of peers, clients, and colleagues. You regain the energy that comes from being part of a team pushing toward a shared objective.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

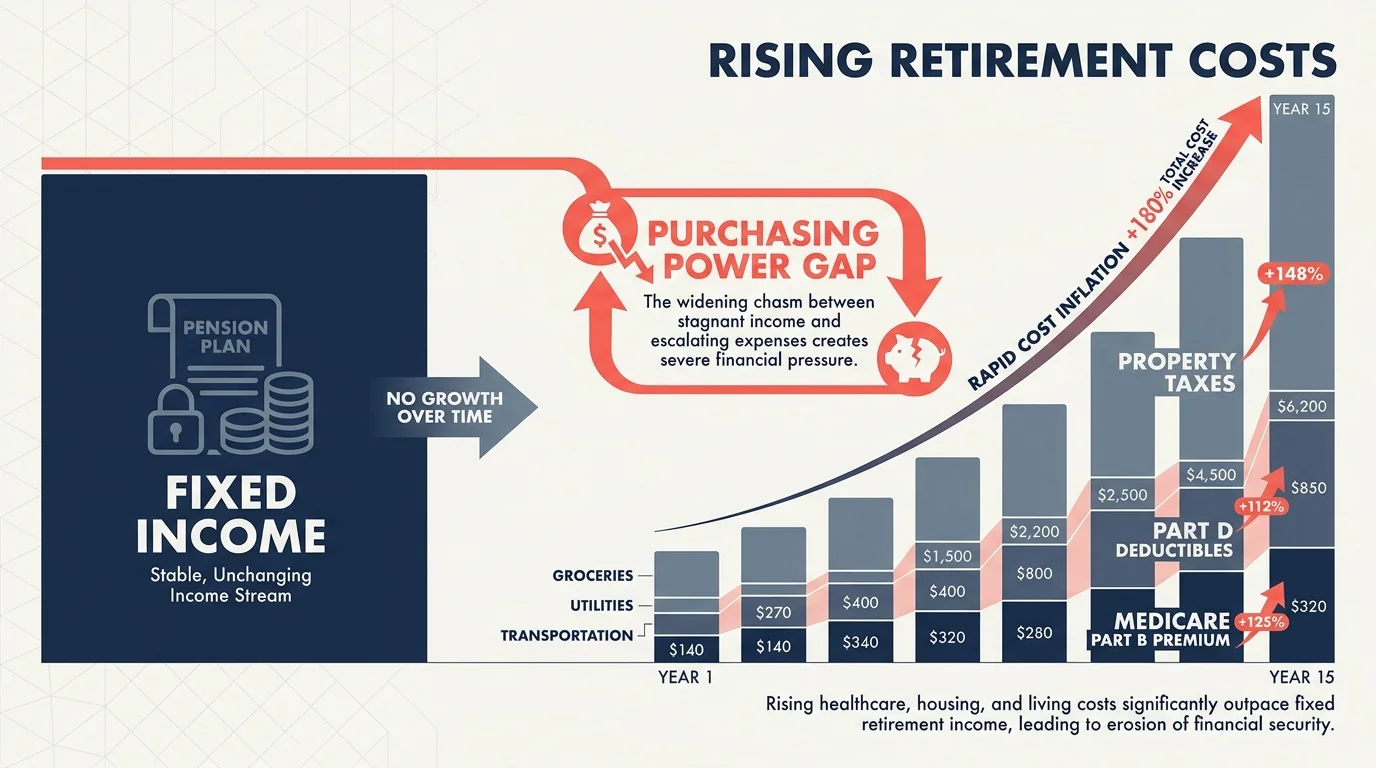

3. Inflation and Healthcare Costs Demand More Financial Cushion

Living on a fixed income forces you to pay strict attention to economic shifts. When grocery bills creep upward, property taxes jump, and utility costs surge, the purchasing power of your retirement portfolio quietly erodes. Even a carefully constructed financial plan can feel the pressure of an inflationary environment.

Healthcare expenses represent an entirely separate hurdle. Medicare covers a substantial portion of your medical needs, but out-of-pocket costs—including Part B premiums, Part D prescription deductibles, and supplemental insurance payments—add up quickly. Earning a steady paycheck from a retirement job changes the financial math entirely. A part-time income covers your essential daily expenses, allowing your investment portfolio more time to grow untouched. You gain the financial breathing room to afford premium healthcare coverage without anxiety, ensuring you can navigate rising costs confidently. If you want to optimize your coverage, utilizing tools like the Medicare Plan Finder alongside your new income stream ensures your health needs remain fully funded.

4. A Lifelong Passion Keeps Calling Your Name

Throughout your primary career, pragmatism likely dictated your choices. You took the promotion because it paid for your children’s college tuition; you stayed at a stressful company because the healthcare benefits were unbeatable. Now that your mortgage is paid down and your essential needs are covered by Social Security and savings, the rules of the game have fundamentally changed.

You finally possess the freedom to work for passion rather than a paycheck. Perhaps you spent thirty years as an accountant but always harbored a desire to work in landscape design. Maybe you retired from corporate sales but feel a strong pull to teach or work for a non-profit organization. A retirement career pivot allows you to monetize a lifelong passion without the pressure of needing it to support a family of four. If you find yourself constantly researching a specific industry or volunteering heavily in a particular field, you are already laying the groundwork for a deeply fulfilling second career.

5. You Give Professional Advice for Free

Expertise does not evaporate the moment you sign your retirement paperwork. Decades of industry knowledge, strategic thinking, and crisis management skills remain firmly intact in your mind. Because of this, younger professionals, former colleagues, and business owners in your network frequently reach out to pick your brain.

You happily meet them for coffee, review their business plans, or troubleshoot their operational bottlenecks. While offering guidance feels rewarding, consistently providing high-level consulting for the price of a latte indicates a clear opportunity. Your knowledge holds tangible market value. Transitioning these casual advisory sessions into a formal consulting business lets you dictate your hours, choose your clients, and receive appropriate compensation for the wisdom you spent a lifetime accumulating. You are already doing the work; a career pivot simply makes it official.

6. You Crave Structure and a Reason to Set an Alarm

The total absence of structure sounds liberating in theory. In practice, a calendar completely devoid of obligations often causes days to blur together indistinguishably. Without a designated reason to wake up, get dressed, and leave the house, lethargy easily sets in.

Humans thrive on a baseline level of routine. A commitment to an employer, a client, or your own small business anchors your week. It forces you to manage your time efficiently, making your leisure hours feel earned and deeply satisfying rather than merely endless. If you find yourself sleeping later than you want to or feeling unmoored without a set schedule, a part-time job provides the exact psychological grounding you require. You dictate the terms—perhaps you only commit to Tuesday and Thursday mornings—but that modest schedule creates a sturdy framework for your entire week.

7. Full-Time Leisure Feels Like a Fast Track to Mental Decline

Your brain operates much like a muscle; it requires consistent resistance training to maintain its strength. Your primary career forced you to learn new software platforms, navigate complex interpersonal dynamics, and adapt to shifting industry trends. That constant friction fostered neuroplasticity, keeping your cognitive faculties sharp and responsive.

Removing all complex problem-solving from your daily life can lead to cognitive stagnation. Crossword puzzles and reading are excellent habits, but they rarely match the multifaceted mental workout of navigating a workplace. A second career demands focus, memory retention, and adaptability. Whether you are learning a modern point-of-sale system at a local boutique or mastering new digital marketing tools for your consulting business, the active learning process acts as a powerful neuroprotective shield. If you feel your mental edge softening in retirement, re-entering the workforce delivers an immediate intellectual upgrade.

8. The Low-Stakes Entrepreneurship Bug Bites You

Starting a business in your thirties carries immense pressure. You face the terrifying reality that a failed venture could cost you your home or drain your children’s education fund. Starting a business in retirement completely neutralizes that existential dread.

With your baseline living expenses covered by guaranteed income streams, entrepreneurship transforms into an exhilarating sandbox. You can launch an Etsy shop, start a niche dog-walking service, or build a local home-repair business entirely on your own terms. If the business scales rapidly, you reap the financial rewards. If it grows slowly, you suffer no catastrophic consequences. The desire to build something from scratch—coupled with the realization that failure will not ruin you financially—is a massive indicator that you are ready to embrace the role of a senior entrepreneur.

9. You Want to Delay Claiming Social Security

The mathematics of Social Security heavily reward patience. You can claim benefits as early as age 62, but doing so results in a permanent reduction of your monthly check. Conversely, for every year you delay claiming past your Full Retirement Age (FRA) up to age 70, your benefit increases by a guaranteed 8% annually.

Many retirees file for Social Security early simply because they need the cash flow to survive. Launching a second career provides an alternative strategy. Earning enough part-time income to cover your living expenses allows you to leave your Social Security benefits untouched. This strategy practically guarantees a significantly larger monthly check later in life, providing robust protection against longevity risk. If you are determined to maximize your lifetime benefits and need a bridge strategy to get you to age 70, the Social Security Administration framework makes a part-time career pivot one of the smartest financial moves you can make.

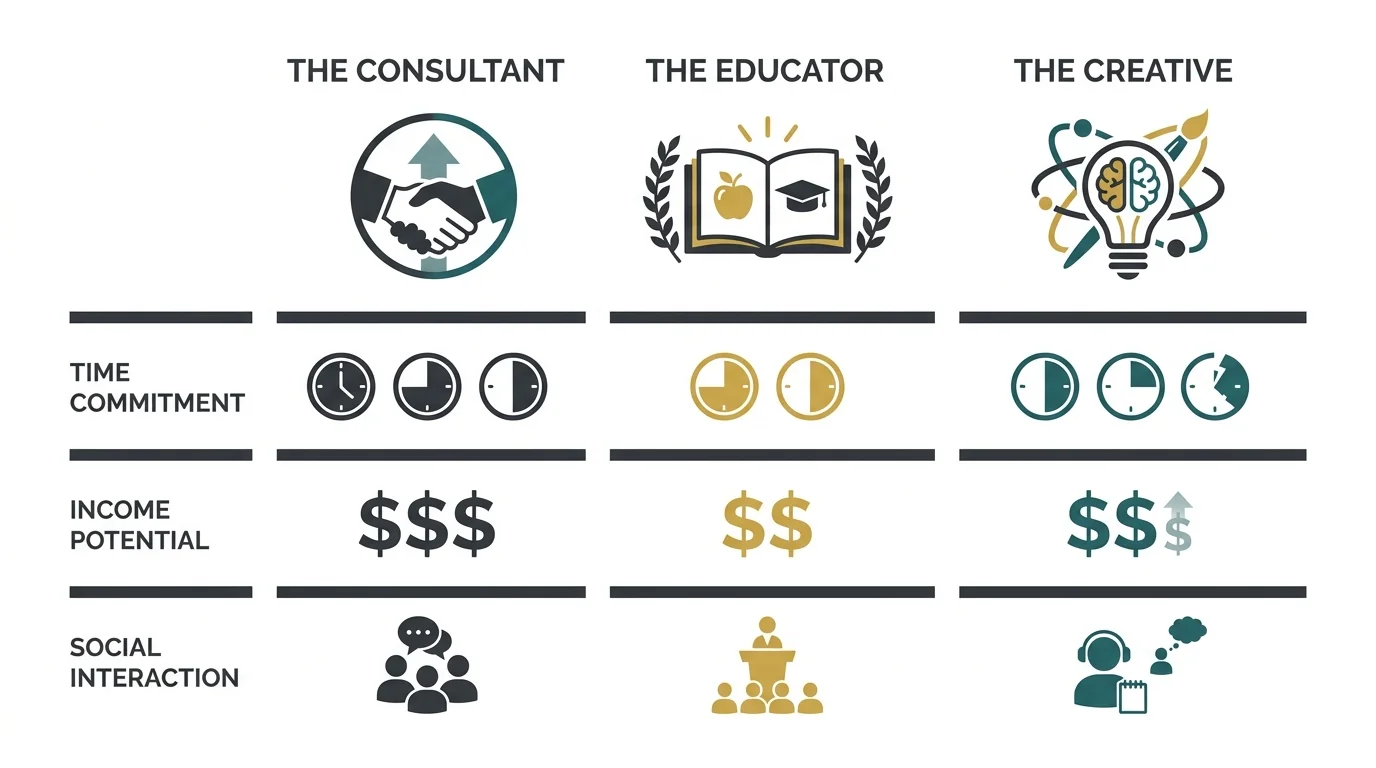

Comparing Popular Retirement Job Paths

When you decide to step back into the professional world, the sheer variety of options can feel overwhelming. Choosing the right path requires balancing your desire for income with your need for schedule flexibility and social interaction. Use the comparison below to weigh the most common avenues for older workers.

| Career Path | Schedule Flexibility | Income Potential | Primary Benefit |

|---|---|---|---|

| Industry Consulting | High (You set client meetings and project deadlines) | High (Leverages specialized decades of expertise) | Maintains professional identity while maximizing hourly rate. |

| Retail & Hospitality | Medium (Shift-based, often willing to accommodate part-time) | Low to Medium (Typically hourly wage) | Provides immediate, vibrant social interaction and gets you out of the house. |

| Gig Economy (Rideshare, Delivery, Freelance Writing) | Extreme (Work exactly when you want, log off instantly) | Medium (Directly tied to the hours you choose to grind) | Absolute autonomy over your day-to-day schedule. |

| Non-Profit & Teaching | Medium to Low (Requires adherence to organizational schedules) | Low to Medium (Mission-driven rather than profit-driven) | Delivers massive emotional fulfillment and community impact. |

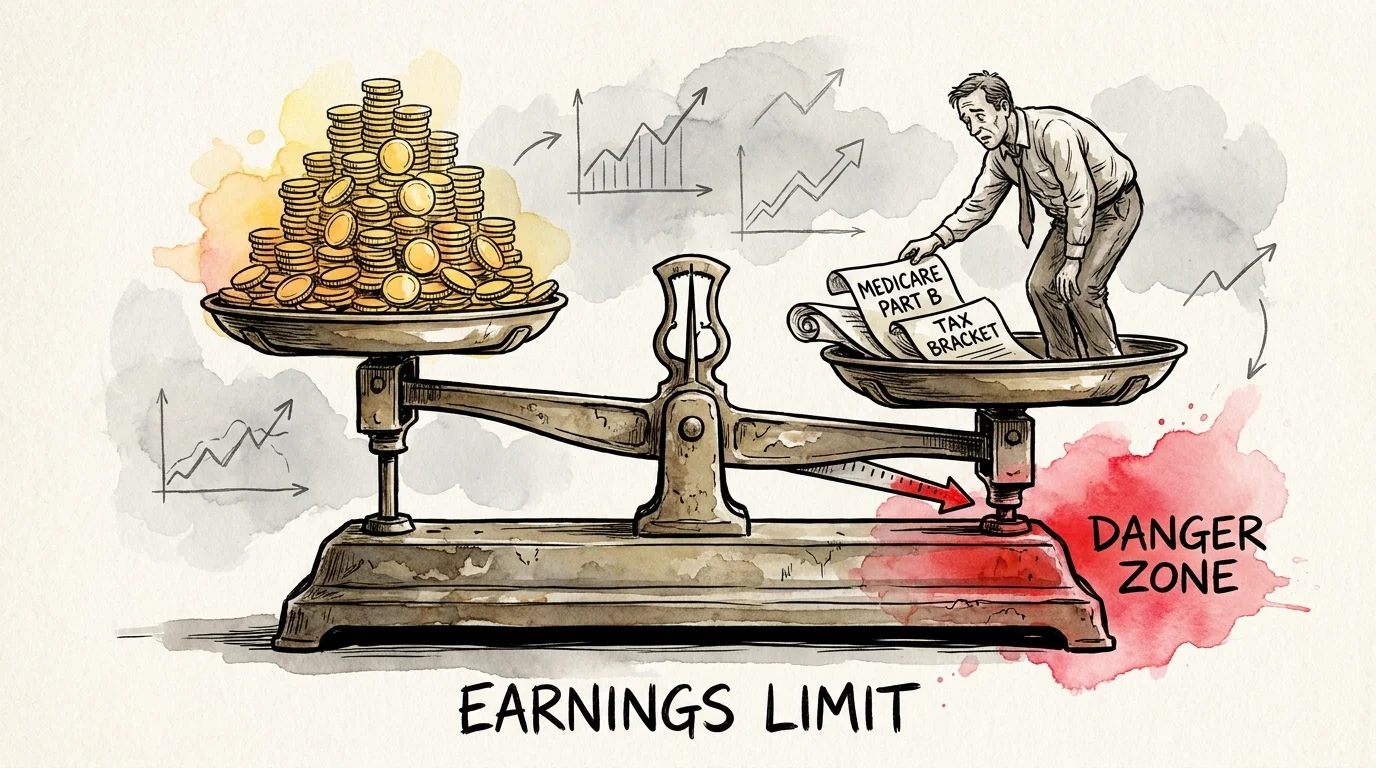

Costly Mistakes to Avoid When Working in Retirement

Jumping back into the workforce requires careful navigation of the rules surrounding government benefits. Earning income as a retiree fundamentally changes your tax profile and can inadvertently penalize you if you ignore the fine print. Protect your hard-earned benefits by steering clear of these common pitfalls.

Triggering the Social Security Earnings Test

If you claim Social Security before your Full Retirement Age (FRA) and continue to work, the government places a strict cap on how much you can earn. Once your wages exceed this annual limit, the SSA temporarily withholds a portion of your benefits—typically $1 for every $2 earned above the threshold. While you eventually recoup this money after reaching FRA, the sudden reduction in your monthly check catches many retirees off guard. Always verify the current year’s earnings limit on SSA.gov before accepting a high-paying role if you have already claimed benefits early.

Stumbling into IRMAA Medicare Surcharges

Medicare premiums are not flat fees for everyone. If your new career pivot proves incredibly lucrative, your increased Adjusted Gross Income (AGI) might trigger the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge dramatically increases your Medicare Part B and Part D monthly premiums. Because IRMAA uses a two-year lookback period, the high income you earn today will inflate your Medicare costs two years down the road. Consult with a tax professional to ensure your second career does not inadvertently double your healthcare premiums.

Overcommitting Before Testing the Waters

The enthusiasm of a new venture often tempts retirees to sign up for forty-hour workweeks right out of the gate. Your energy levels and lifestyle priorities differ immensely from your thirties. Committing to a grueling schedule immediately often leads to rapid burnout, defeating the purpose of a balanced retirement. Always start with a modest ten to fifteen hours a week. You can easily scale your hours upward if you enjoy the work, but walking back a heavy commitment damages professional relationships and causes unnecessary stress.

“Retirement is not the end of the road. It is the beginning of the open highway.”

Actionable Steps to Launch Your Second Act

Recognizing the signs is only the first part of the journey; translating that realization into forward momentum requires a tactical approach. Follow these structured steps to transition smoothly into your new role.

- Conduct a Skills Audit: Write down every hard and soft skill you acquired over your career. Strip away your previous job titles and focus strictly on what you know how to do. A project manager might rebrand as an organizational consultant; a teacher might pivot to corporate training.

- Update Your Digital Presence: Dust off your LinkedIn profile. Ensure your summary reflects your current goals, highlighting that you seek flexible, project-based, or part-time opportunities. Emphasize your reliability and depth of experience—traits modern employers desperately need.

- Tap Your Existing Network: Reach out to former colleagues, vendors, and clients. Inform them you are taking on select projects. The vast majority of high-quality consulting and part-time roles materialize through warm introductions rather than cold job boards.

- Utilize Senior-Focused Resources: Explore platforms dedicated to older adults. Organizations like AARP maintain robust job boards featuring employers specifically committed to hiring experienced workers, allowing you to bypass companies with ageist hiring practices.

- Set Rigid Boundaries: Before you accept any position, define your absolute limits. Decide exactly which days you will not work and the minimum hourly rate you will accept. Guard your leisure time fiercely so your new career enhances your retirement rather than consuming it.

Frequently Asked Questions About Second Careers

Will working part-time affect my existing pension?

In most private sector scenarios, earning external income does not impact your vested pension benefits. However, if you retired from a government position (federal, state, or municipal) and return to work for the same government entity, your pension payments could be suspended or reduced. Always review your specific pension plan documents or speak with your former HR department before accepting a role within the same system.

Do I still pay payroll taxes if I work while receiving Medicare and Social Security?

Yes. Regardless of your age or whether you currently draw Social Security and Medicare benefits, you must continue paying FICA taxes (Social Security and Medicare payroll taxes) on any earned income. Your employer will deduct these automatically, or you must pay them via self-employment taxes if you operate as an independent contractor.

How do I overcome age discrimination during the interview process?

Combat age bias by shifting the narrative from your age to your unparalleled ability to solve problems immediately. Employers fear that older workers may lack tech-savvy or resist new management styles. Pre-empt these concerns by naturally weaving examples of recent software adoption into your conversation and emphasizing your enthusiasm for collaborating with multi-generational teams. Frame your decades of experience as a stabilizing asset that requires zero hand-holding.

Embrace the Next Chapter on Your Terms

Retirement represents a blank canvas, not a finish line. Recognizing that you need more stimulation, income, or social connection is a sign of vitality, not a failure to enjoy your golden years. Stepping back into the professional arena allows you to rewrite the rules of work. You hold the power to choose roles that align perfectly with your passions, dictate a schedule that accommodates your travel plans, and walk away from environments that cause unnecessary stress. Take a few hours this week to outline what your ideal part-time role looks like, update your resume, and begin floating your availability to your network. Your expertise remains highly valuable—it is time to put it to use exactly how you see fit.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Medicare rules, Social Security benefits, and tax laws change regularly—verify current details at Medicare.gov, SSA.gov, or with a licensed professional.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.