Maintaining a four-bedroom family home long after the kids have moved out quietly drains your retirement savings and consumes the energy you should be spending on your post-career dreams. Selling that oversized property and moving into a more manageable space acts as a financial and lifestyle accelerator, instantly freeing up equity, lowering monthly fixed costs, and eliminating endless weekend maintenance chores. By intentionally shrinking your square footage, you can redirect thousands of dollars annually toward the experiences that actually matter to you. Downsizing isn’t about giving up your comfort or settling for less; it is a strategic maneuver to reclaim your time and dramatically speed up the timeline for achieving your most ambitious retirement objectives.

1. Maximize Your Retirement Income Streams

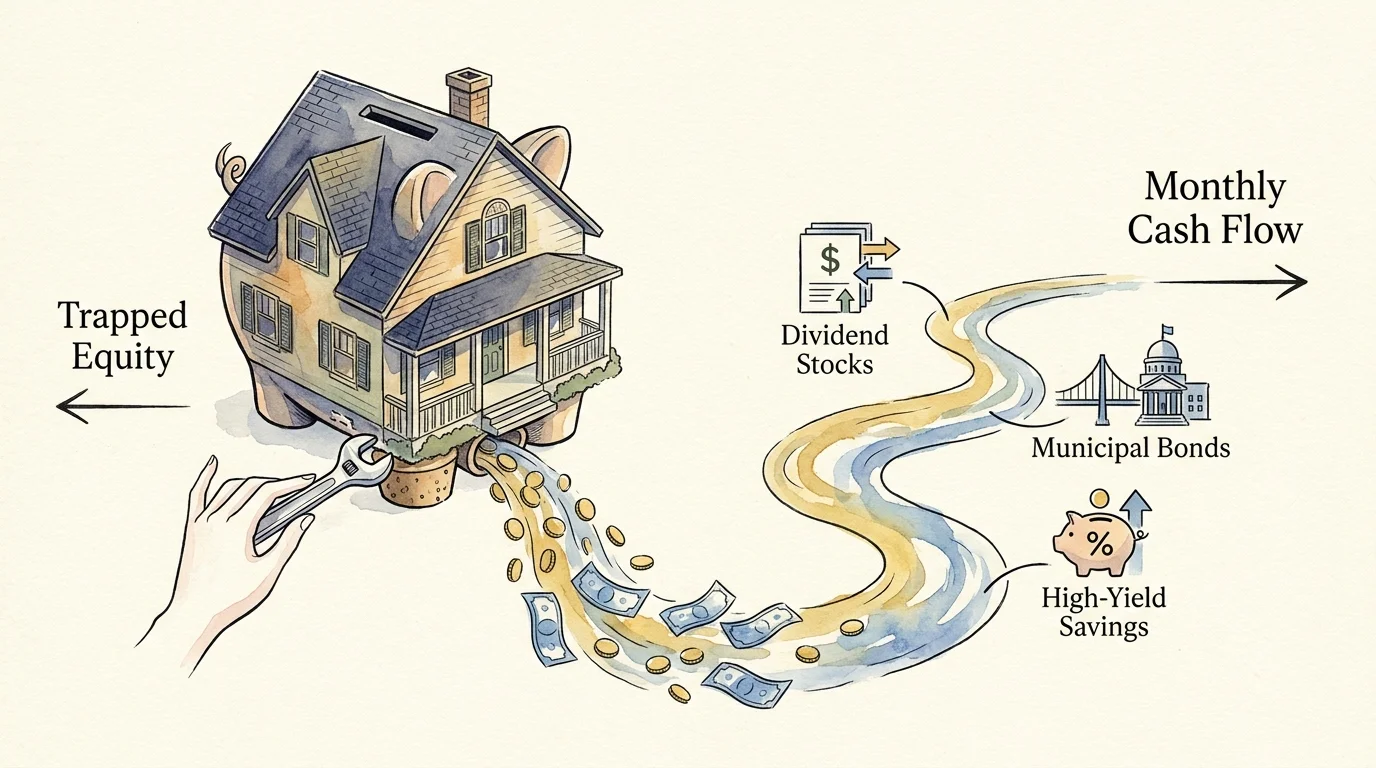

Your primary residence likely represents a massive portion of your net worth, yet it produces zero income. It actually demands constant cash infusions for upkeep, taxes, and insurance. Selling a high-value family home and purchasing a smaller property—or renting an apartment—allows you to extract hundreds of thousands of dollars in trapped equity. You can immediately redirect this capital into income-producing assets like dividend-paying stocks, municipal bonds, or high-yield savings accounts. Creating a predictable monthly cash flow from your home equity transforms your financial picture, giving you the liquid assets necessary to fund hobbies, dining out, and daily comforts without constantly stressing over portfolio withdrawals.

2. Eliminate Mortgage Debt Completely

Entering your senior years with a sizable mortgage puts immense pressure on your fixed income. A primary goal for millions of older adults is living completely debt-free, but reaching that milestone while making payments on a thirty-year loan for a massive house takes decades. Downsizing offers a spectacular shortcut. By taking the equity from your current home, you can often purchase a townhome, condominium, or smaller single-family house entirely in cash. Wiping out your largest monthly expense frees up a massive portion of your Social Security and pension checks, ensuring your money works directly for your lifestyle rather than enriching a bank’s interest margins.

3. Unlock Genuine Location Independence for Senior Travel

Extended travel requires a home base that runs on autopilot. If you own a large property with expansive lawns, a pool, and aging infrastructure, you cannot simply pack your bags and leave for a month without orchestrating a team of caretakers to mow the grass, pick up mail, and ensure pipes do not freeze. Moving into a low-maintenance community or a condominium establishes a true “lock and leave” lifestyle. The homeowners association handles exterior maintenance while you explore European river cruises, visit national parks in an RV, or spend winters in a warmer climate. Downsizing removes the physical tether keeping you anchored to one zip code.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

4. Optimize Your Environment for Aging in Place

The family home where you raised children often contains hidden hazards for an aging body: steep wooden staircases, narrow hallways, sunken living rooms, and slippery bathtub combinations. Waiting for a mobility crisis to modify these obstacles usually proves extremely expensive and stressful. Proactive downsizers achieve the goal of safe, long-term independence by moving to a single-story residence designed with accessibility in mind. Look for properties featuring zero-step entries, walk-in showers with grab bars, wide doorways that easily accommodate walkers, and open floor plans. Creating an environment tailored to your current and future physical needs dramatically reduces the risk of falls and delays or prevents the need for assisted living facilities.

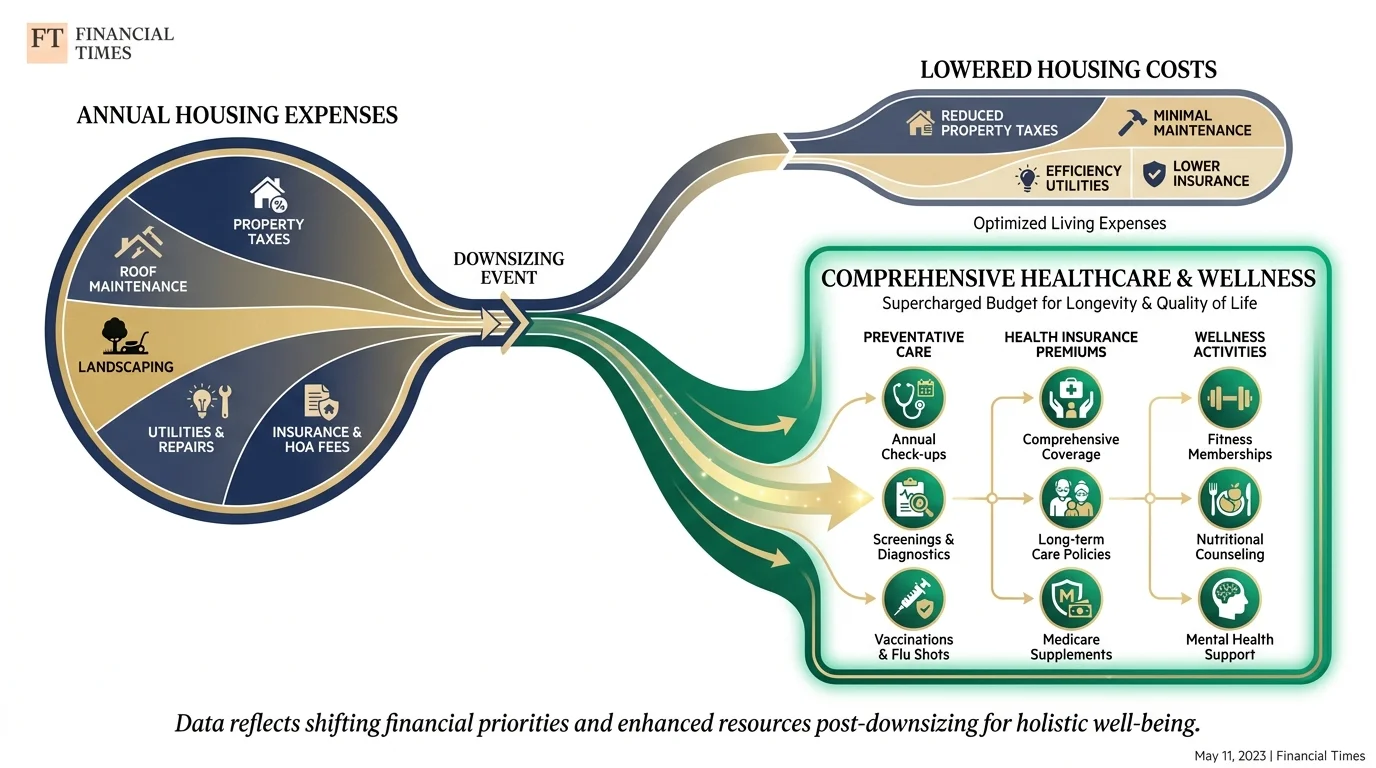

5. Supercharge Your Healthcare and Medical Budget

Healthcare ranks as one of the largest expenses you will face in your later years. Premiums for supplemental insurance, copayments for specialists, and out-of-pocket costs for dental and vision care add up rapidly. When you slash your housing expenses by moving to a smaller footprint, you create a dedicated surplus in your monthly budget. You can use these newfound funds to upgrade your medical coverage. Instead of settling for bare-minimum insurance because of cost constraints, you can afford a premium Medigap policy or a comprehensive Medicare Advantage plan that offers robust networks and extensive drug coverage. Research your expanded options using the official Medicare Plan Finder to ensure your new budget aligns with top-tier health protection.

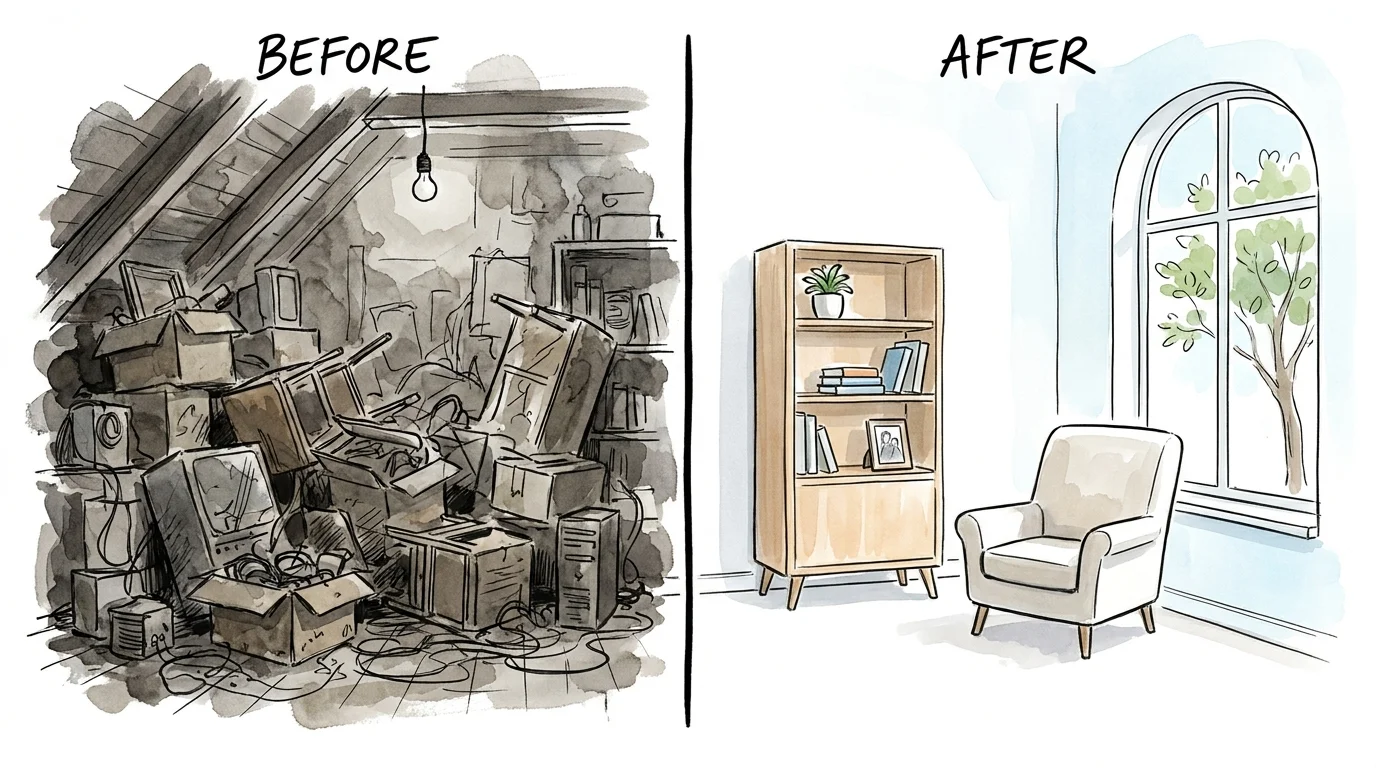

6. Simplify Daily Life and Eliminate Clutter

A large house naturally accumulates decades of possessions—most of which sit untouched in attics, basements, and spare bedrooms. The psychological weight of managing, cleaning, and organizing this much inventory takes a severe toll on your mental energy. Forcing yourself to downsize requires a rigorous decluttering process where you must evaluate what items genuinely serve your present life. Shedding old furniture, outdated clothes, and unnecessary knick-knacks creates a physically and mentally lighter existence. You achieve the goal of a simplified, peaceful daily routine when you only surround yourself with the belongings that bring you actual joy and utility today.

7. Provide Meaningful Financial Gifts to Family Early

Many parents plan to leave their home to their children as an inheritance after they pass away. However, adult children often need financial assistance long before that happens—whether to fund a grandchild’s college tuition, put a down payment on their own first home, or pay off high-interest medical debt. Cashing out the equity of a large property now allows you to distribute a portion of your wealth while you are still alive to witness the positive impact it makes. Watching your family benefit from your financial legacy in real-time provides immense emotional satisfaction that a post-mortem transfer simply cannot match.

8. Relocate to a Tax-Friendly State or Active Community

High property taxes and state income taxes consume a large percentage of retirement funds in places like New Jersey, Illinois, and California. Downsizing presents the perfect opportunity to relocate entirely. Moving to a state with no income tax or highly favorable retiree tax exemptions helps your savings last decades longer. Furthermore, moving out of an isolated suburban neighborhood into a 55+ active adult community instantly connects you with peers who share your schedule and interests. Organizations like AARP frequently highlight how geographic relocation improves social engagement and staves off the loneliness that plagues many seniors who age in place in empty, quiet neighborhoods.

9. Build a Bulletproof Shield Against Inflation

When inflation drives up the cost of electricity, natural gas, water, and building materials, owners of large homes suffer the most. Heating and cooling three thousand square feet requires massive energy consumption, and replacing a massive roof costs a small fortune. A smaller home naturally acts as an inflation hedge. Two-bedroom townhomes cost a fraction of the price to keep comfortable during extreme weather. Exterior maintenance liabilities drop drastically. By shrinking your resource consumption, you insulate your fixed income against volatile economic conditions and unpredictable price spikes.

“The goal of retirement is to live off your assets—not live off your regrets.”

The Hidden Costs: Keeping the Family Home vs. Downsizing

To fully grasp the financial acceleration downsizing provides, compare the structural expenses of maintaining a typical four-bedroom house versus moving to a modern two-bedroom condominium or smaller home.

| Expense Category | Staying in the Large Family Home | Downsizing to a Smaller Property |

|---|---|---|

| Property Taxes | Constantly rising based on high assessed property value and large land footprint. | Significantly reduced due to smaller square footage and lower overall valuation. |

| Utility Bills | High costs to heat, cool, and illuminate unused bedrooms and large living areas. | Drastically lower energy requirements; highly efficient temperature control. |

| Maintenance & Repairs | Expensive roof replacements, extensive exterior painting, and major landscaping demands. | Minimal exterior responsibilities; often entirely managed by an HOA or property management. |

| Homeowners Insurance | High premiums to cover massive replacement costs and liability for large properties. | Lower premiums due to reduced rebuild costs and limited personal property coverage needs. |

| Time Investment | Requires hours of weekly cleaning, yard work, and contractor management. | Frees up dozens of hours per month for hobbies, family, and travel. |

Errors That Cost Retirees Thousands

While the benefits of moving to a smaller footprint are massive, poor execution quickly erodes the financial gains. Avoid these costly missteps when planning your transition:

- Ignoring Capital Gains Tax: The IRS allows single filers to exclude up to $250,000 (and married couples up to $500,000) of capital gains on the sale of a primary residence, provided you have lived there for two of the past five years. If your home has appreciated wildly beyond these limits, failing to plan for the tax bill can shock your budget.

- Underestimating Moving and Furnishing Costs: Packing, hiring professional movers, and preparing a home for sale requires cash upfront. Furthermore, your massive sectional sofa likely will not fit in a new condo living room. Budget accordingly for new, appropriately scaled furniture.

- Miscalculating HOA Fees: Moving to an active senior community lowers individual maintenance costs, but Homeowners Association fees can be steep and are subject to annual increases. Always review the HOA’s financial reserves before purchasing to avoid sudden special assessments.

- Waiting Until a Crisis Forces the Move: Attempting to declutter, sell a home, and relocate while recovering from a stroke or a broken hip is a nightmare scenario. You lose your negotiating leverage and the physical stamina required to manage the project effectively.

When to Get Expert Help

Downsizing is not just a real estate transaction; it is a major wealth transfer and lifestyle pivot. Before listing your property, assemble a team of professionals to protect your interests. Work with a financial advisor to determine exactly how to invest your newfound home equity to minimize taxes and maximize monthly income. An elder law attorney can assist in updating your estate plan to reflect your new assets and living situation.

If you are struggling to find affordable housing options that fit your fixed income, leverage government resources. You can explore the Eldercare Locator to find local aging agencies that provide housing assistance, or review HUD Housing for Seniors for subsidized apartments and supportive housing programs tailored to older adults.

Frequently Asked Questions About Downsizing

When is the absolute best time to downsize for retirement?

The optimal time to downsize is roughly two to three years before you actually stop working, or immediately upon entering retirement while you are still in excellent physical health. Moving while you still have energy allows you to handle the arduous decluttering process and emotionally adjust to your new surroundings without the added stress of physical limitations.

Should I downsize or consider a reverse mortgage to stay in my home?

This depends entirely on your goals. A reverse mortgage allows you to tap your home equity to supplement your income without moving, which is ideal if your current home is already single-story, accessible, and deeply tied to your social support network. However, a reverse mortgage does not solve the problems of expensive utility bills, exhausting yard work, or the isolation of living in a large, empty house. If you want lower maintenance and a fresh start, downsizing is the superior choice.

Will downsizing negatively impact my Social Security or Medicare benefits?

Selling your primary residence does not directly reduce your Social Security monthly benefit amount. However, if the sale generates a massive capital gain that pushes your Modified Adjusted Gross Income (MAGI) over certain thresholds, you may be subject to the Medicare Income-Related Monthly Adjustment Amount (IRMAA). This temporary surcharge increases your Medicare Part B and Part D premiums for one year. Consult a tax professional to time your sale strategically.

Take an honest inventory of your current home this week. Walk through the spare bedrooms, inspect the attic, and tally up your last twelve months of utility and maintenance bills. If the house demands more from you than it gives back, it is time to start planning your exit strategy. Moving to a smaller space unlocks the capital and freedom required to live a larger, more fulfilling retirement.

Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.