Rising living costs are prompting older Americans to rethink their retirement income, but the perfect solution might already be sitting in your attic. Tapping into the hidden value of your belongings is an incredibly effective way to generate extra cash while simultaneously downsizing your living space. In 2026, the secondhand market is booming as younger generations reject disposable goods in favor of vintage and practical items. Whether you want to fund a dream vacation, cover a surprise medical bill, or build a comfortable cash buffer, strategically liquidating unused assets provides immediate financial relief. Here are the nine most profitable things retirees are successfully turning into cash right now to permanently boost their financial security.

1. Vintage Kitchenware and Mid-Century Decor

The nostalgia economy is thriving, and items you received as wedding gifts decades ago are highly sought after by younger buyers. Brands like Pyrex, Corelle, and vintage Tupperware command impressive prices on the secondary market. Buyers actively hunt for specific patterns—such as Pyrex’s Pink Gooseberry or Butterprint—to complete their collections.

Rather than donating these items or tossing them in a yard sale box for a dollar, take the time to research their current market value. Clean the glass carefully, avoid using abrasive scrubbers that damage the original paint, and list them on dedicated online marketplaces or local collector groups. You might find that a single casserole dish funds a week’s worth of groceries.

2. Specialized Crafting Supplies and Professional Tools

Hobbies change as we age; the woodworking tools or professional-grade sewing machines you used faithfully for years might currently be collecting dust. Instead of letting high-quality equipment deteriorate, savvy retirees are passing these items on to the next generation of creators.

High-quality hand tools, power tools, drafting equipment, and extensive crafting stashes hold immense residual value. Older tools manufactured in the mid-to-late 20th century are particularly valuable because they were built with durable metals rather than the plastic components commonly used today. Professional-grade items from brands like Snap-on, Delta, or Bernina retain incredible resale value.

3. Real Wood Furniture and Heirloom Pieces

Modern consumers are experiencing massive fatigue with particleboard furniture that falls apart after one move. As a result, the demand for solid wood furniture—particularly mid-century modern pieces made of teak, walnut, and solid oak—has skyrocketed.

If you are downsizing to a smaller condo or moving into an active adult community, your heavy dining sets, credenzas, and bedroom suites are prime candidates for liquidation. To maximize your profit, consider these steps:

- Identify the maker: Look for manufacturer marks inside drawers or on the back panels.

- Take excellent photos: Clear, well-lit photos taken during daylight hours dramatically increase buyer interest.

- Be honest about wear: Documenting minor scratches builds trust with potential buyers.

- Use local platforms: Furniture is expensive to ship, making local consignment stores or neighborhood apps the most profitable route.

4. Nostalgic Media: Vinyl Records, DVDs, and Retro Gaming

Physical media has made a massive comeback. If you have boxes of vinyl records, cassettes, or classic video game consoles sitting in a closet, you possess highly liquid assets. Younger generations are eager to own physical copies of their favorite media, driving up prices for items that were considered obsolete just a decade ago.

While standard classical or big band records might not fetch a premium, classic rock, jazz, soul, and 1980s pop vinyl are reliable sellers. Furthermore, if you kept your children’s old Nintendo or Sega systems from the 1990s, complete with the original games and cords, you are holding onto prime collector items.

5. Unworn Fine Jewelry and Luxury Watches

Tastes in jewelry evolve over a lifetime. Many retirees find themselves holding onto heavy gold chains, inherited brooches, or luxury watches that spend 364 days a year locked in a safe. With precious metal prices remaining historically high in 2026, liquidating unworn jewelry is one of the fastest ways to generate a significant lump sum of cash.

Before selling fine jewelry, secure an independent appraisal to understand the piece’s true value. Avoid mail-in cash-for-gold operations; instead, work with reputable local jewelers or auction houses that will evaluate the piece for its craftsmanship rather than just its melt value.

6. Unused Vehicles, RVs, and Boats

Owning multiple vehicles made sense during your working years, but maintaining a secondary car, RV, or boat in retirement often becomes a financial drain. Between insurance premiums, registration fees, maintenance, and storage costs, unused vehicles quietly erode your monthly budget.

Selling a secondary vehicle not only provides a massive immediate cash injection but also permanently lowers your ongoing monthly expenses. This dual benefit creates a powerful boost to your retirement cash flow. As the used vehicle market remains robust, liquidating an idle camper or boat is a highly practical financial move.

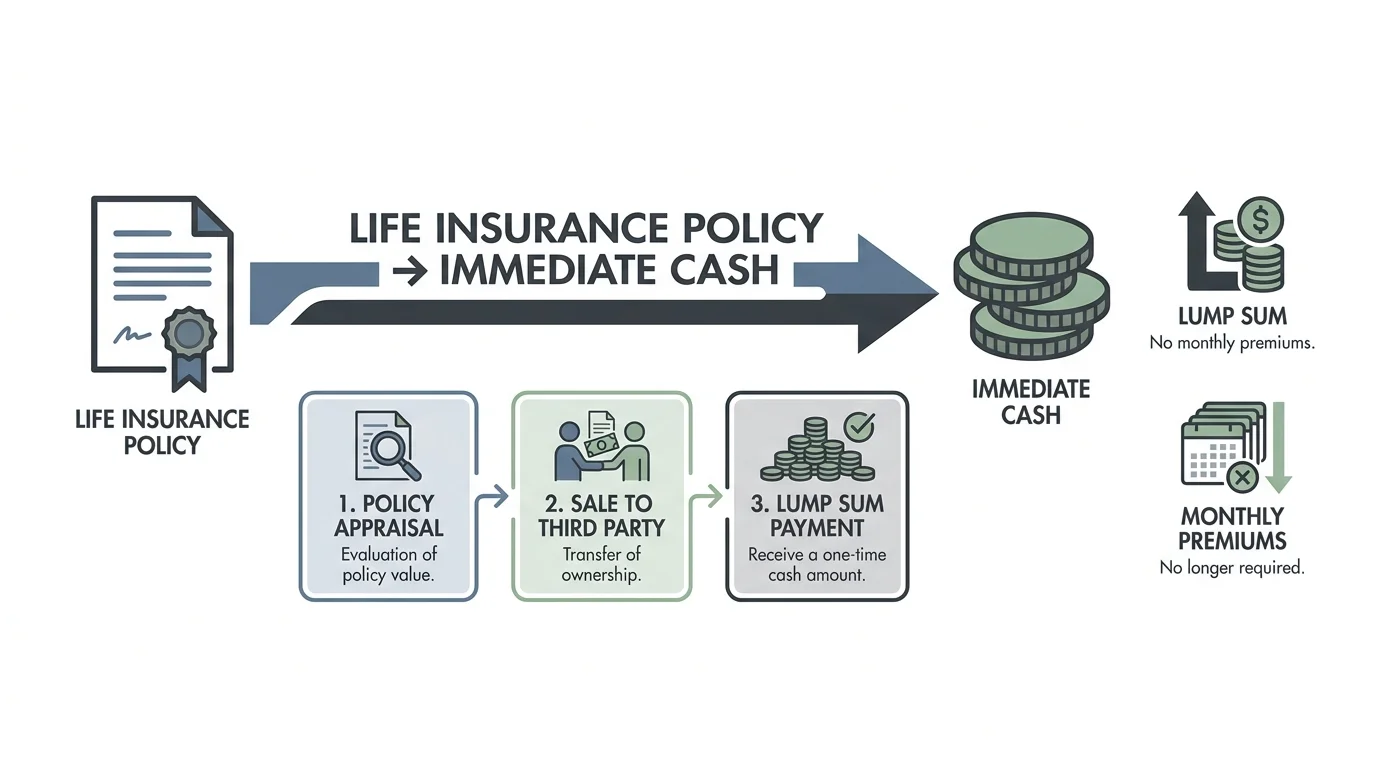

7. Life Insurance Policies (Life Settlements)

Many seniors are unaware that their life insurance policy is a piece of personal property that can be sold. If you no longer need the death benefit—perhaps your children are financially independent or your spouse has passed away—you can sell your policy to a third party through a transaction known as a life settlement.

This process yields a cash payment that is higher than the policy’s surrender value but lower than the death benefit. The buyer takes over the premium payments and eventually collects the payout. Because this is a complex financial transaction, it requires careful navigation. The Consumer Financial Protection Bureau (CFPB) provides excellent retirement planning resources to help you understand the long-term implications of selling financial assets.

8. Fine China, Crystal, and Sterling Silver

The market for traditional formal dining ware has shifted dramatically, but opportunity still exists for strategic sellers. While selling a complete 12-place setting of formal china locally can be challenging, selling individual replacement pieces is highly lucrative.

Companies that specialize in replacing broken dishes for collectors will purchase your unused plates, teacups, and crystal glasses. Sterling silver flatware (ensure it is marked “Sterling” and not just silver-plated) is always in demand for its melt value alone, though desirable patterns from major silversmiths will fetch a premium from collectors.

9. Empty Space: Renting Rooms and Storage

While not a physical item you pack in a box, empty space is a highly valuable asset you can “sell” access to. If you live in a large home with unused bedrooms or have an empty RV pad in your driveway, you can convert that space into a steady stream of passive income.

Platforms allowing you to rent out garage space for winter boat storage or a spare bedroom to a traveling nurse are incredibly popular. Organizations like AARP frequently highlight home-sharing and space-renting as innovative ways for seniors to age in place while offsetting rising property taxes and utility costs.

“The goal of retirement is to live off your assets—not live off your regrets.”

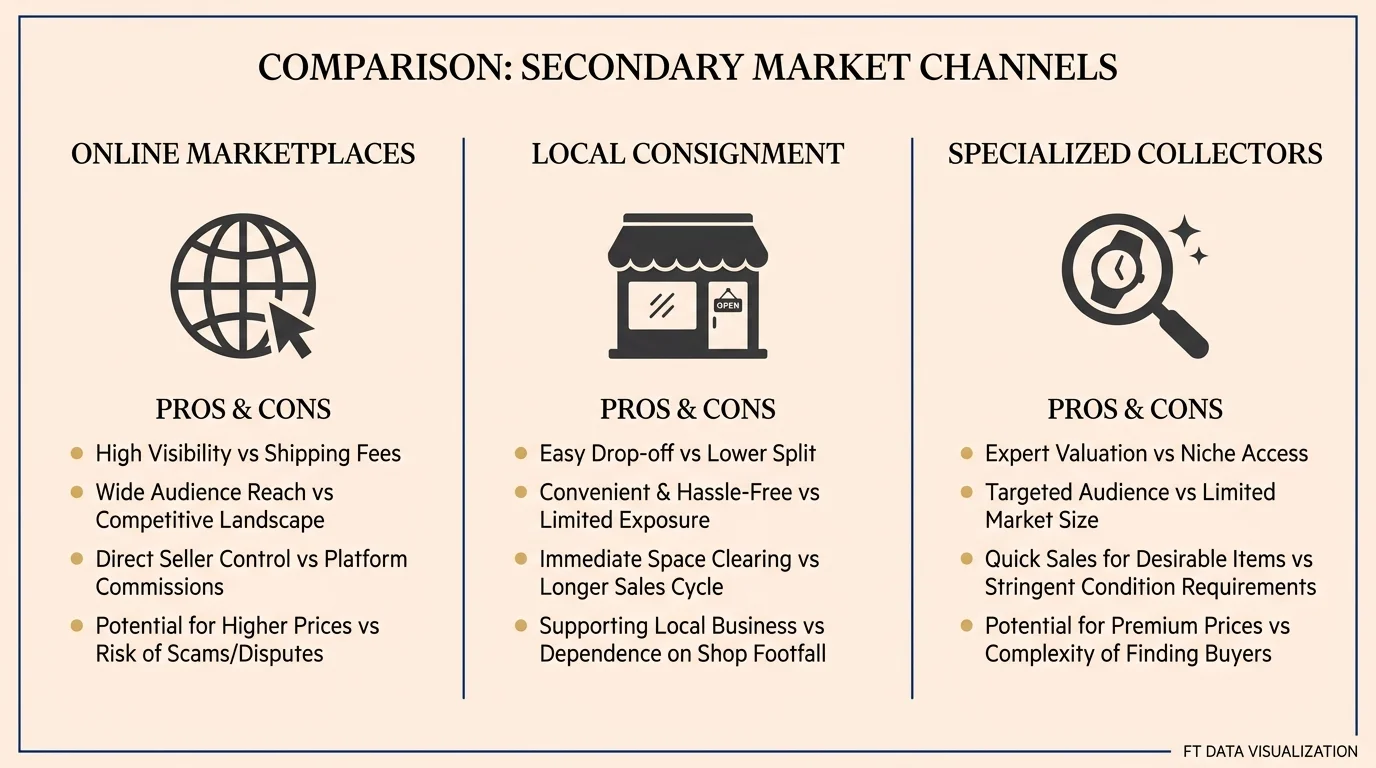

Platform Comparison: Where to Sell Your Items

Choosing the right venue for your items dictates how much profit you keep and how much effort you expend. Use this comparison to match your items with the most effective sales platform.

| Sales Platform | Best For Selling | Fee Structure | Effort Level Required |

|---|---|---|---|

| Online Marketplaces (eBay, Etsy) | Vintage decor, lightweight collectibles, specific replacement pieces, jewelry. | High (10% to 15% of final sale price). | High. Requires detailed photography, managing listings, packing, and shipping. |

| Local Apps (Facebook Marketplace) | Heavy furniture, tools, vehicles, large crafting lots. | None (Free to list and sell locally). | Medium. Involves messaging buyers and coordinating safe local pickups. |

| Local Consignment Shops | High-end clothing, antique furniture, premium home goods. | Very High (Store takes 40% to 60% commission). | Low. You drop the items off; the store handles the marketing and transaction. |

| Estate Liquidation Services | Emptying an entire home, large collections, fine art. | High (30% to 50% commission plus setup fees). | Very Low. Professionals handle appraising, pricing, and running the sale. |

Common Retirement Traps When Liquidating Assets

Generating extra cash is empowering, but the process carries distinct risks. Protect your time and money by avoiding these frequent pitfalls.

Overvaluing Based on Emotion

We all attach sentimental value to our belongings. The dining table where your family shared Thanksgiving dinners feels priceless to you, but a buyer only sees wood and hardware. Research completed sales—not active listings—to determine true market value.

Ignoring Tax Implications

Selling personal items at a loss (for less than you originally paid) generally does not trigger taxes. However, if you sell a piece of fine art, an antique, or a secondary property for a profit, you may owe capital gains tax. Keep records of your sales to avoid surprises during tax season.

Falling for Buyer Scams

When selling items online or locally, prioritize your safety. Never accept overpaid checks where the buyer asks you to wire the difference back. Deal strictly in cash or secure digital payments, and conduct local transactions in well-lit public spaces—many police stations now offer designated “safe exchange” parking spots for this exact purpose.

When to Consult a Professional

While clearing out the garage is a simple weekend project, liquidating major assets requires professional oversight. If you are considering selling a life insurance policy, real estate, or high-value collections, consult with a fiduciary financial advisor or tax professional. They will map out how a sudden influx of cash might impact your Medicare premiums (through IRMAA surcharges) or your tax bracket.

Furthermore, if you are looking for broader strategies to stretch your retirement income, utilize resources like the National Council on Aging (NCOA) to explore benefit programs that might reduce your daily expenses, lessening the pressure to sell off your assets.

Frequently Asked Questions

Do I have to pay taxes on items I sell from around my house?

Generally, no. If you sell personal items like clothing, furniture, or kitchenware for less than you originally paid for them, the IRS considers this a non-deductible personal loss, and you owe no tax. You only owe capital gains taxes if you sell an item (like a collectible, antique, or property) for a profit.

Is it better to have an estate sale or sell items individually?

It depends on your goal. If you need to clear a house quickly and lack the physical energy to manage buyers, an estate sale company is the most efficient choice, though they take a significant cut. If you want to maximize profit and have the time to research, photograph, and list items, selling individually yields much higher returns.

How do I know if my vintage items are actually valuable?

The most accurate way to check value is to search for your item on eBay and filter the results by “Sold Items.” This shows you what people are actually paying, rather than what hopeful sellers are asking. For high-end jewelry or art, hire an independent appraiser who charges a flat fee rather than a percentage of the item’s value.

Taking inventory of your belongings provides a dual benefit: a cleaner, safer living environment and a healthier bank account. Start small this weekend by tackling a single closet or a specific hobby stash. As you gain momentum, you will discover that shedding the weight of unused possessions brings a profound sense of freedom. Enjoy the extra financial breathing room, and put that newly generated cash toward a goal that genuinely enhances your retirement lifestyle.

Retirement rules, tax implications, and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.