Stepping into your post-career life should feel like opening a highly anticipated new chapter rather than navigating a financial minefield, yet easily avoidable retirement planning errors consistently derail decades of hard work. The decisions you make during your first few years out of the workforce lock in your income trajectory, determine your healthcare costs, and establish your daily quality of life. From claiming Social Security prematurely to underestimating the emotional impact of sudden abundant free time, seemingly minor miscalculations often compound into significant financial or emotional burdens. By examining these frequent missteps and learning how to bypass them, you secure the freedom and peace of mind you genuinely deserve.

1. Claiming Social Security Before Running the Numbers

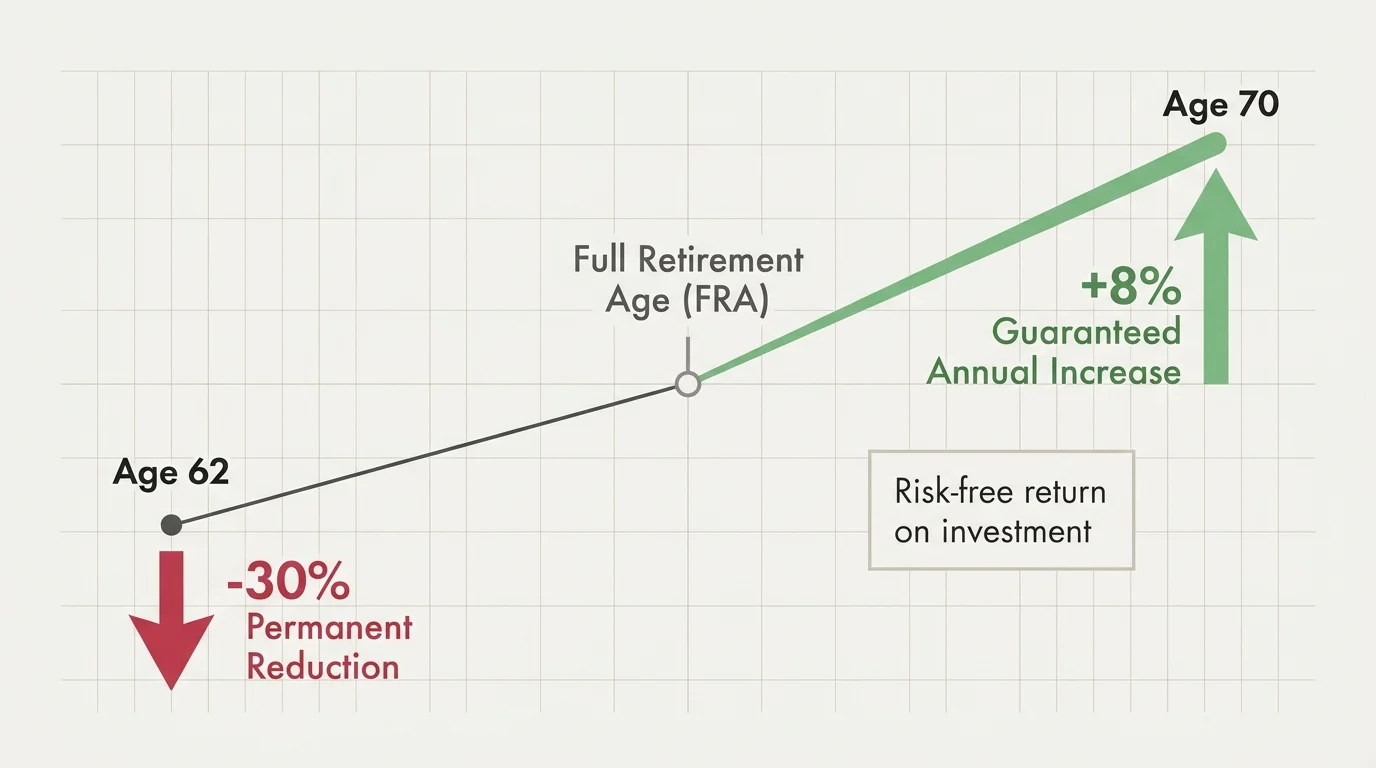

Filing for Social Security the moment you turn 62 remains one of the most persistent retirement regrets. While the appeal of immediate income tempts many Americans, claiming benefits before your Full Retirement Age (FRA) permanently reduces your monthly check by as much as 30 percent. Over a retirement that could easily span three decades, this reduction substantially limits your purchasing power during your most vulnerable years.

Alternatively, delaying your claim past your FRA earns you delayed retirement credits. Your benefit increases by a guaranteed 8 percent for every year you wait, up to age 70. This represents a robust, risk-free return on your investment that no standard market portfolio can securely match. Furthermore, if you are married, the timing of your claim directly dictates the survivor benefit your spouse will eventually receive. When the higher earner files early, they accidentally diminish the financial safety net left behind for their surviving partner.

Before submitting any paperwork, utilize the official Social Security Retirement Estimator to compare your potential monthly payouts at ages 62, FRA, and 70. Assess these figures alongside your current savings, life expectancy, and familial health history to form a deliberate, calculated strategy.

2. Misunderstanding Medicare Timelines and Coverage Limits

Healthcare costs typically represent one of your largest expenses in retirement, yet millions of seniors stumble through the Medicare enrollment process. Missing your Initial Enrollment Period—a seven-month window surrounding your 65th birthday—triggers permanent late enrollment penalties. If you miss the Part B deadline without qualifying creditable employer coverage, Medicare tacks on a 10 percent penalty to your monthly premium for every full 12-month period you could have enrolled but did not. Part D prescription drug plans carry similar lifetime penalties.

Beyond missing deadlines, retirees frequently fail to optimize their specific coverage. Selecting between Original Medicare (paired with a Medigap policy) and a Medicare Advantage plan heavily dictates your access to doctors and your out-of-pocket maximums. Choosing a plan simply because a friend recommended it ignores your unique prescription needs and preferred specialist network.

| Coverage Feature | Original Medicare (Plus Medigap) | Medicare Advantage (Part C) |

|---|---|---|

| Provider Network | See any doctor nationwide who accepts Medicare. | Must use the plan’s specific HMO or PPO network. |

| Referrals | No referrals needed for specialists. | Often require primary care referrals for specialists. |

| Out-of-Pocket Costs | Higher monthly premiums up front, but predictable, low costs for medical services. | Often zero premium, but higher copays and coinsurance when you need significant care. |

| Extra Benefits | Standard medical only (dental/vision require separate plans). | Frequently bundles dental, vision, hearing, and fitness perks. |

Review your options annually during the Open Enrollment Period using the Medicare Plan Finder. Because formularies and plan benefits shift yearly, complacency often leads to expensive pharmacy bills.

3. Making Permanent Retirement Relocation Mistakes Based on Vacation Memories

Moving to a sunny beachfront town or a remote mountain cabin sounds idyllic. However, relocating based on fond vacation memories frequently results in costly retirement relocation mistakes. A resort town in the middle of July feels entirely different from that same town during an isolated, gray February.

When retirees sell their long-time family home and permanently relocate without testing the waters, they frequently encounter unexpected challenges. High property taxes, limited access to top-tier healthcare facilities, and the emotional toll of moving away from an established social circle and grandchildren quickly turn a dream destination into an isolating experience.

Protect your peace of mind by renting in your target destination for at least six months before committing to a mortgage. This trial run exposes you to the off-season weather, the reality of the local medical infrastructure, and the daily cost of living. If the location fits your lifestyle perfectly, you can then buy with absolute confidence.

4. Exiting the Workforce Without a Clear Sense of Purpose

Financial planners spend decades telling you how to afford retirement, but few prepare you for how to actually live it. Sudden, unstructured freedom often triggers depression, anxiety, and a profound loss of identity, especially for individuals whose self-worth was deeply intertwined with their career titles.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

The honeymoon phase of retirement—sleeping in, golfing daily, or catching up on reading—usually wears off within the first year. Without daily challenges or social engagement, retirees quickly face disenchantment. Successful retirement lifestyle decisions require treating your purpose as seriously as your portfolio. Identify causes you care about, volunteer your expertise, launch a low-stress micro-business, or mentor younger professionals. Structuring your days around meaningful activities ensures your mental acuity remains sharp and your social calendar remains vibrant.

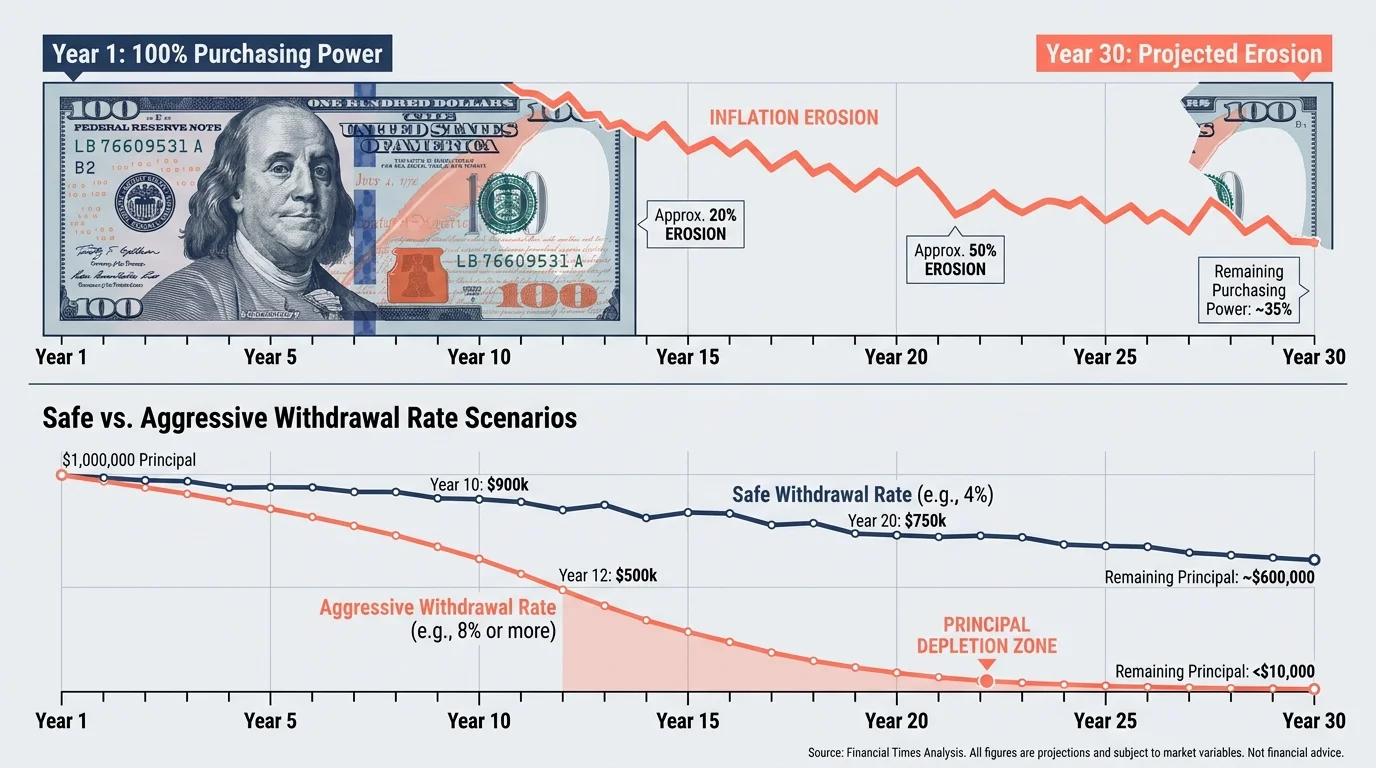

5. Underestimating the Impact of Inflation and Withdrawal Rates

Pulling too much money from your retirement accounts during your early years often causes irrevocable portfolio damage, especially if the stock market simultaneously experiences a downturn. This phenomenon, known as sequence of returns risk, forces you to sell off more shares at depressed prices just to maintain your standard of living.

“The goal of retirement is to live off your assets—not live off your regrets.”

Many retirees rigidly cling to the “4 Percent Rule,” assuming they can safely withdraw 4 percent of their initial portfolio value, adjusted annually for inflation. However, high inflationary environments and fluctuating market yields demand flexibility. Relying strictly on static formulas without adapting to the economic climate creates immense financial stress. Implement a dynamic withdrawal strategy; cut discretionary spending during bear markets and harvest gains during bull markets to ensure your nest egg outlives you.

6. Entering Your Golden Years Tethered to High-Interest Debt

Transitioning to a fixed income while servicing high-interest credit card debt or massive auto loans chokes your financial flexibility. When interest rates on consumer debt exceed 20 percent, debt payments actively erode the savings you spent decades accumulating.

Eliminate consumer debt before you officially submit your resignation letter. If you carry a mortgage, evaluate whether paying it off completely aligns with your liquidity needs. While some financial models suggest investing surplus cash rather than paying down a low-interest mortgage, the psychological relief of living entirely debt-free provides immense value. Entering retirement without mandatory debt payments drastically reduces the amount of income you need to generate, thereby lowering your tax burden and keeping your investments intact.

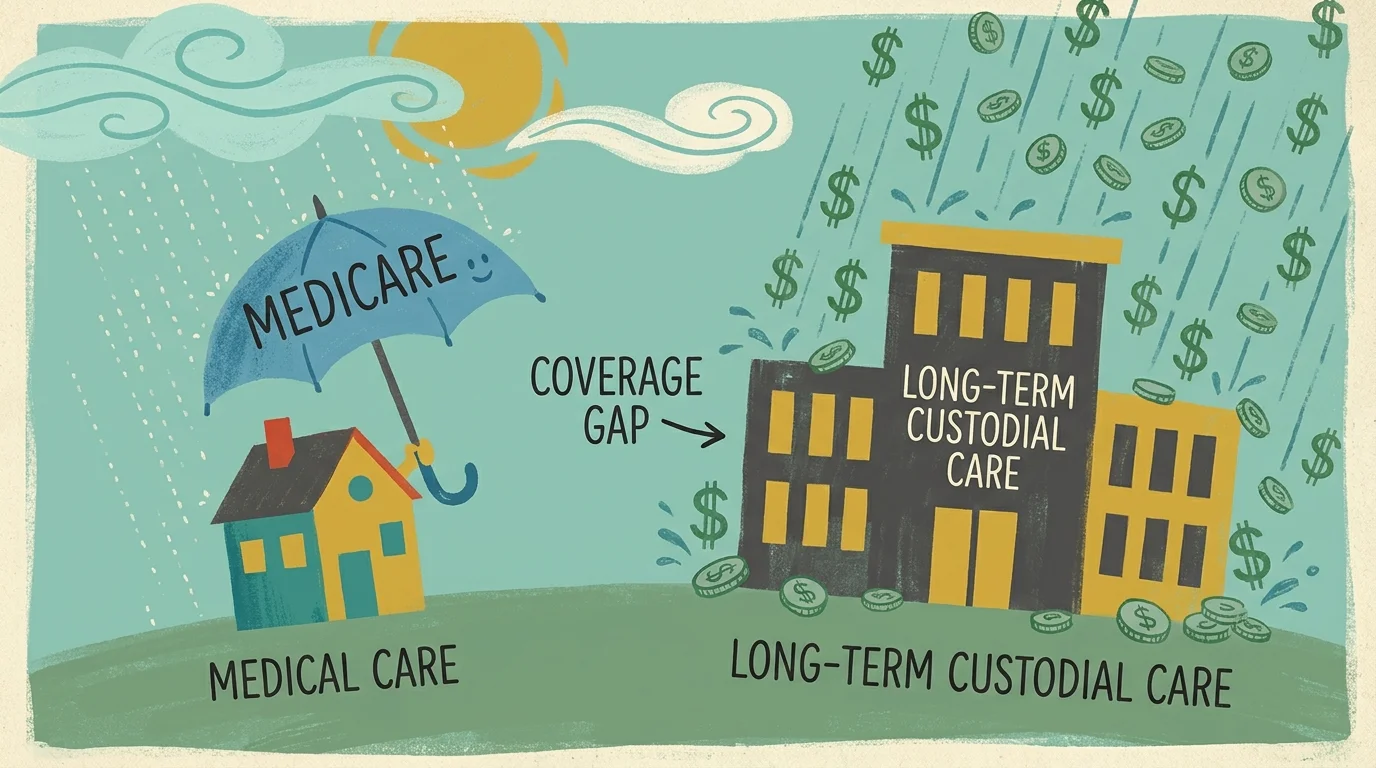

7. Assuming Medicare Covers Long-Term Custodial Care

One of the most dangerous myths in senior living assumes that Medicare acts as a safety net for nursing homes or assisted living facilities. In reality, Medicare primarily covers medically necessary acute care, such as hospital stays, doctor visits, and short-term rehabilitative care following a qualifying inpatient hospital stay. It explicitly does not cover custodial care—assistance with daily activities like bathing, dressing, and eating.

Data from the Administration for Community Living (ACL) indicates that roughly 70 percent of adults aged 65 will require some form of long-term care support during their later years. With private nursing home rooms easily exceeding six figures annually in many states, ignoring this reality decimates family estates in a matter of months.

Proactively explore your options in your late fifties or early sixties. Evaluate traditional long-term care insurance, hybrid life insurance policies with long-term care riders, or earmarked self-funding strategies. Ignoring the topic until a health crisis strikes strips you of your choices and places massive physical and financial burdens on your spouse or adult children.

8. Jeopardizing Your Financial Security to Support Adult Children

Your parental instinct naturally drives you to help your children pay off student loans, fund a lavish wedding, or cover the down payment on their first home. However, financially supporting adult children at the expense of your own retirement security frequently ends in disaster.

You cannot secure a traditional bank loan to fund your retirement, but your children have decades to pay off educational debt or build their own equity. Draining your IRA or taking out a home equity loan to solve your children’s financial problems puts your own independence at severe risk. If you run out of money at age 85, those same children will ultimately bear the burden of supporting you. Establish clear financial boundaries early. The greatest financial gift you can give your family is your own self-sufficiency.

Don’t Make These Mistakes

Beyond specific financial blunders, overarching behavioral traps frequently compromise a peaceful retirement. Avoid these common philosophical missteps:

- The “Set It and Forget It” Mindset: Never assume your initial retirement plan requires zero maintenance. Tax laws change, inflation fluctuates, and your health evolves. Review your strategy annually.

- Hoarding Your Assets Out of Fear: Frugality builds wealth, but excessive stinginess destroys your enjoyment of it. Give yourself permission to spend reasonably on experiences and travel while you have the physical health to enjoy them.

- Delaying Hard Conversations: Failing to clearly communicate your estate plans, medical directives, and end-of-life wishes guarantees chaos for your survivors. Draft your legal documents and talk to your family now.

- Letting Your Social Network Shrink: Isolation poses severe risks to cognitive and physical health. Actively cultivate friendships outside of your immediate family and former workplace.

When Professional Advice Is Worth It

While many retirees manage their affairs independently, specific transitions carry stakes too high for guesswork. Engaging professional assistance transforms a complex maze of regulations into a clear roadmap.

Consult a fee-only fiduciary financial advisor to pressure-test your portfolio withdrawal strategy and execute complex Roth conversions. When structuring your estate, utilize an elder law attorney to protect your assets from long-term care spend-downs and draft durable powers of attorney. Finally, if you feel overwhelmed by healthcare choices, contact your local State Health Insurance Assistance Program (SHIP) through the Eldercare Locator for unbiased, localized Medicare counseling.

Frequently Asked Questions

What is the most common retirement regret?

Many seniors cite failing to plan for the emotional transition as their top regret. Leaving the workforce strips away daily structure and social interaction, leading to unexpected feelings of isolation and lack of purpose. Financially, claiming Social Security too early and missing out on decades of maximized benefits ranks highest.

Can I undo my Social Security claiming decision if I change my mind?

Yes, but the window is extremely narrow. The Social Security Administration allows you to withdraw your application and restart your benefits later, but you must do so within 12 months of your initial claim. Additionally, you must repay every dollar you and your family received during that period.

How much cash should I hold in retirement to avoid sequence of returns risk?

While individual needs vary, many financial experts recommend keeping one to two years’ worth of essential living expenses in highly liquid, safe accounts (like high-yield savings or short-term CDs). This cash buffer allows you to pay your bills during a severe market downturn without selling your equity investments at a loss.

Taking Charge of Your Next Chapter

Achieving a fulfilling, regret-free retirement relies far less on luck and much more on intentional, proactive choices. By understanding the mechanics of your benefits, testing out major lifestyle changes before committing, and treating your physical and mental health as your greatest assets, you construct a resilient foundation for your future. Take one immediate step today: log into your government benefit portals, review your actual projected numbers, and map out a realistic timeline that aligns with the life you genuinely want to live.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.