Switching to a fixed income means every dollar you spend needs to work harder for your retirement budgeting. The smartest way to offset rising costs and effectively discount everyday expenses is by maximizing cash back credit cards. Gone are the days of needing complex travel points or elite status tiers. Today’s best retiree credit cards prioritize straightforward cash rewards for groceries, gas, pharmacies, and dining. By aligning your wallet with your senior finances, you can easily generate hundreds of dollars in tax-free cash back each year. This guide cuts through the marketing noise to show you exactly which card categories fit your lifestyle best and how to avoid costly reward traps.

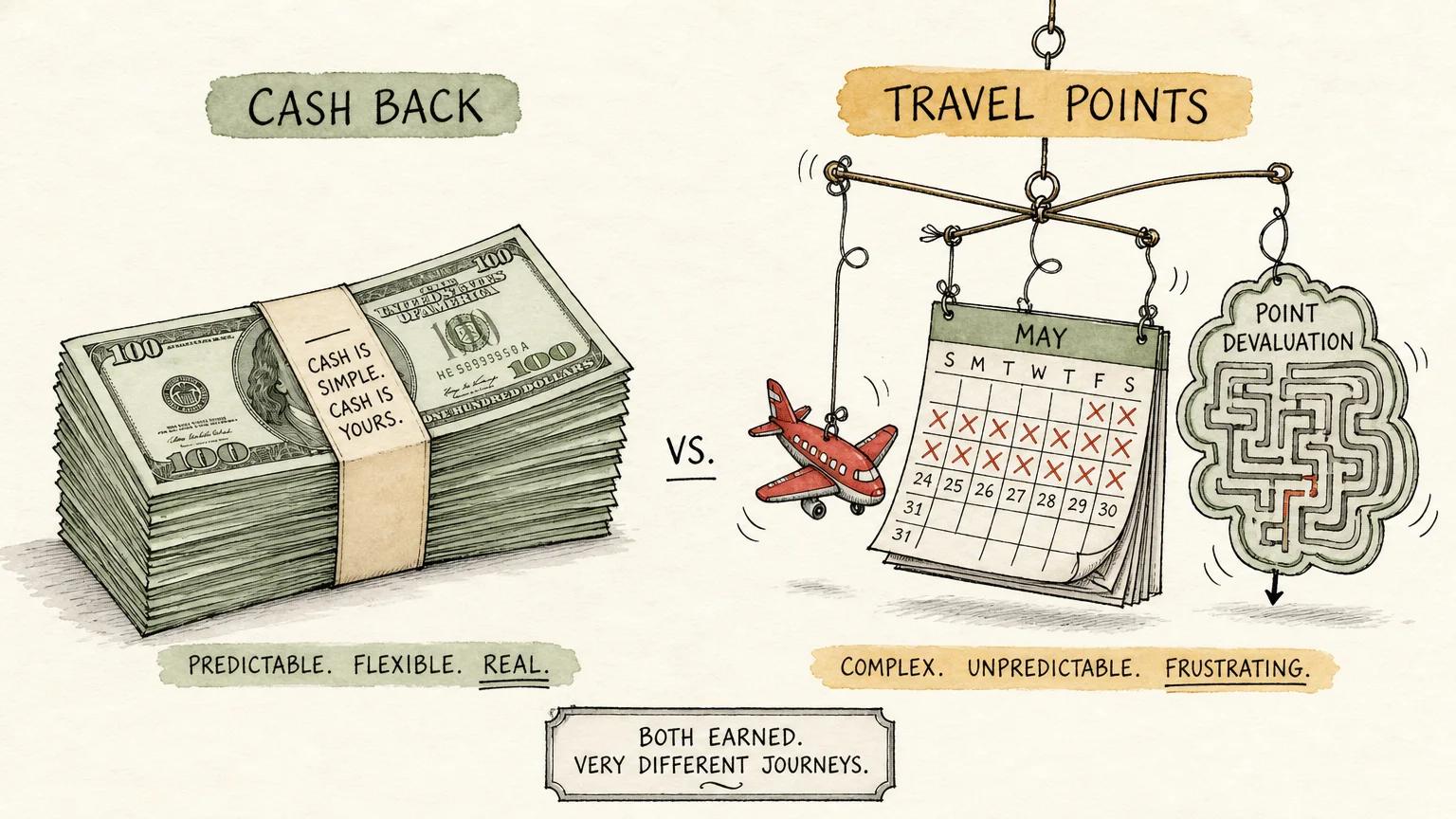

Why Cash Back Beats Travel Points for Most Retirees

During your working years, chasing airline miles and hotel points might have felt like a lucrative game. Business trips and family vacations justified premium credit cards with high annual fees and complex reward structures. Once you transition into retirement, your financial priorities fundamentally shift. Predictability and flexibility become your most valuable assets.

Travel points are inherently volatile. Airlines and hotel chains frequently devalue their rewards programs without warning; a flight that cost 30,000 miles last year might suddenly require 50,000 miles today. Furthermore, travel rewards often involve blackout dates, limited availability, and the pressure to spend more money just to redeem the points you already earned.

Cash back is entirely different. A dollar in cash back will always be worth exactly one dollar. You do not have to decipher complicated redemption charts or wait for a specific vacation to enjoy the fruits of your spending. Whether you use that cash to lower your monthly credit card bill, deposit it directly into a high-yield savings account, or use it to offset out-of-pocket medical expenses, cash back provides pure, unadulterated flexibility. For retirees managing a carefully planned budget, knowing exactly how much a reward is worth brings unparalleled peace of mind.

How to Report Income on Credit Card Applications After Retirement

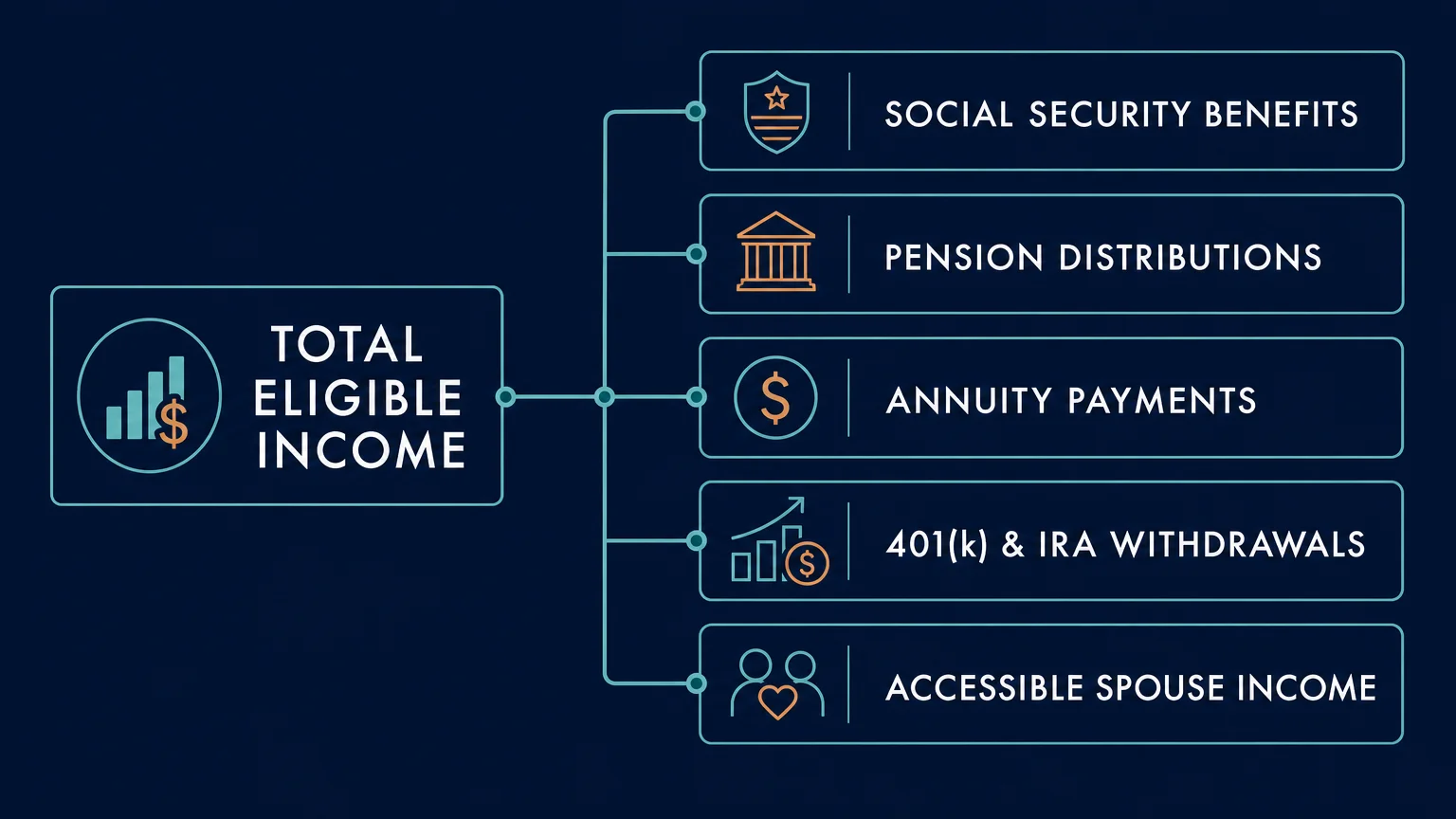

A common hurdle many retirees face is figuring out how to successfully apply for new rewards credit cards without a traditional employer W-2. You might assume that stepping away from a standard paycheck disqualifies you from prime credit offers. Thankfully, consumer protection laws allow you to include a wide variety of financial resources when an application asks for your annual income.

Under the CARD Act, applicants over the age of 21 can list any income to which they have a reasonable expectation of access. This drastically expands your options. When calculating your annual income for a credit card application, you should include your Social Security benefits, pension distributions, and annuity payments. You can also claim regular withdrawals from your 401(k), IRA, or other investment accounts. If you receive dividend income or rental property income, add that to the total.

If you are married or share household finances, you can legally include your spouse’s or partner’s income on the application, provided you have access to those funds to pay your bills. Presenting a comprehensive picture of your financial resources ensures credit issuers accurately evaluate your ability to manage a new line of credit, unlocking the best cash back offers available.

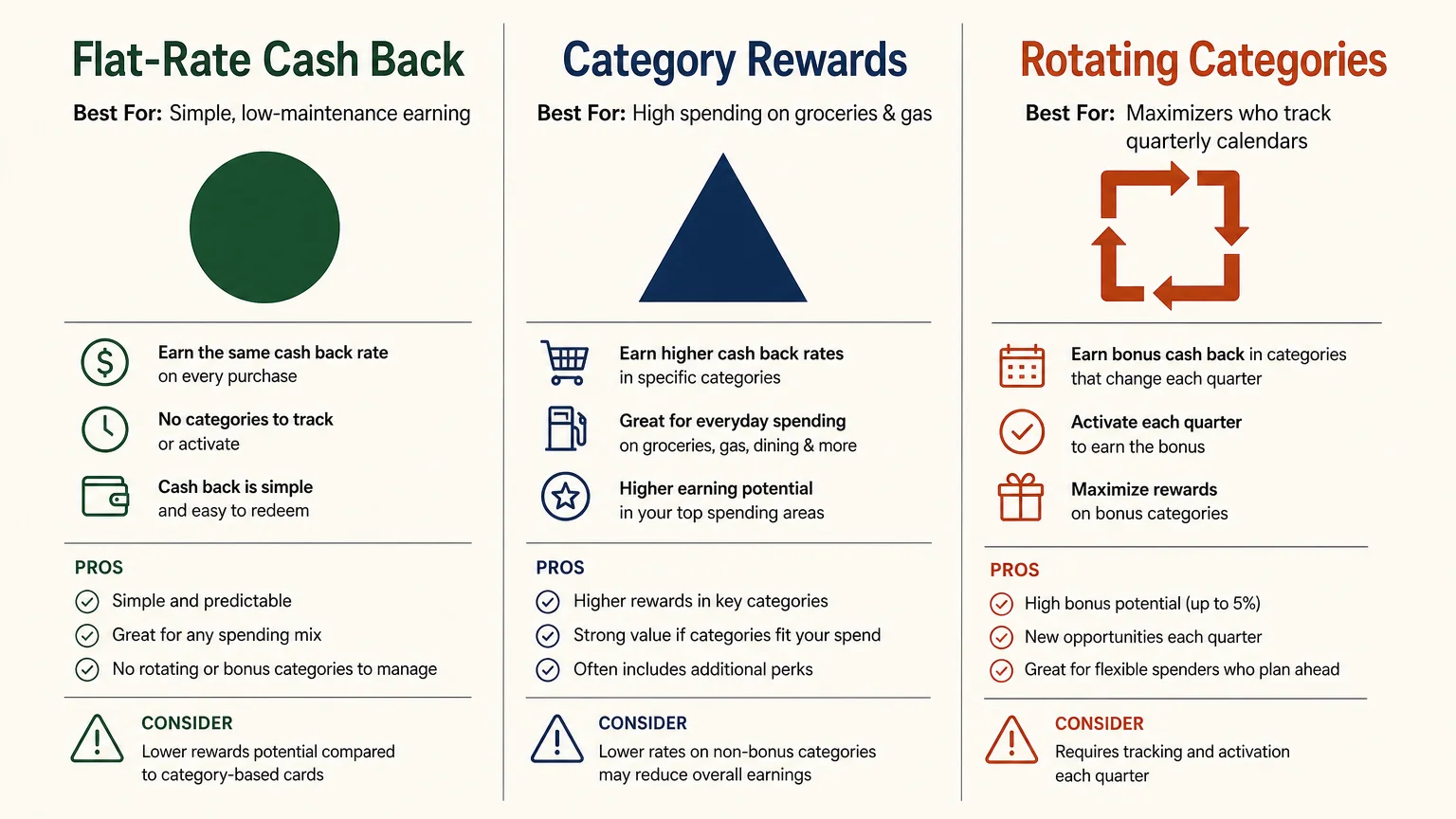

The Three Core Strategies for Earning Rewards

Not all cash back credit cards operate the same way. Issuers design their products around different spending habits, and choosing the right card means understanding how much effort you want to put into tracking your purchases. You generally have three main strategies to choose from.

| Card Strategy | Best For | Pros | Cons |

|---|---|---|---|

| Flat-Rate Cash Back | Retirees who want absolute simplicity and hate tracking categories. | Earns the exact same rate (typically 1.5% to 2%) on every single purchase. | Leaves money on the table for heavy spending in specific categories like groceries. |

| Tiered Categories | Retirees with predictable, consistent monthly budgets. | Offers high returns (3% to 6%) on specific everyday categories like supermarkets and gas stations. | Often caps the amount you can spend at the higher earning rate each year. |

| Rotating Categories | Active optimizers who enjoy maximizing every dollar. | Provides up to 5% cash back in categories that change every three months. | Requires manual activation each quarter and mental effort to remember current categories. |

Top Card Categories to Match Your Daily Routine

Rather than seeking a single perfect piece of plastic, the most successful retirees build a small, manageable collection of two or three cards that complement each other. Consider which of the following archetypes align best with your typical spending habits.

The Grocery and Pharmacy Champion

Food and healthcare represent two of the largest recurring expenses in retirement. A tiered cash back card that heavily rewards supermarket spending is arguably the most valuable tool in your wallet. Look for cards that offer between 3% and 6% cash back at U.S. supermarkets. If you spend $500 a month on groceries, a 5% cash back card generates $300 in pure savings over the course of a year. Many of these cards also offer elevated rewards at pharmacies, making them ideal for covering co-pays, over-the-counter medications, and wellness supplies.

The Flat-Rate Anchor

Every wallet needs a reliable anchor. A flat-rate card earning 2% cash back on all purchases serves as your default payment method for anything that falls outside of specialized categories. Use this card for your home repairs, auto insurance premiums, utility bills, and unexpected expenses. Because it requires zero mental gymnastics, a 2% flat-rate card guarantees you are always earning a respectable return without needing to remember where you are shopping.

The Medical Bill Strategist

Even with comprehensive Medicare coverage, you will likely encounter significant out-of-pocket healthcare costs. Dental implants, hearing aids, and vision care frequently fall outside standard coverage. When you know a large medical bill is on the horizon, consider applying for a cash back card offering a generous sign-up bonus. For instance, if a card offers a $300 cash bonus after you spend $3,000 in the first three months, putting a $3,000 dental procedure on that card yields an immediate 10% return. You can easily use that bonus as a statement credit to effectively discount the cost of your care.

Don’t Make These Mistakes

While cash back credit cards are powerful financial tools, they can quickly turn into liabilities if mismanaged. Avoiding common pitfalls is just as important as maximizing your rewards.

- Carrying a balance month to month: This is the cardinal sin of rewards credit cards. If you pay 22% or 24% in annual interest, earning 2% cash back is a mathematically losing battle. You must pay your statement balance in full every single month to truly benefit from these programs.

- Paying for perks you no longer use: That premium airline card you kept from your working years might charge a $95 or $250 annual fee. If you no longer use the free checked bags or airport lounge access, you are throwing money away. Audit your wallet annually to ensure your cards still serve your current lifestyle.

- Closing old accounts haphazardly: When you realize a card no longer fits your needs, your first instinct might be to cancel it. Closing an old credit card can negatively impact your credit score by reducing your total available credit and shortening your average account history. Instead, call the issuer and ask to downgrade the account to a no-annual-fee cash back card.

- Ignoring the security benefits: Some retirees prefer using debit cards out of a fear of debt. However, credit cards offer superior zero-liability fraud protection. If a thief steals your debit card, the cash is missing from your checking account while the bank investigates. If a credit card is compromised, the issuer’s money is tied up, not yours.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” — Robert Kiyosaki

Using Rewards to Strengthen Your Retirement Budgeting

Generating cash back is only the first half of the equation; how you deploy those funds dictates their true impact on your senior finances. The most straightforward method is applying your cash back directly as a statement credit. This immediately reduces the amount of cash you need to pull from your checking account or retirement distributions to cover your monthly bills.

Alternatively, you can route your cash back into a separate, high-yield savings account. Watching these small rebates accumulate into a substantial emergency fund or a dedicated vacation account provides a fantastic psychological boost. Over a few years, a disciplined couple can easily save enough cash back to fund a significant home improvement project or a domestic getaway.

You can even mentally allocate your cash back to offset specific fixed costs. For example, if you generate $35 a month in credit card rewards, you can view that as completely neutralizing a portion of your monthly Medicare Part B premium. For extensive guidance on managing daily expenses and protecting your assets on a fixed income, the Consumer Financial Protection Bureau (CFPB) offers excellent, unbiased resources tailored specifically for older adults.

When Professional Advice Is Worth It

While optimizing credit card rewards is an excellent strategy for independent, financially stable retirees, credit can sometimes become overwhelming. If you find yourself relying on credit cards to pay for basic necessities because your Social Security and pension checks fall short, cash back rewards will not solve the underlying issue. Carrying high-interest debt on a fixed income rapidly depletes your hard-earned savings.

If your minimum payments are consuming a frightening percentage of your monthly budget, it is time to seek professional guidance. You do not have to navigate debt alone. Non-profit credit counseling agencies can help you negotiate lower interest rates and consolidate payments. Organizations like AARP provide tools to help you evaluate your spending, while government resources at USA.gov can connect you with legitimate financial assistance programs designed to ease the burden of housing, utilities, and medical costs.

Frequently Asked Questions About Retiree Credit Cards

Do credit card rewards count as taxable income?

In almost all cases, no. The IRS generally views cash back earned from everyday spending as a rebate or a discount on the purchase price, rather than taxable income. Because it is not taxable, it will not affect your Medicare Income-Related Monthly Adjustment Amount (IRMAA) or the taxation of your Social Security benefits. The only exception is if a bank gives you a cash bonus merely for opening an account without requiring any spending; in that rare case, they may send you a 1099-INT form.

Should I put my Medicare premiums on a credit card to earn rewards?

If you pay your Medicare premiums directly to the government (rather than having them deducted from your Social Security check), you can technically use a credit card. However, Medicare via the U.S. Treasury portal charges a convenience fee for credit card transactions. This fee usually outweighs the 1.5% or 2% cash back you would earn, making it a poor strategy. Stick to using your cards for groceries, gas, and retail purchases where no extra fees apply.

Is it safe to link my credit cards to mobile wallets on my smartphone?

Yes; in fact, it is often safer than carrying the physical card. Mobile wallets like Apple Pay and Google Pay use a process called tokenization. When you tap your phone at a store register, the merchant never sees your actual credit card number. Instead, they receive a unique, single-use code to process the transaction. This makes it incredibly difficult for hackers to steal your card information from retail databases.

Can I be denied a credit card simply because I am retired?

No. The Equal Credit Opportunity Act strictly prohibits lenders from discriminating against applicants based on age or because they receive public assistance income, including Social Security. As long as you have a strong credit history and sufficient verifiable income from your retirement resources to meet the issuer’s debt-to-income requirements, your employment status will not prevent you from being approved.

Next Steps for Your Wallet

Taking control of your senior finances does not require complex spreadsheets or stressful sacrifices. It begins with a simple audit of the plastic already sitting in your wallet. Lay out your current credit cards and review your last three months of statements. Identify where you spend the most money—whether that is the local grocery store, the pharmacy, or the gas pump—and check if your current cards actually reward those specific habits. If you are paying an annual fee for a travel card you haven’t used since 2023, pick up the phone today and ask to downgrade it to a no-fee cash back alternative.

By strategically aligning your credit cards with your daily retirement lifestyle, you empower your fixed income to stretch further. Every dollar you claw back from the banks through smart, responsible cash back strategies is another dollar you keep for your own peace of mind, your family, and your future.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.