Trading your snow shovel for a beach chair is the quintessential American retirement dream, but the reality of coastal living often carries a hidden price tag that can devastate a fixed income. Before you finalize your senior relocation to the shoreline, you must account for the specialized expenses unique to oceanside properties. Beyond the obvious premium on real estate, retiring near the ocean exposes your budget to aggressive salt-air corrosion, mandatory windstorm insurance, and specialized maintenance requirements that inland residents never face. Understanding these specific beach retirement costs empowers you to structure your retirement planning accurately, ensuring your coastal sanctuary remains a source of joy rather than an overwhelming financial burden.

1. The Shocking Reality of Coastal Insurance Premiums

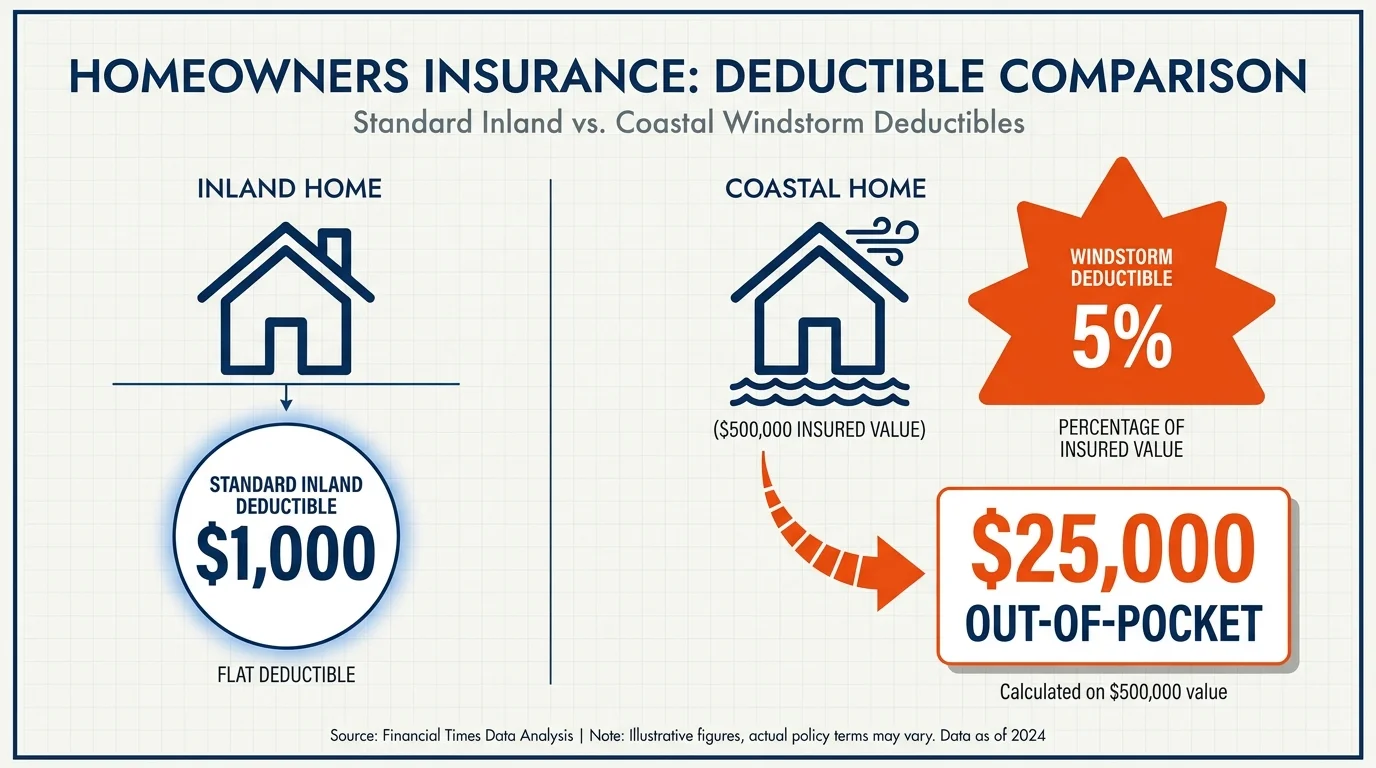

When you purchase a home inland, a standard homeowners insurance policy covers most common perils. On the coast, securing adequate coverage requires a patchwork of specialized, high-cost policies. Standard homeowners insurance explicitly excludes damage from rising water, meaning you must purchase a separate policy through the National Flood Insurance Program (NFIP) or a private carrier. Furthermore, most coastal homeowners policies include a separate wind and hail deductible.

Unlike standard deductibles that require a flat fee of $1,000 or $2,000, windstorm deductibles are typically calculated as a percentage of your home’s total insured value. If you insure a coastal home for $500,000 with a 5% wind deductible, you are responsible for the first $25,000 of damage out of pocket before the insurance company pays a dime. When planning your fixed-income budget, you must factor in these layered premiums, which easily run three to four times higher than inland insurance costs.

2. Salt Air Corrosion Eats Everything

The ocean breeze feels wonderful on a warm evening, but the microscopic salt particles carried in that breeze relentlessly attack metal, wood, and exterior paint. Accelerated wear and tear is one of the most pervasive, yet underestimated, beach retirement costs. Items that last a decade or more in the suburbs require constant replacement near the ocean.

Your outdoor air conditioning condenser unit is the most vulnerable target. Inland, an HVAC unit might last 12 to 15 years. On the oceanfront, the salt air destroys the aluminum fins and copper coils, often forcing a complete replacement every five to seven years. Coastal residents must purchase specially coated units at a premium, and even then, the lifespan is drastically reduced. This aggressive corrosion extends to your vehicle’s undercarriage, exterior light fixtures, patio furniture, and window hardware. You will spend significantly more on preventative maintenance, specialized exterior paint, and stainless-steel replacements.

3. Special Assessments and HOA Mega-Bills

Many retirees opt for coastal condominiums to avoid exterior maintenance, but this convenience introduces a different financial risk: the special assessment. Saltwater environments accelerate the degradation of concrete balconies, seawalls, roofing, and community amenities. When a condo association’s reserve fund falls short of the amount needed for major structural repairs, the board levies a special assessment against all unit owners.

Recent structural safety laws in prominent coastal states mandate strict reserve funding and mandatory inspections for older buildings. If you buy into an older building with underfunded reserves, you could face sudden assessments ranging from $10,000 to over $50,000. Before purchasing, you must scrutinize the homeowners association (HOA) financials and reserve studies to ensure you are not buying into a deferred maintenance nightmare.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

4. The “Tourist Town” Tax on Everyday Goods

Retiring near the ocean usually means relocating to a community built around tourism. Barrier islands and coastal enclaves face logistical challenges when transporting goods, and local merchants capitalize on a transient tourist population willing to spend freely. As a full-time resident, you end up paying the “tourist tax” on everyday necessities.

Groceries, gasoline, hardware supplies, and dining out consistently cost more in beach towns. While vacationers might shrug off a 20% premium on a cart of groceries for a one-week stay, absorbing those inflated prices 52 weeks a year severely impacts a retirement budget. Over time, many coastal retirees find themselves driving 30 to 45 minutes inland just to visit a big-box store or discount supermarket to keep their living expenses manageable.

5. Evacuation and Emergency Preparedness Budgets

Coastal living requires accepting the inevitable reality of severe weather. Preparing for and fleeing from tropical storms or hurricanes is an annual budget line item that inland residents rarely consider. True emergency preparedness involves significant upfront capital and ongoing seasonal costs.

Upfront costs often include installing impact-resistant windows, purchasing custom-fit storm shutters, and investing in a whole-home standby generator. Seasonal costs include the physical act of evacuating. When a mandatory evacuation order is issued, you must secure lodging inland, pay a premium for fuel, and cover dining out for several days. A single evacuation can cost an evacuating couple between $500 and $1,500. If you have mobility issues or complex medical needs, arranging safe transport and accommodating lodging adds even more to that figure.

6. Healthcare Scarcity and Travel Expenses

Many picturesque beach towns have small populations during the off-season, which means they lack the infrastructure to support large medical centers or specialized healthcare providers. While you will likely find adequate primary care, accessing a top-tier cardiologist, oncologist, or orthopedic surgeon often requires significant travel.

As you age, healthcare becomes the most critical component of your quality of life. If you require ongoing specialist care, you must budget for the travel time, gas, and potential overnight stays in the nearest major metropolitan area. Furthermore, you must verify how your Medicare coverage travels with you. To understand network restrictions and estimate potential out-of-pocket costs, you should regularly consult the Medicare Plan Finder. Relocating to a new zip code triggers a Special Enrollment Period, making it the perfect time to ensure your coverage aligns with the local healthcare landscape.

7. The Unexpected Cost of Hosting the Family

When you live where everyone else vacations, your home naturally becomes the preferred destination for holidays, summer breaks, and long weekends. While hosting adult children and grandchildren is a joyous part of retirement, the financial impact of the “summer guest subsidy” adds up rapidly.

During the peak visitation months, your utility bills will spike as the air conditioning works overtime and water usage doubles. You will find yourself buying more groceries, paying for meals out, and covering the entrance fees to local attractions, boat rentals, or beach activities. Many retirees actively embrace this role, but you must build a specific “hospitality” buffer into your annual cash flow to accommodate the steady stream of visitors without draining your core savings.

8. Mold, Mildew, and Relentless Pest Control

The high humidity that characterizes coastal environments creates the perfect breeding ground for mold, mildew, and aggressive pests. Managing the interior climate of a beach house is a continuous, year-round expense. You will likely run dehumidifiers constantly, increasing your electrical costs, to prevent mold from taking hold in your closets and HVAC ductwork.

Pest control requires an aggressive strategy. Coastal areas are notorious for subterranean and Formosan termites, which can decimate a home’s structural integrity if left unchecked. You must maintain active termite bonds, schedule quarterly exterminator visits to handle palmetto bugs and ants, and potentially invest in specialized pest exclusions for your crawl spaces and attics.

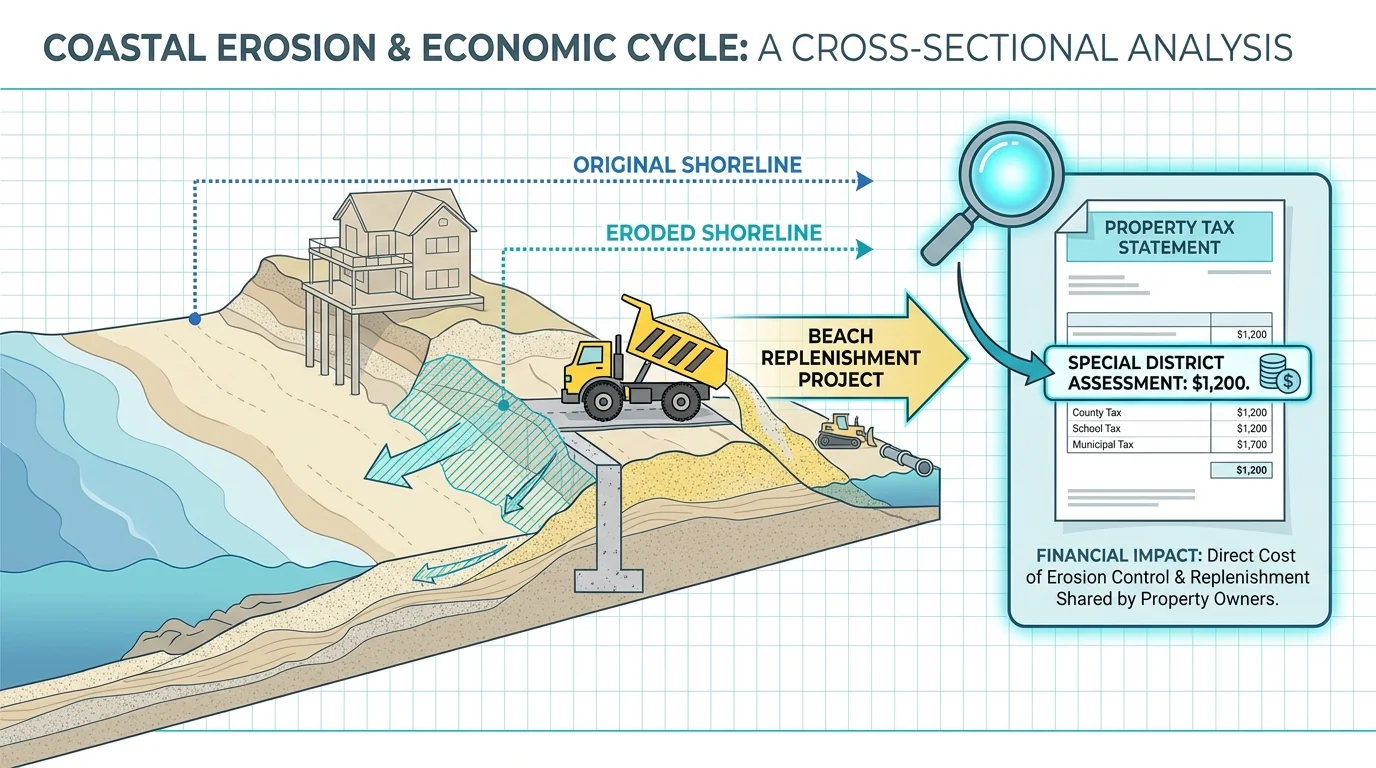

9. Beach Replenishment and Coastal Erosion Taxes

The ocean is a dynamic force, and beaches naturally erode over time. To protect oceanfront property and maintain the wide, sandy beaches that attract tourists, local municipalities frequently undertake massive beach renourishment and dredging projects. These engineering feats cost millions of dollars.

Local governments fund these projects by levying special municipal taxes, establishing special taxing districts, or significantly raising property taxes for residents. Even if your home is situated several blocks away from the actual sand, you are often included in the tax district responsible for funding the coastal management. When calculating your long-term housing costs, you must assume property taxes will rise aggressively to combat rising sea levels and natural erosion.

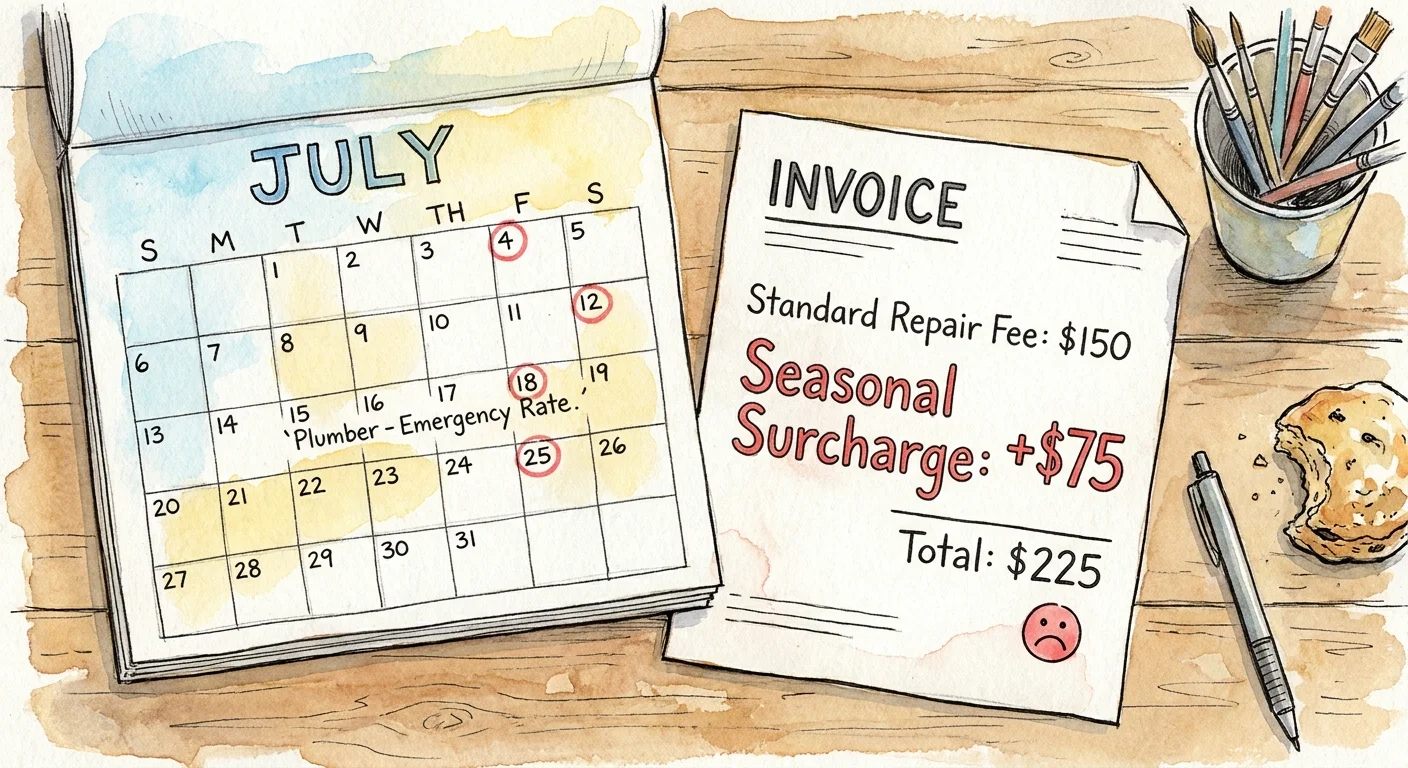

10. Peak-Season Vendor Premiums

Maintaining a home requires plumbers, electricians, landscapers, and general contractors. In coastal towns, the local economy is dominated by the short-term rental market. During peak tourist season, property management companies keep local tradespeople incredibly busy fixing emergency issues at lucrative rental properties.

Getting a contractor to show up at a residential home for routine maintenance during the summer often requires paying top dollar. Vendors charge a premium simply because their time is in such high demand. You will either pay inflated rates for basic home services or wait weeks for repairs that would be handled immediately in a traditional suburban neighborhood.

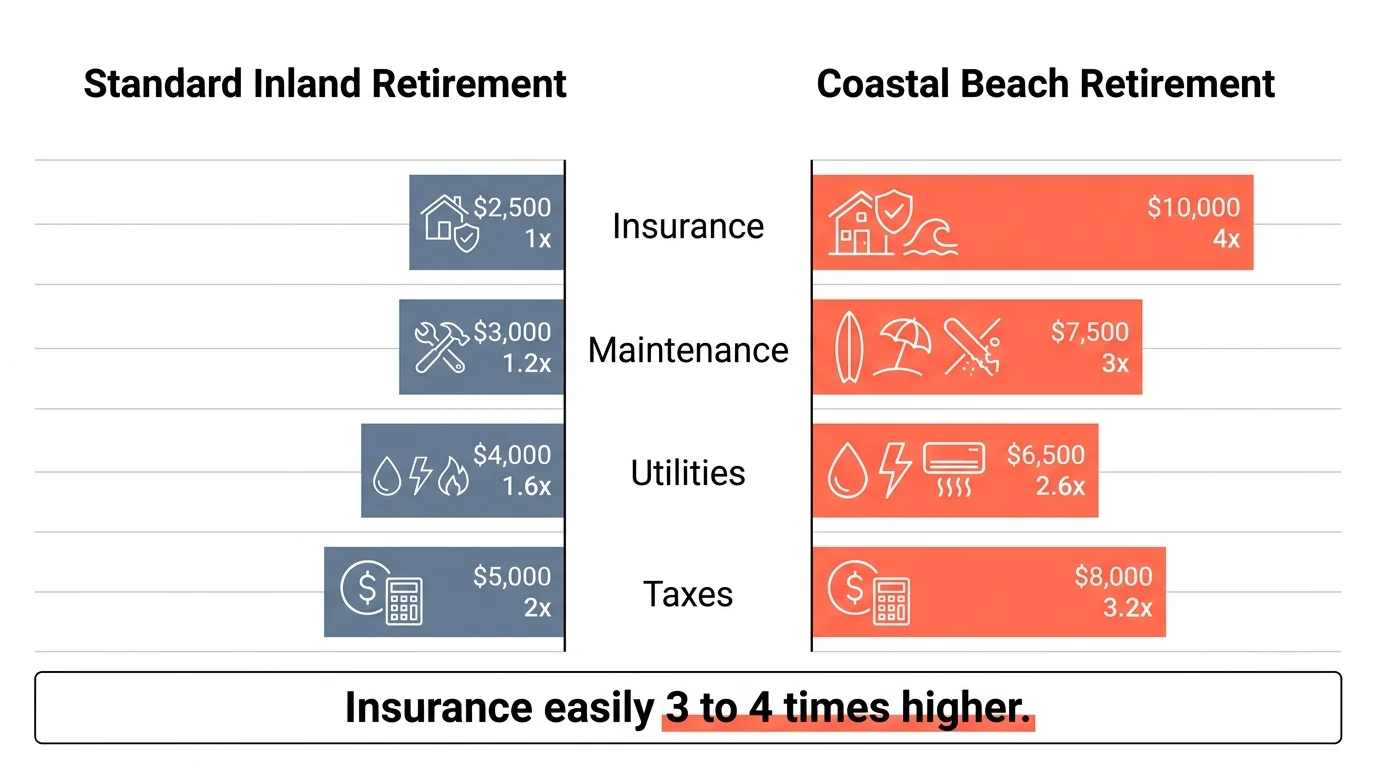

Comparing the Financial Realities

To put these expenses into perspective, reviewing a direct comparison of typical maintenance and carrying costs clarifies the financial commitment required for oceanside living.

| Expense Category | Typical Inland Cost (Annualized) | Coastal Cost (Annualized) | The Coastal Reason |

|---|---|---|---|

| HVAC Replacement | $400 – $500 | $1,100 – $1,500 | Salt air corrosion drastically reduces unit lifespan; requires specialty coatings. |

| Property Insurance | $1,200 – $2,500 | $4,000 – $12,000+ | Requires separate wind/hail policies, high deductibles, and NFIP flood insurance. |

| Pest & Moisture Control | $300 – $500 | $800 – $1,200 | High humidity requires continuous dehumidification; aggressive termite mitigation. |

| Exterior Maintenance | $500 – $800 | $1,500 – $2,500 | Frequent window washing, power washing, and specialized exterior painting required. |

Errors That Cost Retirees Thousands

When planning a move to the coast, emotion often overrides financial logic. Avoid these common, expensive mistakes:

- Failing to Read the Elevation Certificate: Never buy a coastal property without reviewing its FEMA elevation certificate. Buying a home that sits below base flood elevation guarantees exorbitant flood insurance premiums that can render the home unaffordable on a fixed income.

- Ignoring Medicare Network Restrictions: Moving across state lines—or even just to a new county—can completely upend your Medicare Advantage or Part D coverage. Retirees often assume their current plan travels seamlessly, resulting in massive out-of-network bills. Always verify coverage networks before finalizing a move.

- Underestimating HOA Reserve Health: Buying into a condo complex with low monthly dues feels like a win until a $30,000 roof assessment hits. If the reserve study is outdated or underfunded, walk away.

When to Get Expert Help

Navigating the financial complexities of a coastal retirement is not a do-it-yourself project. Before committing to a major senior relocation, assemble a team of professionals to verify your numbers. Consult a fee-only financial advisor to stress-test your retirement income against worst-case insurance and assessment scenarios. You can find excellent guidelines on choosing advisors and managing late-life finances through the Consumer Financial Protection Bureau (CFPB).

Additionally, speak with a local, independent insurance broker in your target zip code. Do not rely on national averages. Have the broker pull actual quotes for wind, flood, and hazard insurance on specific properties you are considering. Finally, utilize free resources provided by AARP to research the cost of living and healthcare quality ratings in your desired beach town.

Frequently Asked Questions

Does standard homeowners insurance cover hurricane damage?

Rarely. In coastal areas, standard policies almost always exclude flood damage (rising water/storm surge), and many also exclude wind and hail damage. You typically need three separate policies or riders to fully protect your home: standard hazard, wind/hail, and flood.

Will my Medicare Advantage plan work if I move to a beach town in another state?

Usually, no. Medicare Advantage plans operate on localized county or regional networks. If you move out of your plan’s service area, you must enroll in a new plan available in your new zip code. You will be granted a Special Enrollment Period to make this switch without penalty.

How much extra should I budget for home maintenance near the ocean?

A safe rule of thumb is to double your standard home maintenance budget. If you currently set aside 1% of your home’s value annually for upkeep inland, plan to set aside at least 2% to 2.5% for an oceanside property to cover accelerated wear, tear, and corrosion.

Do not let the hidden expenses of coastal living shatter your vision of a perfect retirement. By accounting for elevated insurance premiums, aggressive maintenance requirements, and localized inflation, you can build a resilient financial plan that protects your lifestyle. Take an afternoon this week to pull sample insurance quotes for your target zip code and run a realistic budget. Being proactive today guarantees your time at the beach will be spent enjoying the sunset, rather than worrying about the bills.

Retirement rules and benefit amounts vary based on individual work history, income, and circumstances. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.