A happy couple enjoys a healthy breakfast outdoors with easy access to Florida’s modern medical facilities.

A happy couple enjoys a healthy breakfast outdoors with easy access to Florida’s modern medical facilities.

Trading your snow shovel for a golf club or a morning walking trail is a classic milestone, but the drive to relocate goes far beyond a simple desire for a sunny retirement USA experience. High winter heating bills, the joint-aching reality of sub-zero temperatures, and the physical risk of icy sidewalks push thousands of older adults to evaluate the best warm states to retire each year.

When you move in your sixties or seventies, you are not just buying a new house; you are investing in a new healthcare network, a different tax environment, and a climate that actively supports your physical mobility. The physical benefits of year-round sunshine are well documented—from higher vitamin D absorption to the sheer ease of maintaining a daily walking habit without worrying about frostbite. Yet the financial implications of crossing state lines require careful calculation.

“The goal of retirement is to live off your assets—not live off your regrets.” — Anonymous

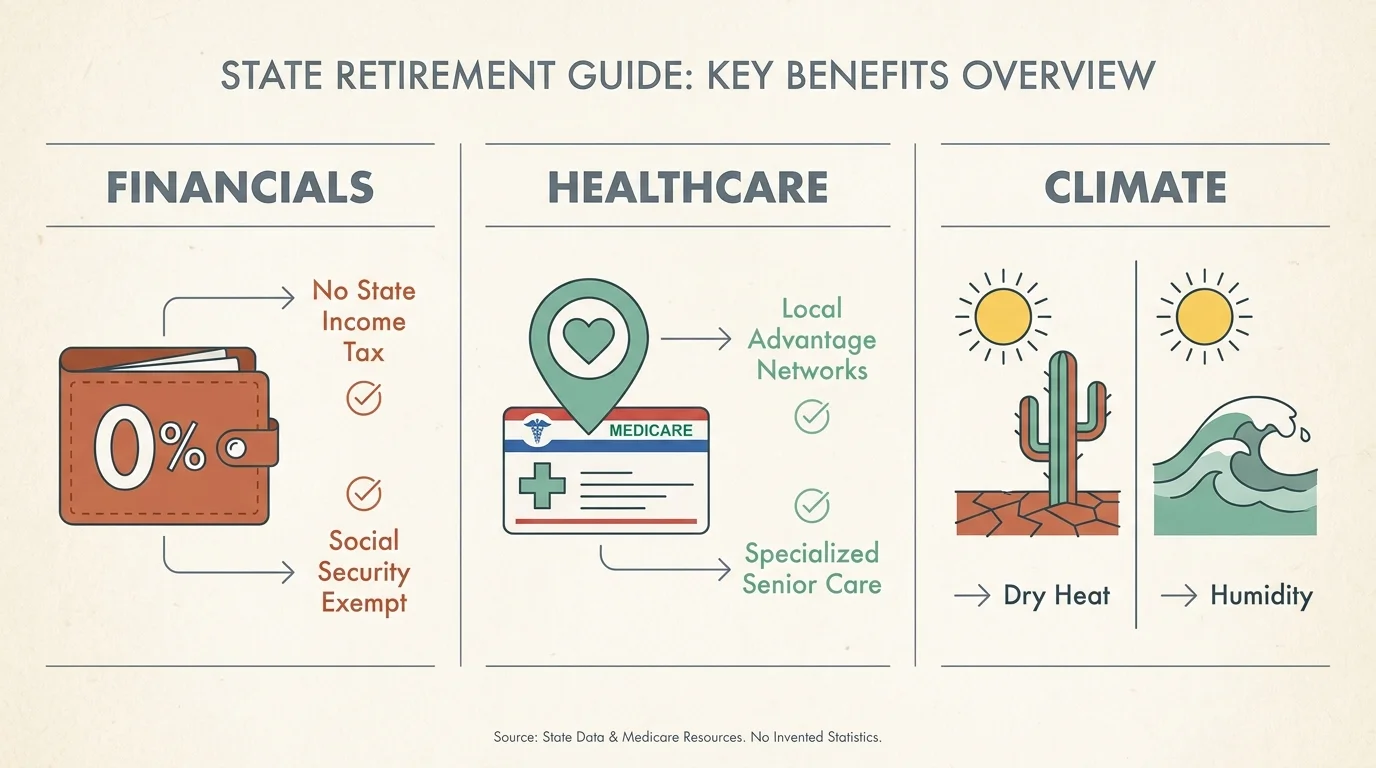

Relocating across the country is a massive logistical and financial undertaking. To help you evaluate your options, we evaluated states based on their tax friendliness toward fixed incomes, access to quality medical care, cost of living, and climate benefits.

The Bottom Line Up Front

- Taxes matter as much as sunshine: Moving to a state with zero income tax or generous retirement income exemptions can save you thousands annually.

- Your Medicare footprint will change: Relocating permanently means you will likely need to select a new Medicare Advantage or Part D plan, as networks are highly localized.

- Dry heat versus humidity: Both offer warmth, but states like Arizona offer a dry climate that many arthritis sufferers prefer, while coastal states like Florida provide ocean breezes at the cost of high summer humidity.

1. Florida: The Traditional Heavyweight

Florida remains the undisputed giant of retirement relocation, and its appeal rests heavily on two massive pillars: year-round warmth and an incredibly favorable tax structure. Florida levies no state income tax, meaning your Social Security benefits, pension payouts, and 401(k) withdrawals remain entirely untouched by state revenue collectors.

Because the state hosts such a massive population of older adults, the healthcare infrastructure is highly specialized. From the Mayo Clinic in Jacksonville to specialized orthopedic and cardiac centers in Tampa and Naples, you will find physicians who focus almost entirely on the needs of aging bodies. The state also offers a robust array of Medicare Advantage plans, often featuring high-value extra benefits due to the intense competition among insurance carriers in the state.

However, the financial picture is not perfect. While you save heavily on income taxes, you must budget aggressively for property insurance. Homeowners insurance premiums in Florida have surged due to hurricane risks, and you will need to factor this recurring cost into your monthly housing budget.

2. Arizona: The Dry Heat Haven

If you suffer from osteoarthritis or other joint conditions, the desert Southwest frequently serves as the premier health retirement location. The dramatic lack of humidity in Arizona provides immense relief to those whose joints ache when damp, cold fronts move through. Cities like Tucson, Prescott, and the greater Phoenix area boast 300 days of sunshine a year, making daily outdoor exercise virtually guaranteed.

Financially, Arizona is highly accommodating. The state does not tax Social Security benefits, and property taxes remain relatively low compared to the national average. While Arizona does have a state income tax, it moved to a low flat tax rate of 2.5%, keeping your retirement withdrawals largely protected.

The healthcare system in Arizona is anchored by top-tier facilities like the Mayo Clinic in Scottsdale and Banner Health. Active adult communities are practically an Arizona invention, offering an instant social network for newcomers who want to retire warm weather style while maintaining an intensely active lifestyle.

3. Texas: Big Spaces and Zero Income Tax

Texas draws retirees who want a lower cost of living combined with plenty of space and a famously independent culture. Like Florida, Texas boasts zero state income tax. This makes it an incredibly powerful wealth-preservation tool if you are drawing down substantial balances from traditional IRAs or a corporate pension.

The climate varies dramatically across the state’s massive footprint. The Texas Hill Country—surrounding Austin and San Antonio—is widely considered the best climate seniors can find in the state, offering mild winters, beautiful rolling landscapes, and less humidity than the Gulf Coast. Healthcare in Texas is world-class, particularly if you settle within driving distance of Houston’s renowned medical center or the specialized hubs in Dallas.

You must balance the income tax savings against the state’s property tax rates, which are among the highest in the country. To offset this, Texas offers generous property tax homestead exemptions for residents aged 65 and older, effectively freezing the school tax portion of your property tax bill once you qualify.

4. South Carolina: Coastal Charm on a Budget

For retirees who want the Atlantic coastal experience without the soaring costs and intense summer heat of South Florida, South Carolina offers a compelling middle ground. Cities like Charleston, Beaufort, and Greenville offer immense historical charm, thriving culinary scenes, and excellent walkability.

South Carolina is incredibly friendly to retirement wallets. The state does not tax Social Security benefits. Furthermore, residents over the age of 65 can claim a generous $15,000 income tax deduction, which applies to all forms of retirement income. Property taxes are remarkably low, making housing significantly more affordable than in many Northern states.

While the winters are mild and brief, you will experience four distinct seasons, which appeals to retirees who still want to see leaves change in the autumn but refuse to shovel snow in January. Healthcare networks are expanding rapidly, particularly around the Greenville-Spartanburg area and Charleston’s Medical University of South Carolina.

5. Nevada: The Desert Alternative

Nevada extends far beyond the bright lights of the Las Vegas Strip. Communities like Henderson and Reno are rapidly becoming hotspots for retirees seeking a tax-friendly, sun-drenched environment. Nevada joins the ranks of states with absolutely no state income tax, allowing you to maximize every dollar of your savings.

The climate mirrors the benefits of Arizona, offering the dry heat that eases joint pain and respiratory issues. Henderson routinely ranks as one of the safest cities in America and features master-planned communities designed specifically for active adults, complete with miles of paved walking trails and state-of-the-art recreation centers.

Healthcare access has improved dramatically over the last decade to support the influx of older residents, though those with highly specialized or rare medical conditions often maintain secondary care networks in neighboring California.

6. Georgia: The Hidden Tax Haven

Georgia quietly offers one of the most lucrative tax environments for retirees in the entire country. Once you turn 65, the state grants a massive retirement income exclusion of up to $65,000 per person (or $130,000 for a married couple filing jointly). This exclusion covers pensions, 401(k) distributions, and passive income, meaning the vast majority of middle-class retirees will pay zero state income tax in Georgia.

The climate provides mild, short winters and long, warm summers. Coastal areas like Savannah and St. Simons Island offer beautiful oceanfront living, while northern Georgia provides stunning mountain views and slightly cooler temperatures.

Atlanta boasts world-class healthcare facilities, including Emory University Hospital, providing peace of mind for managing complex health conditions. Cost of living across most of Georgia remains well below the national average, making your retirement dollars stretch remarkably far.

7. New Mexico: High Altitude and Deep Culture

Dubbed the Land of Enchantment, New Mexico offers a culturally rich, visually stunning environment for those who want a quiet, artistic retirement. The state provides an ideal climate featuring more than 300 days of sunshine, low humidity, and cool evenings due to the high elevation.

Housing in cities like Albuquerque, Santa Fe, and Las Cruces is more affordable than in comparable Western states like Colorado or Arizona. While New Mexico does tax Social Security, recent legislation has exempted these benefits for single filers earning under $100,000 and joint filers earning under $150,000, effectively shielding most retirees.

Healthcare in New Mexico is solid in the major metro areas, though residents moving to more rural, artistic enclaves like Taos should be prepared to drive for specialized medical care.

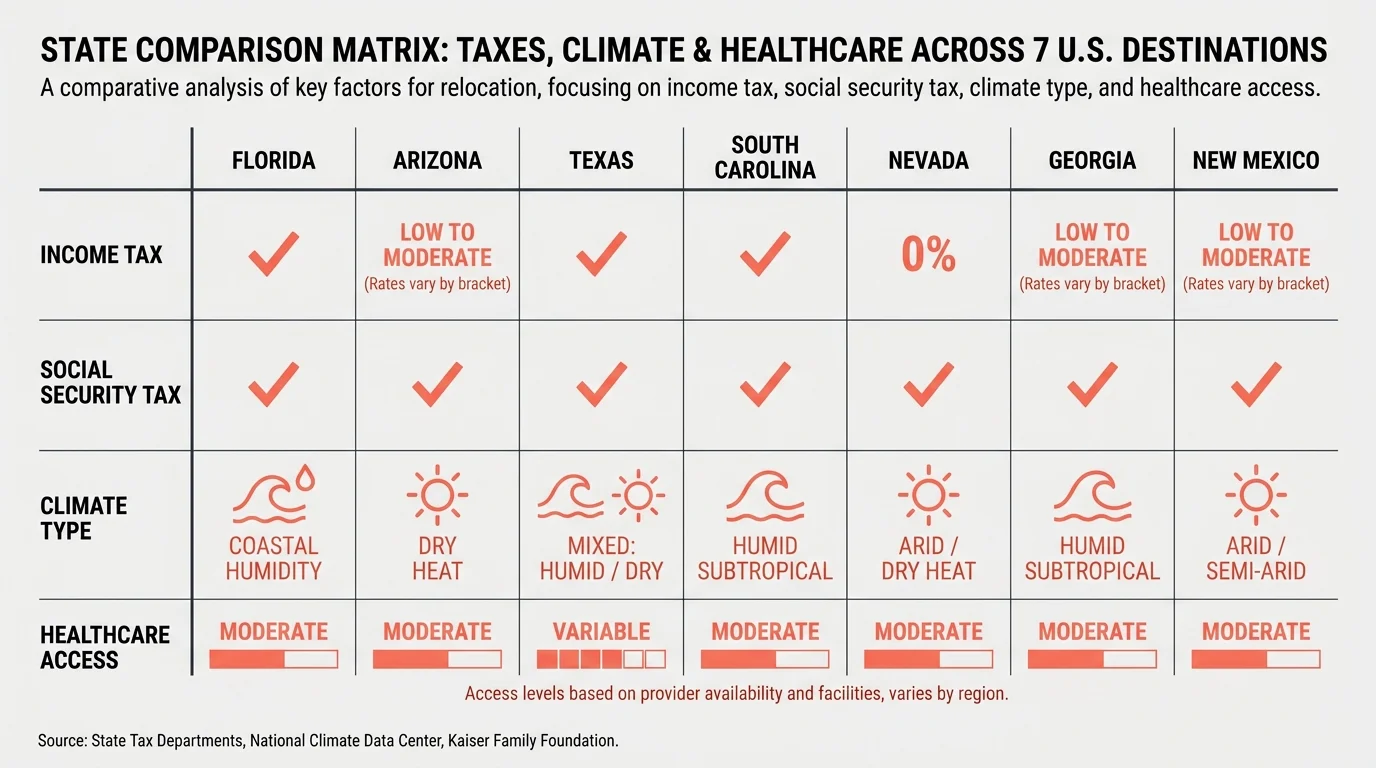

Comparing the 7 Warm States

To help you visualize your options, review this side-by-side comparison of the financial and climate factors that will directly impact your quality of life.

| State | State Income Tax Status | Social Security Taxed? | Primary Climate Benefit |

|---|---|---|---|

| Florida | No State Income Tax | No | Tropical warmth, ocean breezes |

| Arizona | Low Flat Tax (2.5%) | No | Dry desert heat, excellent for joints |

| Texas | No State Income Tax | No | Varied; dry in west, humid on coast |

| South Carolina | Up to $15k deduction (65+) | No | Mild winters, distinct but warm seasons |

| Nevada | No State Income Tax | No | Dry heat, massive sunshine hours |

| Georgia | Up to $65k deduction (65+) | No | Mild winters, lush greenery |

| New Mexico | Progressive (with income limits) | Exempt for most | High altitude, low humidity, cool nights |

Don’t Make These Mistakes

The excitement of moving to a sunny paradise can easily cloud your financial judgment. Protect yourself by avoiding these common relocation traps.

Failing to rent first: You should never buy a home in a new state without living there for at least six months. Renting allows you to experience the intense heat of a Florida August or an Arizona July before committing. It also lets you test the local traffic, the neighborhood vibe, and the proximity to grocery stores and pharmacies.

Ignoring your Medicare network: Medicare Advantage (Part C) and Medicare Prescription Drug (Part D) plans are region-specific. If you move out of your plan’s service area, you are granted a Special Enrollment Period to choose a new plan. Do not assume your favorite doctors in your new state will accept your current coverage. Always run your medications and prospective new ZIP code through the Medicare Plan Finder to ensure you will have affordable coverage upon arrival.

Underestimating extreme weather costs: Warm weather often comes with environmental trade-offs. You must factor the cost of hurricane insurance in coastal states, or massive summer air conditioning bills in the desert, into your monthly budget. A state with low taxes might quickly become expensive if your homeowner’s premium triples.

Leaving your support system blindly: Health in retirement is not just about physical medicine; it is deeply tied to social connection. Moving 1,000 miles away from your children, grandchildren, and lifelong friends can trigger intense isolation. Ensure your chosen destination has an active, welcoming community infrastructure or easy airport access so family can visit frequently. If you need local support resources in a new state, the federal government’s Eldercare Locator is an excellent tool for finding community services.

When Professional Advice Is Worth It

Changing your state of residence involves complex legal and financial maneuvers. You are not just packing boxes; you are changing your legal domicile.

If you have substantial assets, consult a financial advisor or a CPA before making the move. Establishing a new domicile requires specific steps—like changing your driver’s license, registering your vehicles, and updating your voter registration—to prove to your former, higher-tax state that you have truly left. High-tax states like New York and California are known for auditing retirees who claim to have moved but maintain a secondary home in their original state.

Furthermore, an elder law attorney in your new state should review your estate planning documents. Powers of attorney, healthcare directives, and living wills are governed by state law. A document drafted in Illinois may not be immediately recognized or easily executed by a hospital in Texas.

Frequently Asked Questions

Does moving to a warm climate actually help arthritis?

Many older adults report a significant reduction in joint pain and stiffness when moving to a warmer, drier climate. While the physical deterioration of the joint does not reverse, changes in barometric pressure and temperature heavily influence pain receptors. Dry climates like Arizona and Nevada are particularly favored because they lack the damp cold that frequently exacerbates osteoarthritis.

Do I have to notify Social Security if I move to a new state?

Yes. Even if your benefit is deposited directly into your bank account, you must update your address with the Social Security Administration. This ensures you receive vital correspondence, including your annual SSA-1099 tax form and updates regarding your Medicare Part B premiums.

Can I keep my current Medicare Supplement (Medigap) plan if I move?

Generally, yes. Unlike Medicare Advantage plans, standardized Medicare Supplement plans (Medigap) are accepted by any doctor nationwide who accepts Original Medicare. However, your premium may change based on your new ZIP code, and it is wise to compare rates once you settle in your new home.

Are there programs to help older adults afford a move?

While the federal government does not pay for moving expenses, there are numerous state and local programs designed to help older adults reduce their daily living costs, freeing up capital. You can search for energy assistance, property tax relief, and prescription savings programs in your prospective new state using the National Council on Aging’s BenefitsCheckUp tool.

Your Next Steps

Finding the right warm state for your retirement requires balancing your physical needs with your financial reality. Begin by narrowing your choices down to two or three states based on your tax situation and climate preference. Next, schedule extended visits to those areas during their worst weather months—visit Florida in August or Arizona in July—to ensure you can tolerate the climate year-round.

Once you verify that the local lifestyle aligns with your vision, analyze the housing market and investigate local healthcare networks. By taking a methodical, data-driven approach, you ensure your relocation provides both physical comfort and long-term financial security.

Retirement rules, tax brackets, and Medicare plan availability vary based on individual circumstances, location, and annual legislative changes. This article provides general guidance only. Consult a SHIP counselor, financial advisor, or elder law attorney for advice specific to your situation.

Last updated: February 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.