A peaceful watercolor scene illustrates the four key pillars of a comfortable and affordable retirement.

A peaceful watercolor scene illustrates the four key pillars of a comfortable and affordable retirement.

Fulfilling retirements do not require a six-figure income or a multimillion-dollar portfolio. You can build a rich, comfortable life on a retirement budget of $40,000 a year simply by choosing the right location. Geography plays a massive role in retiree finances, dictating everything from your property taxes to your healthcare costs.

Relocating to an affordable retirement town stretches your Social Security benefits significantly further, giving you more freedom to travel, pursue hobbies, or spoil your grandchildren. By prioritizing areas with low cost living, excellent healthcare access, and vibrant communities, you can enjoy your golden years without constant financial stress.

Explore these ten outstanding locations where your money works harder for you.

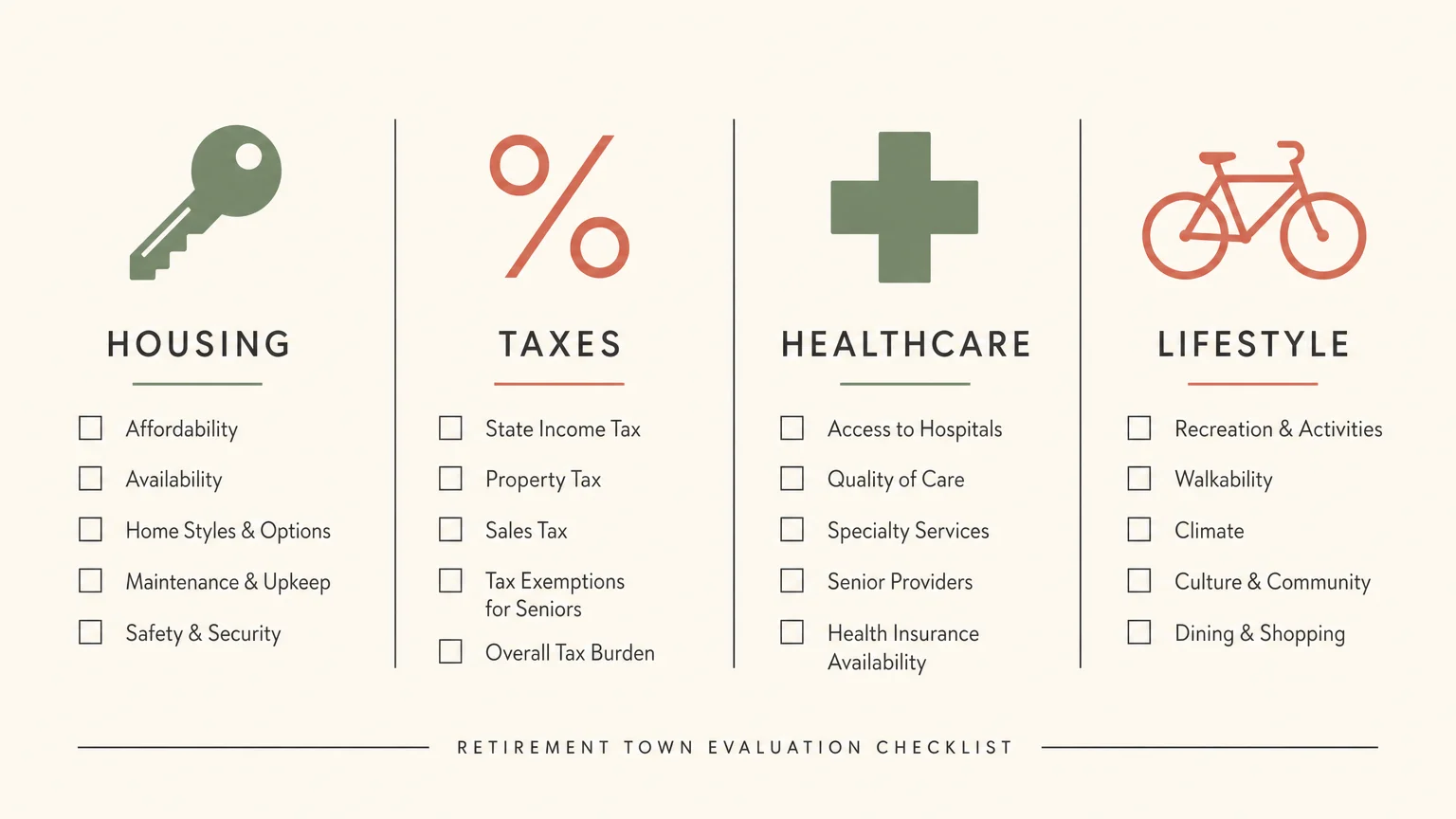

What You Need to Know

- Housing is the anchor: Keeping your housing costs (rent or mortgage, plus taxes and insurance) under $1,200 a month is the secret to thriving on a $40,000 annual income.

- Taxes matter as much as price: Several states exempt Social Security and pension income from state taxes, effectively giving you an instant raise.

- Healthcare access is non-negotiable: An affordable town is only viable if it features a robust local hospital system and plentiful Medicare providers.

- Lifestyle determines satisfaction: Low costs mean nothing if you are bored. The best towns offer free or inexpensive natural amenities, cultural events, and community centers.

How We Evaluated Affordable Retirement Towns

Living on $40,000 a year translates to a monthly income of roughly $3,333. To live comfortably on this amount without clipping coupons out of desperation, you need an environment designed for affordability.

When evaluating the best towns to retire, we looked well beyond basic median home prices. A truly great retirement destination balances financial practicality with a high quality of life.

First, we analyzed real estate markets where securing a comfortable home or apartment leaves plenty of room in your monthly budget. Next, we examined the state and local tax burdens. Property tax rates and the taxation of retirement income can quietly drain your savings if you are not careful. We prioritized states that treat retiree finances gently.

Finally, we evaluated healthcare infrastructure. As you age, proximity to quality medical care dictates your independence and peace of mind. Every town on this list features strong regional medical centers.

We also factored in the local lifestyle—because true low cost living includes access to parks, lakes, walking trails, and community organizations that keep you active without requiring a pricey country club membership.