Nearly 400,000 Americans cross state lines each year to start their retirement. If you are preparing to join them in 2026, the map of ideal destinations looks drastically different than it did just a decade ago. Surging property insurance premiums, shifting state tax laws, and changing climate patterns have fundamentally rewritten the playbook for where you can stretch your savings without sacrificing your quality of life.

Finding the right state to spend your golden years requires balancing two competing forces: your wallet and your wellbeing. Move purely for the lowest cost of living, and you might find yourself miles away from quality healthcare or stranded in a community with little social engagement. Relocate strictly for the perfect senior lifestyle, and you could drain your nest egg years ahead of schedule.

To help you navigate this massive life decision, we evaluated all 50 states based on affordability, tax burdens, healthcare access, and everyday livability. Whether you want to retire cheap in a quiet mountain town or seek a vibrant, sun-soaked community packed with amenities, this guide will help you identify the best states to retire in the USA right now.

The Bottom Line Up Front

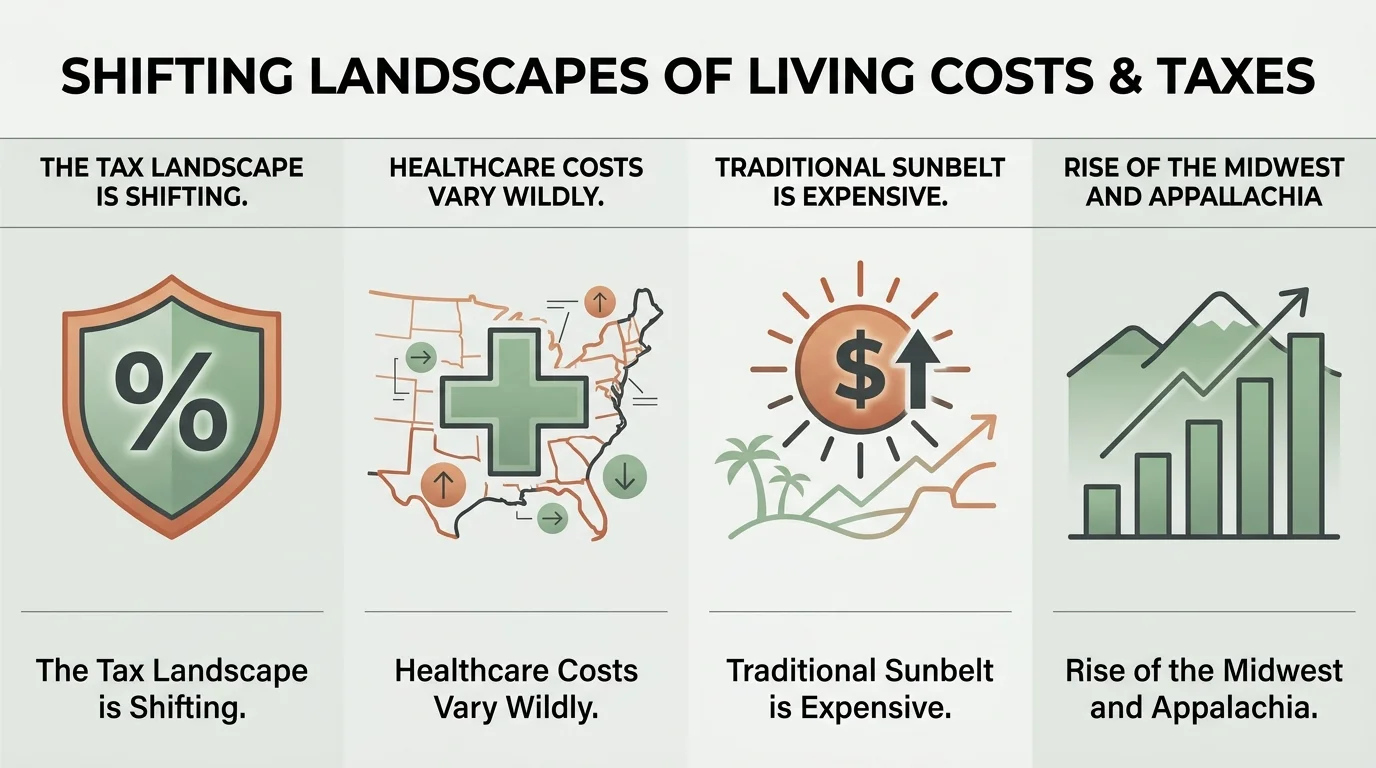

- The Tax Landscape is Shifting: More states now exempt Social Security benefits from state income taxes, but property taxes and local sales taxes often make up the difference. Always calculate the total tax burden.

- Healthcare Costs Vary Wildly: Moving to a new state often means changing your Medicare coverage, especially if you rely on regional Medicare Advantage networks.

- The Traditional Sunbelt is Expensive: Florida and Arizona remain incredibly popular for lifestyle, but skyrocketing homeowner’s insurance and housing costs have pushed them down the list for budget-conscious retirees.

- The Rise of the Midwest and Appalachia: States like South Dakota, Pennsylvania, and West Virginia are emerging as top contenders by combining excellent tax benefits with a low cost of living for seniors.

Why the “Best” State is Changing in 2026

Retirement relocation used to be a simple equation: sell the family home in a snowy northern state, buy a smaller condo in Florida or Arizona, and enjoy the sunshine. Today, that equation is far more complex.

Economic shifts over the past few years have forced retirees to look beyond the obvious choices. Persistently high interest rates have kept national housing inventory relatively tight, making the median home price a massive barrier in coastal communities. Furthermore, severe weather events have triggered historic spikes in property insurance premiums across the Southeast and Gulf Coast. A state with no income tax loses its financial appeal if you have to pay $6,000 a year just to insure your roof.

Quality healthcare access has also taken center stage. As the 65-and-older population grows, wait times for specialists in popular retirement hubs have lengthened. Savvy retirees now research hospital bed capacity and the local density of geriatric specialists before calling a moving company.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

Top 3 States to Retire Cheap (Cost-Conscious Picks)

If maximizing your retirement income is your top priority, you need states that offer a trifecta of savings: low property taxes, affordable housing, and generous exemptions on retirement income. These three states stretch your dollar the furthest.

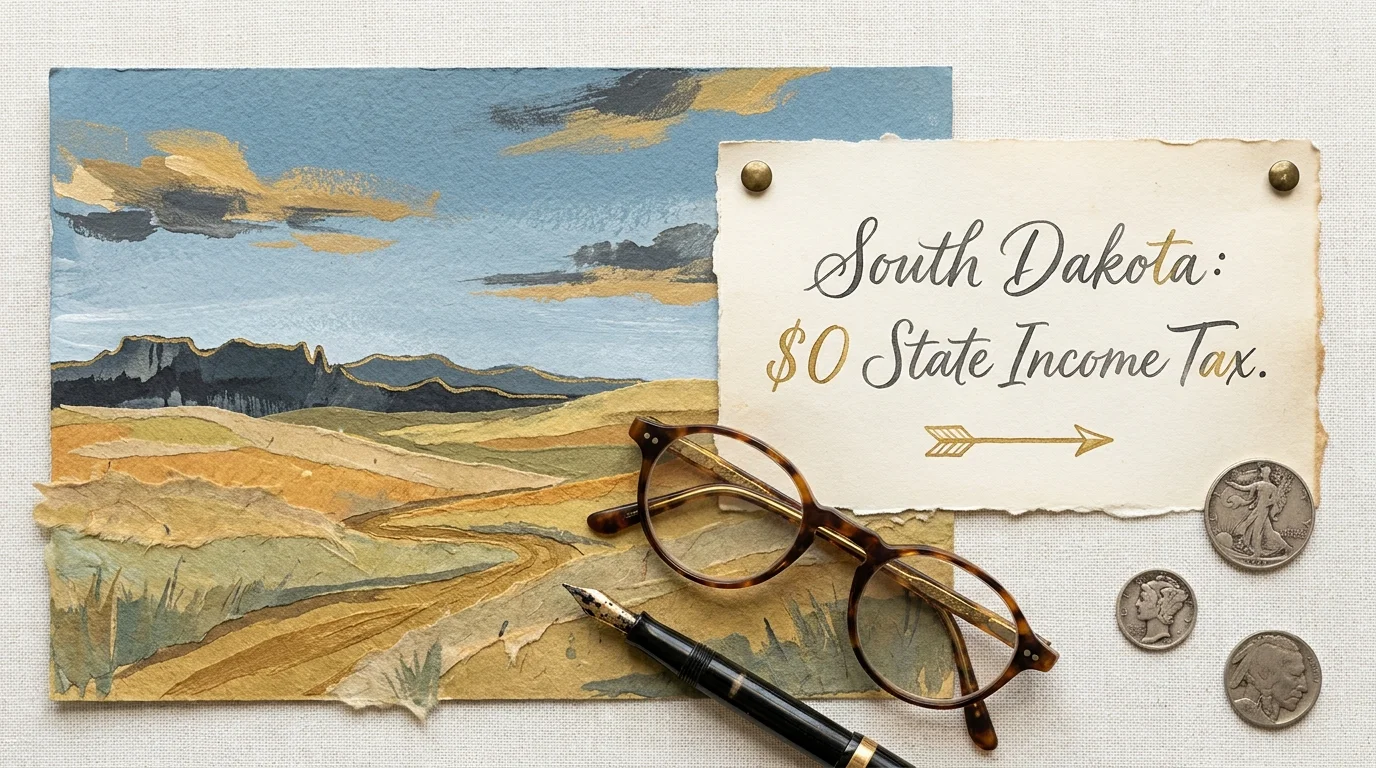

1. South Dakota

South Dakota consistently dominates lists for affordability, and 2026 is no exception. The Mount Rushmore State levies zero state income tax, meaning your Social Security, pensions, and withdrawals from traditional IRAs remain completely untouched by the state government.

Housing remains highly accessible, with median home prices sitting well below the national average. Beyond the balance sheet, cities like Sioux Falls and Rapid City offer robust regional healthcare networks and a surprising array of cultural amenities. If you can handle the harsh winters, the financial peace of mind is unmatched.

2. Wyoming

For those who prefer wide-open spaces over crowded subdivisions, Wyoming presents a compelling financial case. Like South Dakota, Wyoming has no state income tax. Furthermore, it boasts incredibly low property taxes, helping you keep your fixed expenses predictable year after year.

Wyoming is ideal for the rugged, independent retiree. The state offers unparalleled access to national parks and outdoor recreation. However, because the population is sparse, you must carefully evaluate your proximity to major medical centers. Living near Cheyenne or Casper provides the best balance of remote living and necessary infrastructure.

3. West Virginia

West Virginia is rapidly gaining attention as a haven for retirees fleeing high costs on the East Coast. The state offers some of the lowest median home prices in the country. In recent years, West Virginia has aggressively phased out state income taxes on Social Security benefits for most earners, making it much more competitive.

The Appalachian lifestyle offers beautiful mountain views, quiet communities, and a distinct lack of traffic congestion. Towns like Morgantown and Charleston provide access to excellent university-backed medical systems, giving you premium healthcare without the premium price tag.

Top 3 States for the Ultimate Senior Lifestyle

If you have a well-funded retirement and want to prioritize active living, community engagement, and world-class healthcare, these states offer unparalleled quality of life.

1. Pennsylvania

Pennsylvania might surprise you as a lifestyle pick, but it strikes a near-perfect balance for modern retirees. The state famously exempts all retirement income from state taxes—including Social Security, pensions, 401(k)s, and IRAs. This leaves you with more disposable income to enjoy your free time.

The state offers a diverse lifestyle menu. You can choose the rich cultural and historical environments of Philadelphia or Pittsburgh, the quiet farming communities of Lancaster County, or the mountain retreats in the Poconos. Most importantly, Pennsylvania is home to some of the nation’s premier healthcare systems, ensuring you have immediate access to top-tier specialists as you age.

2. Virginia

Virginia blends Southern charm with Mid-Atlantic sophistication. From the beaches of Virginia Beach to the Blue Ridge Mountains and the historic streets of Williamsburg, the state caters to almost every hobby and interest. The climate provides four distinct seasons without the extreme, lingering winters of New England.

Financially, Virginia is highly accommodating. It does not tax Social Security benefits, and it offers a substantial age-based tax deduction for residents 65 and older. The state also features top-rated hospitals, particularly in the northern regions and around Charlottesville.

3. Florida (With Caveats)

No list of retirement destinations is complete without Florida. It remains the undisputed champion for weather, beaches, and master-planned 55+ communities. The absence of state income tax continues to draw affluent retirees looking to shield their investment income.

However, relocating to Florida in 2026 requires caution. While the senior lifestyle is unmatched, the cost of living for seniors has surged in specific categories. Homeowner’s insurance and HOA fees have skyrocketed in many coastal communities. Florida is best suited for retirees who have substantial financial buffers and want a turnkey, highly social retirement experience.

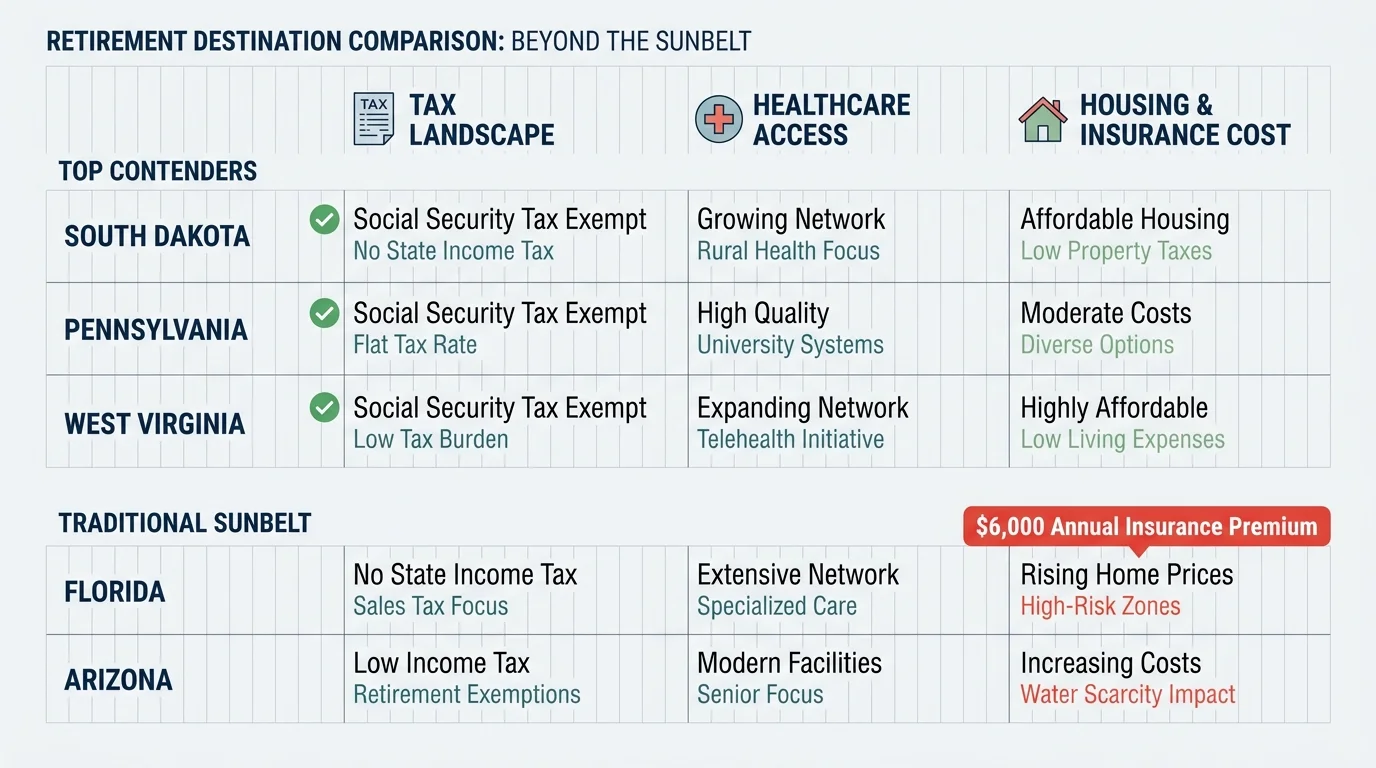

State-by-State Comparison: Cost & Care

Use this table to compare how our top picks stack up against one another in critical categories. Note that healthcare rankings represent statewide averages; care quality can fluctuate significantly by county.

| State | State Tax on Social Security? | Tax on IRA/401(k) Withdrawals? | Housing Affordability | Healthcare Quality Access |

|---|---|---|---|---|

| South Dakota | No | No | High | Moderate |

| Wyoming | No | No | High | Moderate to Low |

| West Virginia | No (for most) | Yes (partially exempt) | Very High | Moderate |

| Pennsylvania | No | No | Moderate | Very High |

| Virginia | No | Yes (with generous deductions) | Moderate to Low | High |

| Florida | No | No | Low (due to insurance/HOAs) | High |

Common Retirement Traps When Relocating

Uprooting your life is exciting, but it exposes you to several critical financial and emotional risks. Avoid these frequent missteps when choosing your new state.

The “Vacation vs. Living” Trap

Many retirees move to a location they have only ever visited for a week or two at a time. Spending a week at a beachside rental in July is vastly different from navigating local traffic, paying local utility rates, and dealing with year-round weather events. Before you buy a home in a new state, rent a property in your target neighborhood for at least three to six months. Experience the off-season to ensure the community remains vibrant and functional when the tourists leave.

The Medicare Network Trap

If you use Original Medicare (Parts A and B) paired with a Medigap supplement, your coverage generally travels with you to any doctor in the United States who accepts Medicare. However, if you are enrolled in a Medicare Advantage (Part C) plan, your coverage is highly regional. Medicare Advantage plans operate on local networks of doctors and hospitals. Moving out of state—or even just to a different county—will likely force you to drop your current plan and find a new one. Do not assume your favorite national insurance carrier offers the same robust network in a rural South Dakota town as they do in suburban Chicago. You can check network availability in your new zip code using the official Medicare Plan Finder.

The Isolation Trap

Focusing entirely on the cost of living often leads retirees to move far away from their established support networks. While an isolated cabin in the mountains sounds idyllic, aging in place requires infrastructure. Consider how you will access groceries, attend medical appointments, and maintain your home if you temporarily lose your ability to drive. Moving closer to adult children or reliable public transportation often pays massive dividends in your later years.

“The goal of retirement is to live off your assets—not live off your regrets.”

When to Consult a Professional

Relocating across state lines involves complex tax laws and healthcare deadlines. You do not have to figure this out alone. Consider consulting the following experts before you commit to a move.

- Financial Advisor or CPA: State domicile rules are notoriously tricky. If you plan to split your time between two states (the classic “snowbird” strategy), you must prove to the higher-tax state that you have legitimately moved. A CPA will help you establish domicile and understand how the new state taxes your specific blend of pensions, IRAs, and investments. You can find guidance on retirement plan distributions directly through IRS Retirement Plans.

- SHIP Counselor: The State Health Insurance Assistance Program (SHIP) provides free, unbiased Medicare counseling. When you move, you qualify for a Special Enrollment Period to change your Medicare coverage. A local SHIP counselor in your new state can help you compare available plans and ensure your necessary prescriptions are covered.

- Elder Law Attorney: Your estate planning documents—such as wills, trusts, and power of attorney directives—are governed by state law. An elder law attorney in your new state should review your existing documents to ensure they are valid and enforceable under local statutes.

If you are looking for local aging resources, community centers, or transportation assistance in a new city, the Eldercare Locator, managed by the Administration for Community Living, is an excellent place to start your research.

Frequently Asked Questions About Retiring Out of State

Does moving to a new state affect my Social Security payments?

No. Your gross Social Security benefit is federal and remains exactly the same regardless of which state you live in. However, your net take-home amount may change if you move from a state that does not tax Social Security to one of the few states that still applies a tax to these benefits.

How long do I have to live in a state to be considered a resident for tax purposes?

Most states require you to live there for more than 183 days of the year (just over half the year) to be considered a statutory resident. However, states like New York and California look closely at where your “true domicile” is by examining where your car is registered, where you vote, and where your primary doctors are located. Keep meticulous records if you divide your time between states.

What happens to my Medicare coverage when I move?

Original Medicare travels with you anywhere in the U.S. If you have a Medicare Advantage plan or a standalone Part D prescription drug plan, moving out of your plan’s service area triggers a Special Enrollment Period. You typically have the month before your move and two months after your move to enroll in a new plan in your new location without penalty.

Is it cheaper to rent or buy when relocating for retirement?

In 2026, the answer depends entirely on the local market and your timeline. Renting for the first year is almost always the safest strategy. It protects you from buying in the wrong neighborhood and gives you time to understand the true cost of living. Tools like the AARP Livability Index can help you evaluate housing options and neighborhood walkability before making a permanent decision.

Plan Your Next Chapter

Finding the best state to retire is not about chasing the absolute lowest tax rate or following the crowd to the busiest golf course. It is about aligning your physical environment with your financial reality and your personal goals. Take the time to crunch the numbers, visit your top choices during their worst weather months, and have honest conversations with your family about your long-term care preferences.

Your retirement location will serve as the foundation for the next few decades of your life. Start building a shortlist of potential states today, reach out to local experts in those areas, and take the first concrete step toward designing the retirement lifestyle you have earned.

Information in this article reflects current rules as of the publication date and may change. Always confirm benefit details directly with Social Security Administration, Medicare.gov, or relevant government agencies before making decisions.

Last updated: April 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.

I moved from Denver to Rapid City SD because my kids, grandkids live here now. At 70, Retiring this year, if you’re still working, jobs are hard to find. Housing under $300k is a small house, no garage. Unless you play soccor, tennis, hike, there’s not much to do. Larger cities offer classes to take through Parks & Rec. Not here. We still have crime, drugs, violence. Health insurance is not the best. Sanford will be coming in so competion soon. A lot of people go to Omaha or Denver for specialists. Kids have appts at Children’s Hosp in Denver. I hoped to enjoy my backyard, but the wind stops me from sitting on my porch. I miss that in Colo. Cold in the winter -40+ windchills, wind blows. We had 85 mph winds in Jan 2026 that destroyed & relocated my large wooden play set, took out wood fences. I dont think cost of living is different from Denver. Denver has better weather. Property taxes are high. I’m looking for a cheaper house to move into with less than $4k a year property taxes. Count on at least 1-2 large hailstorms in the summer to leave dents on your car. This year the city is charging $100 for a yard trash bin (there’s an ordinance you cant put lawn clippings, weeds in trash bin-had to use approved paper bags that were picked up with trash), with a monthly subscription fee & dump vouchers. We used to make a dump run using your water bill. If you don’t pay for a lawn bin, we have to take lawn waste to a dumpster in town. Water and trash bill is almost $100 with all the taxes, fees they add on-in the winter. I don’t like living here, despite having family closer. Oh & to get a break for seniors age 65+ with property taxes, your income has to be under $20k for 1 person. SD is not a great place to live overall.