Deciding where to spend your golden years requires balancing your desired lifestyle with the realities of a fixed income. If you want to see your retirement savings last as long as possible, relocating to a more affordable city is the most powerful financial lever you can pull. Moving away from high-cost metros allows you to instantly stretch retirement money without drastically altering your daily spending habits. The ideal destination combines affordable housing, favorable senior tax policies, and excellent medical care. We evaluated regional housing markets, state tax exemptions, and daily living expenses to identify seven standout locations. These affordable cities for retirees offer an exceptional quality of life while keeping your long-term financial security firmly intact.

The Blueprint for a Financially Sustainable Retirement City

Relocating is a major life event; doing it strategically can add years of longevity to your investment portfolio. When you transition from earning a salary to living off accumulated assets and fixed benefits, the rules of personal finance change entirely. Your primary focus shifts from income generation to capital preservation and tax efficiency.

To identify the best cities for seniors looking to maximize their nest eggs, you must look beyond the simple sticker price of real estate. A truly affordable retirement destination excels in three specific categories: tax friendliness, housing stability, and healthcare accessibility.

- Favorable Tax Structures: The ideal retirement state does not tax Social Security benefits. Furthermore, the best locations offer generous exemptions on pension income and withdrawals from retirement accounts like IRAs and 401(k)s.

- Reasonable Cost of Living: A low cost of living USA designation means your everyday expenses—groceries, utilities, transportation, and home maintenance—fall below the national average. This prevents the slow drain on your monthly budget.

- Accessible, High-Quality Healthcare: As you age, medical expenses inevitably consume a larger portion of your budget. Living near major health systems ensures you have access to top-tier specialists without incurring the massive travel costs associated with seeking out-of-town care.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” — Robert Kiyosaki

1. Augusta, Georgia: Southern Charm with Massive Tax Benefits

Augusta frequently flies under the radar for retirees flocking to the South, but this historic city offers an incredible combination of southern hospitality and financial prudence. Situated along the Savannah River, Augusta provides a mild climate, beautiful outdoor spaces, and a vibrant cultural scene—all without the premium price tag found in nearby coastal cities like Charleston or Savannah.

Georgia is widely considered one of the most tax-friendly states for retirees. The state completely exempts Social Security income from state taxes. Even more impressively, Georgia offers a retirement income exclusion of up to $65,000 per person for residents aged 65 and older. If you and your spouse both qualify, you can potentially shield $130,000 of retirement income from state taxation every single year. Housing in Augusta is equally appealing; you can comfortably find well-maintained, single-story homes in safe neighborhoods for significantly less than the national median.

From a healthcare perspective, Augusta punches far above its weight class. The city is home to the Medical College of Georgia and a robust network of hospitals and specialized clinics. You secure access to cutting-edge medical treatments and clinical trials right in your backyard, ensuring your physical health is protected just as fiercely as your financial health.

2. Knoxville, Tennessee: Nature Access with Zero State Income Tax

If you dream of an active retirement filled with hiking, fishing, and scenic drives, Knoxville serves as the perfect gateway to the Great Smoky Mountains. While Nashville has seen housing prices skyrocket in recent years, Knoxville remains a bastion of affordability in the Volunteer State. You get all the perks of a vibrant university town—including collegiate sports, lifelong learning opportunities, and a thriving downtown—at a fraction of the cost.

Tennessee levies zero state income tax. This means your Social Security benefits, pension payouts, and IRA withdrawals are entirely yours to keep. For retirees moving from high-tax states like New York or California, this single factor can equate to tens of thousands of dollars in savings over the course of a decade. Property taxes in Knox County are also highly competitive, keeping your fixed monthly overhead exceptionally manageable.

The city features excellent infrastructure for seniors, including reliable public transportation options and numerous community centers offering tailored programming. Healthcare is anchored by the University of Tennessee Medical Center, providing comprehensive geriatric care and specialized services that cater specifically to the aging population.

3. Fort Wayne, Indiana: Unbeatable Housing Affordability

When your primary goal is to minimize housing expenses, Fort Wayne stands out as a premier destination. Located in northeastern Indiana, this city consistently ranks among the most affordable housing markets in the entire country. If you want to downsize and pay cash for a home—thereby eliminating a mortgage payment entirely—Fort Wayne makes that goal highly attainable.

Indiana provides a welcoming tax environment for older adults; the state does not tax Social Security benefits. While standard retirement account withdrawals are subject to the state’s flat income tax, the exceptionally low property taxes and everyday living expenses more than compensate for this. You can stretch retirement money significantly further here, allowing you to allocate funds toward travel, hobbies, or spoiling your grandchildren.

Fort Wayne has invested heavily in its quality of life, recently revitalizing its downtown riverfront area with accessible walking paths, public art, and community gathering spaces. The city boasts a comprehensive healthcare network, including Parkview Health and Lutheran Health Network, ensuring you never have to travel far for routine checkups or emergency care.

4. Winston-Salem, North Carolina: Premier Healthcare on a Budget

North Carolina has long been a favorite destination for retirees relocating from the Northeast, but specific cities within the state offer better value than others. Winston-Salem combines a rich historical legacy with a modern focus on technology and healthcare. The city features a moderate climate with four distinct, yet gentle, seasons, making it ideal for those who want to experience fall foliage and spring blooms without suffering through brutal winters.

Like the other states on this list, North Carolina does not tax Social Security income. The cost of living in Winston-Salem is notably lower than in the state’s larger metros like Charlotte or Raleigh. You can easily find comfortable, accessible housing options, from charming historic bungalows to modern 55-plus communities featuring zero-step entries and lawn maintenance services.

The crown jewel of Winston-Salem is its medical infrastructure. Anchored by Atrium Health Wake Forest Baptist, the city offers world-class medical care, including a renowned comprehensive cancer center and specialized centers for aging and Alzheimer’s research. Knowing you have premier healthcare just minutes away provides an invaluable sense of security during your retirement years.

5. McAllen, Texas: Sunbelt Living at a Steep Discount

For retirees seeking year-round warmth, the Rio Grande Valley offers a tropical climate without the exorbitant costs associated with Florida or southern California. McAllen is a vibrant, culturally rich city located near the southern tip of Texas. It is widely recognized for having one of the lowest costs of living in the United States.

Texas famously levies no state income tax, meaning your entire retirement income stream is protected from state-level deductions. While Texas property taxes can be high in some areas, McAllen’s affordable home prices keep your actual tax bill quite low. Furthermore, Texas offers generous property tax exemptions and deferrals specifically for homeowners aged 65 and older, effectively freezing your school district taxes and protecting you from future rate hikes.

McAllen is renowned for its birdwatching, outdoor recreation, and incredible culinary scene. The healthcare system in the region has expanded rapidly to accommodate the growing population of “Winter Texans”—retirees who migrate south for the winter. You will find modern hospitals and numerous specialists well-versed in senior healthcare needs.

6. Huntsville, Alabama: Intellectual Hub with Low Property Taxes

Known as the “Rocket City” due to its deep ties to the US space program, Huntsville offers a unique blend of intellectual stimulation, high-tech amenities, and southern affordability. Despite rapid economic growth and a booming job market, Huntsville has managed to keep its cost of living incredibly reasonable, making it a hidden gem for retirees.

Alabama is exceptionally friendly to retirees from a tax perspective. The state exempts Social Security benefits and most defined-benefit pensions from state income tax. Where Alabama truly shines is its property taxes, which are among the lowest in the nation. When you combine affordable housing with rock-bottom property taxes, your monthly carrying costs drop dramatically.

Huntsville provides a robust array of cultural amenities, including museums, botanical gardens, and symphony performances. The local healthcare system is anchored by Huntsville Hospital, the second-largest hospital in Alabama, offering comprehensive specialized care. The presence of a highly educated population has fostered a community that values continued learning, making it easy to find engaging social groups and volunteer opportunities.

7. Tucson, Arizona: Desert Beauty Without the Premium Price Tag

Arizona is a classic retirement haven, but areas like Scottsdale and Sedona have become prohibitively expensive for many fixed-income seniors. Tucson offers the quintessential southwestern retirement experience—complete with stunning mountain views, endless sunshine, and a dry climate that is gentle on aging joints—at a much more accessible price point.

Arizona does not tax Social Security benefits, and the state offers a modest exemption for military and civil service pensions. The cost of living in Tucson runs slightly below the national average, but the real savings come from the housing market, which remains significantly more affordable than the Phoenix metropolitan area.

Tucson is a haven for outdoor enthusiasts, offering miles of accessible trails in Saguaro National Park and the surrounding mountain ranges. The city is home to the University of Arizona, providing retirees with discounted access to cultural events, lectures, and sporting events. Healthcare is excellent, with numerous highly-rated hospitals and specialized clinics catering to the region’s large senior population.

Comparing the Financial Benefits

To help you visualize how these locations stack up against each other, review this breakdown of key financial and lifestyle factors. Keep in mind that housing markets fluctuate; these general ranges reflect the sustained affordability of these regions compared to national averages.

| City & State | State Tax on Social Security? | Cost of Living vs. National Avg | Primary Lifestyle Advantage |

|---|---|---|---|

| Augusta, GA | No | Significantly Lower | Generous state retirement income deductions |

| Knoxville, TN | No | Moderately Lower | Zero state income tax; mountain access |

| Fort Wayne, IN | No | Significantly Lower | Unbeatable median home prices |

| Winston-Salem, NC | No | Moderately Lower | Top-tier medical research facilities |

| McAllen, TX | No | Significantly Lower | Zero state income tax; tropical climate |

| Huntsville, AL | No | Significantly Lower | Ultra-low property tax rates |

| Tucson, AZ | No | Slightly Lower | Dry climate; university town amenities |

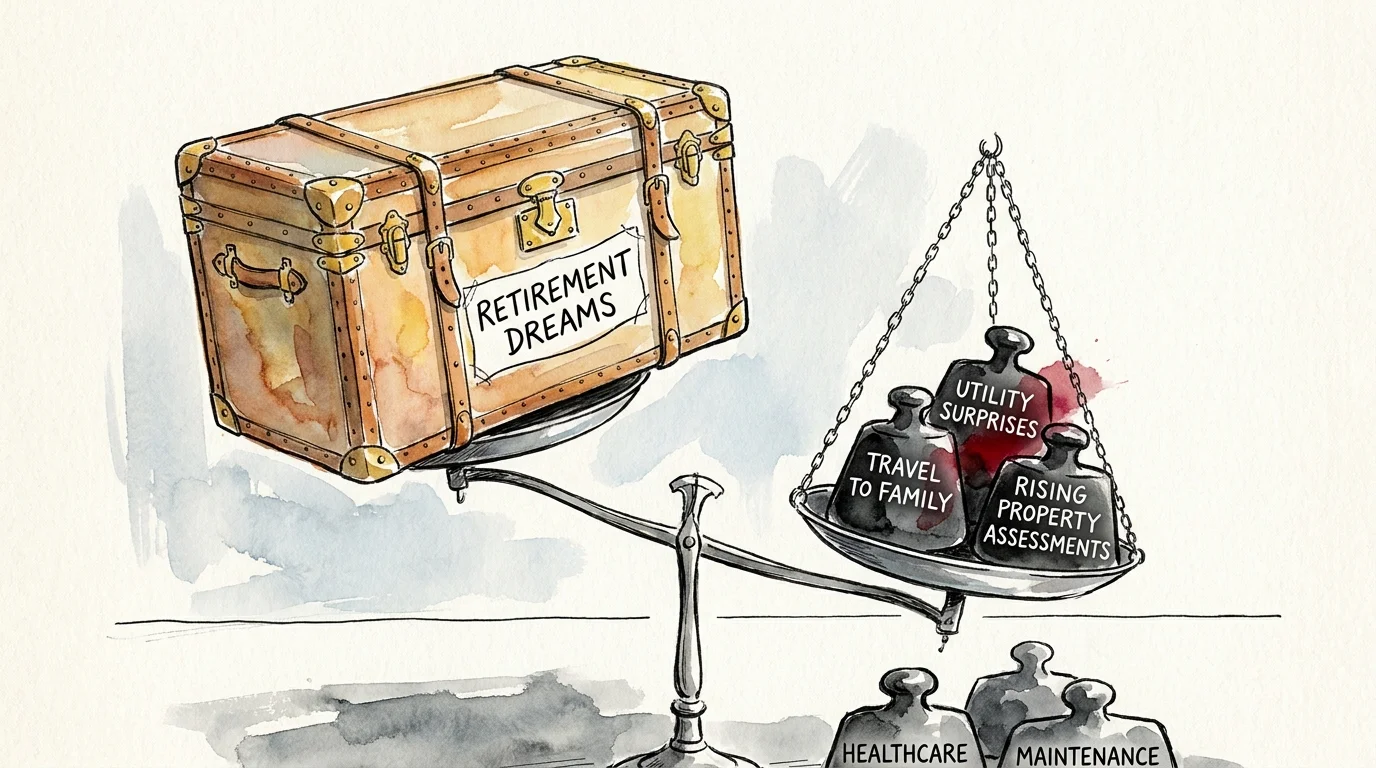

Common Retirement Traps When Relocating

Even when moving to an affordable city, poor planning can quickly erode your expected financial gains. Relocation requires meticulous attention to detail to ensure your new living situation actually saves you money. Avoid these frequent missteps.

Ignoring Healthcare Networks: Medicare Advantage (Part C) plans are highly localized. A plan that provides excellent coverage in your current county may not operate in your new state. Before committing to a move, you must verify your healthcare options. Use the official Medicare Plan Finder to research available plans, premiums, and network providers in your destination zip code. Failing to do so could result in losing access to preferred doctors or facing massive out-of-network bills.

Overlooking Hidden HOA Fees: Many retirees flock to 55-plus communities or low-maintenance condo developments. While the purchase price may seem like a bargain, aggressive Homeowners Association (HOA) fees can completely negate your monthly savings. Furthermore, these fees are subject to annual increases. Always request a history of HOA fee increases and a copy of the reserve study before purchasing a property.

Underestimating the Cost of Travel: Moving halfway across the country to a low cost of living USA destination saves money daily, but how often will you travel back to visit family? If your new city does not have a major airport, or if you must purchase expensive last-minute flights to see your grandchildren, your travel budget can easily consume the money you saved on property taxes.

“The goal of retirement is to live off your assets—not live off your regrets.”

When to Consult a Professional

Relocating across state lines during retirement triggers several complex financial and legal changes. You should absolutely consult a professional team before making your final move.

First, speak with a fiduciary financial advisor or tax professional. Selling a home you have owned for decades can trigger capital gains taxes if the profit exceeds the IRS exclusion limits ($250,000 for singles, $500,000 for married couples). A professional can help you time the sale and structure your withdrawals to minimize your tax burden. You can use resources from the Social Security Administration to calculate how a move might change your overall income strategy.

Second, consult an estate planning attorney in your new state. Estate laws, probate processes, and medical directive requirements vary wildly heavily across state lines. A will or power of attorney drafted in New York might face legal hurdles if executed in Alabama. An attorney will ensure your legacy planning documents align seamlessly with your new state’s legal code.

Finally, consider utilizing the National Council on Aging (NCOA) to research local programs and support systems available in your target city. They provide excellent guidance on navigating senior services in unfamiliar communities.

Frequently Asked Questions

Does moving to a different state affect my Social Security monthly payment?

No. Your baseline federal Social Security benefit remains exactly the same regardless of where you live in the United States. However, the amount of money you actually keep in your pocket may change based on whether your new home state taxes Social Security benefits. Moving to one of the tax-friendly states listed above ensures you keep every dollar of your federal benefit.

Should I rent before buying a home in a new retirement city?

Yes, renting for six to twelve months is highly recommended. Renting allows you to test-drive the neighborhood, experience the climate during different seasons, and ensure the local healthcare and social scenes meet your expectations. If you discover the city isn’t a perfect fit, you can pivot without going through the expensive and stressful process of selling a home you just purchased.

Will my Medicare Supplement (Medigap) plan move with me?

Generally, yes. Unlike Medicare Advantage plans, which are regional, Medicare Supplement plans are standardized federally and usually move with you, provided you stay on Original Medicare. However, your monthly premium may change based on the zip code of your new residence. You must notify your insurance provider of your address change immediately to ensure seamless coverage.

Make Your Next Move Count

Stretching your retirement savings does not require sacrificing your quality of life; it simply requires strategic placement of your assets. By choosing a city that inherently respects your fixed income through low taxes, affordable housing, and accessible healthcare, you reclaim control over your financial future. Take the time to visit these cities, explore their neighborhoods, and crunch the numbers. Your ideal retirement destination is out there waiting for you.

If you feel inspired to explore relocation, start by calculating your projected retirement income and comparing it against the median home prices in your top two destination choices.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Medicare rules, Social Security benefits, and tax laws change regularly—verify current details at Medicare.gov, SSA.gov, or with a licensed professional.