Many Americans spend decades aggressively saving for the future but overlook the essential transition steps required right before handing in their final notice. Stepping away from a steady paycheck is an irreversible financial shift, and minor miscalculations in your final working years often compound into permanent retirement regrets.

Instead of crossing your fingers and hoping your nest egg stretches, you need a concrete strategy to protect your assets, lock in maximum healthcare benefits, and establish a daily purpose.

By addressing seven specific blind spots before you leave the workforce, you can avoid the costly mistakes that blindside even the most diligent savers and step into your next chapter with absolute confidence and financial security.

1. Failing to Test Drive the Retirement Budget

One of the most profound shocks new retirees face is the sudden shift from accumulating wealth to actively draining it. For thirty or forty years, your primary financial goal was watching the balance go up. The psychological friction of watching it go down—even if mathematically planned—can trigger intense anxiety.

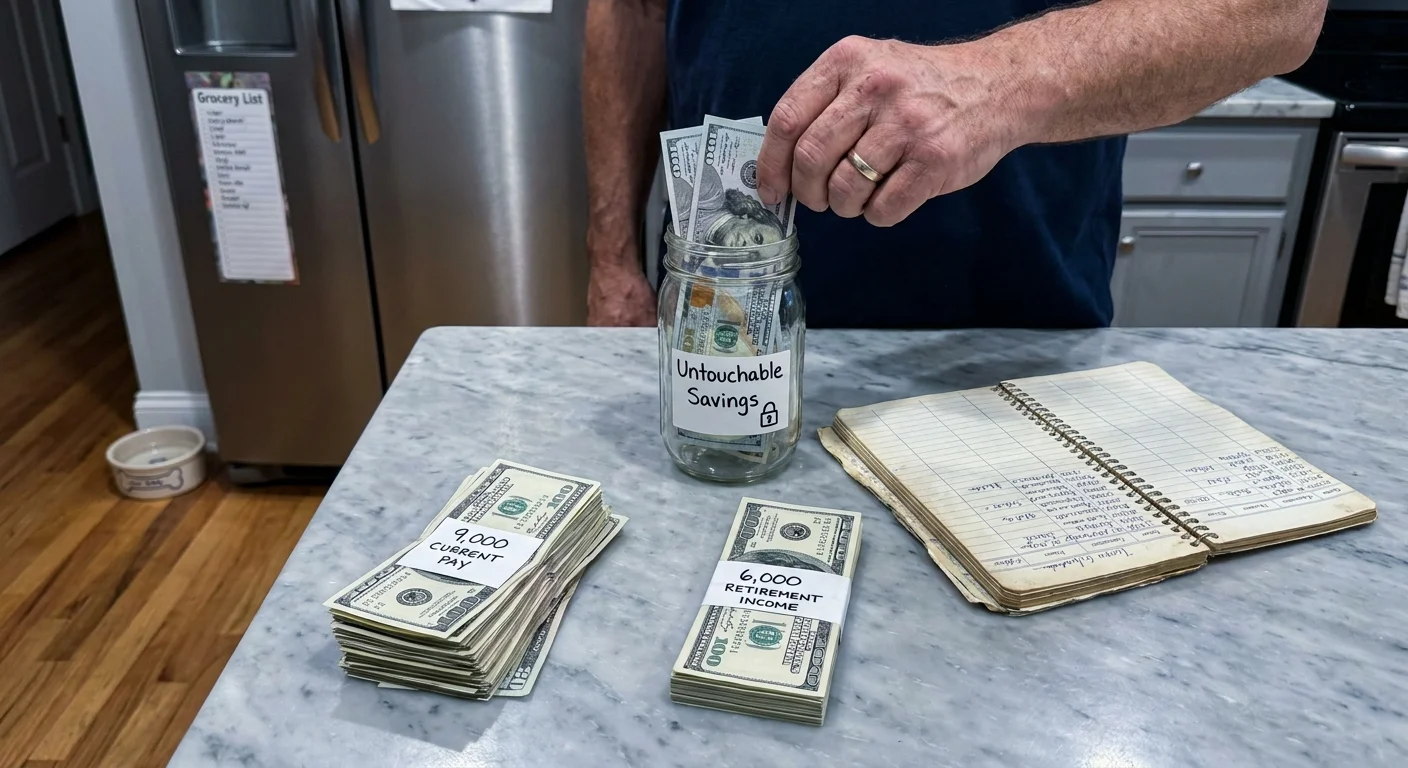

Retirees frequently regret not conducting a “trial run” of their retirement budget while they still had the safety net of their salary. To avoid this, live strictly on your projected retirement income for six consecutive months before your actual retirement date. If you plan to live on $6,000 a month in retirement, but your current take-home pay is $9,000, immediately route the extra $3,000 into an untouchable savings account.

This exercise provides two massive benefits. First, it stress-tests your assumptions. You will quickly discover if your projected budget accounts for inflation, property tax hikes, and those hidden lifestyle expenses you forgot to calculate. Second, it pads your cash reserves right before you stop working. If you find the trial budget too restrictive, you still have your job and can adjust your timeline or savings strategy accordingly.

2. Leaving Employer Healthcare and Benefits on the Table

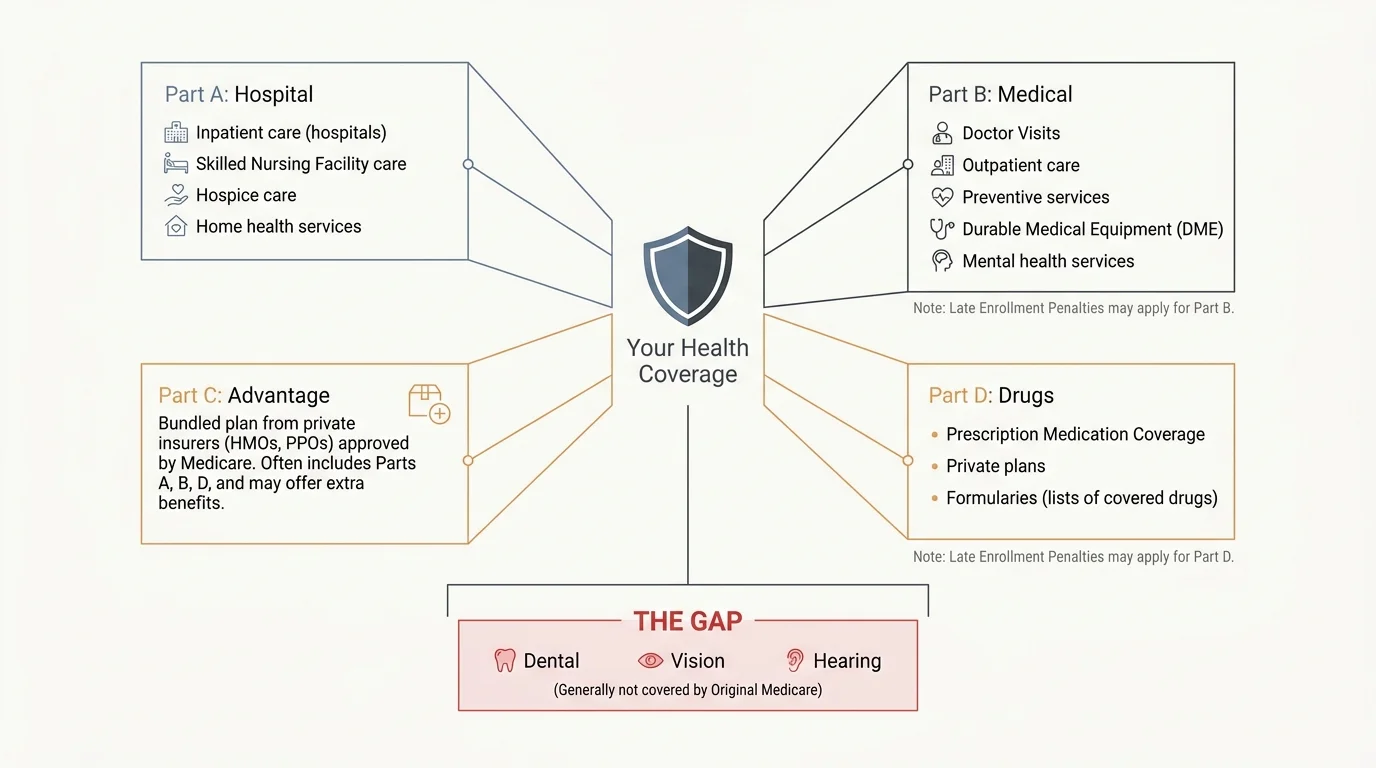

Walking away from comprehensive corporate benefits without a final audit is a costly unforced error. Corporate vision and dental plans are generally far more generous than what you will find on the private market or through basic Medicare options. Medicare Parts A and B do not cover routine dental care, dentures, or eyeglasses.

In the final twelve months of your employment, schedule every major medical, dental, and vision procedure you have been putting off. Secure new eyeglasses, complete necessary dental crown work, and undergo any elective surgeries while you still have your employer’s maximum coverage and out-of-pocket limits working in your favor.

Furthermore, if you have access to a Health Savings Account (HSA) through a high-deductible health plan, max it out. HSAs offer a rare triple-tax advantage: contributions reduce your taxable income, the money grows tax-free, and withdrawals for qualified medical expenses are entirely tax-free. Unlike Flexible Spending Accounts (FSAs), HSA balances roll over indefinitely and serve as a powerful stealth retirement account specifically for healthcare costs.

3. Claiming Social Security Based on Emotion Instead of Math

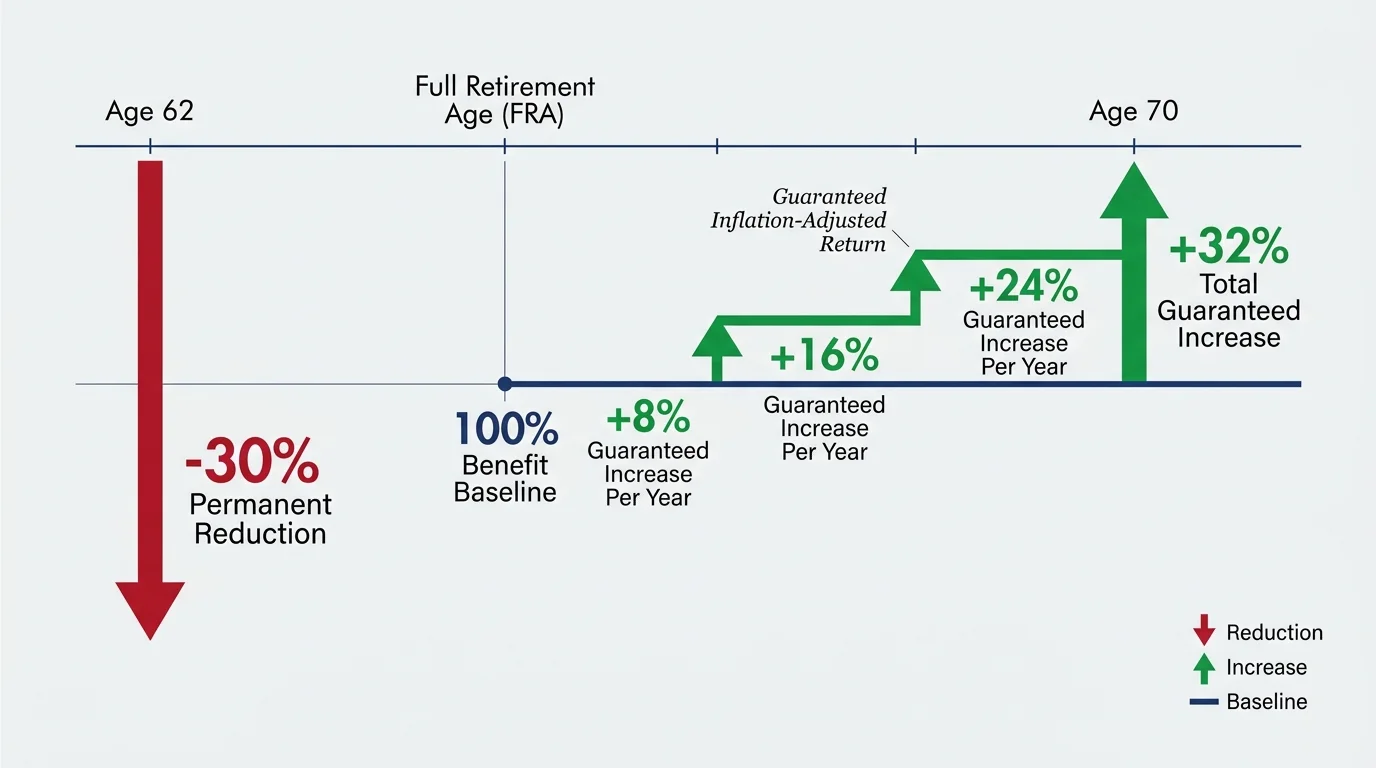

The temptation to claim Social Security at age 62 is powerful. You paid into the system your entire working life, and you want your money. However, locking in permanent reductions to your baseline benefit is a regret that surfaces later in life, particularly when inflation bites or a higher-earning spouse passes away.

Claiming at 62 permanently reduces your monthly check by up to 30% compared to waiting for your Full Retirement Age (FRA). Conversely, for every year you delay claiming past your FRA up to age 70, your benefit increases by a guaranteed 8%. Very few investments offer a guaranteed, inflation-adjusted 8% return in today’s market.

Before submitting your application, you must evaluate your break-even point. Use the official Social Security Retirement Estimator to run specific scenarios. Evaluate your longevity markers, family health history, and how your claiming age impacts your spouse’s survivor benefits. The highest earner in a marriage should strongly consider delaying their claim to age 70, as the surviving spouse ultimately inherits the single largest benefit check when the other passes away.

4. Underestimating the True Cost and Complexity of Medicare

Many workers assume healthcare costs will vanish once they hit 65. The reality is that Medicare requires substantial premium payments, deductibles, and careful plan selection. Failing to understand these mechanics before leaving your employer’s HR department leaves you vulnerable to massive out-of-pocket costs.

You must decide between Original Medicare combined with a Medigap policy, or a bundled Medicare Advantage plan. Retirees who travel frequently or want unrestricted access to specialists often regret choosing restricted networks just to save on upfront premiums.

| Feature | Original Medicare + Medigap | Medicare Advantage (Part C) |

|---|---|---|

| Network Restrictions | None. See any doctor in the U.S. who accepts Medicare. | Restricted to regional HMO or PPO networks. |

| Referrals Needed? | No. You can book specialists directly. | Often required by the primary care physician. |

| Upfront Premiums | Higher monthly cost (Part B + Medigap premium). | Lower monthly cost (often $0 beyond Part B). |

| Out-of-Pocket Costs | Highly predictable; Medigap covers most copays/deductibles. | Variable; you pay copays up to an annual out-of-pocket maximum. |

| Extra Benefits | Does not include dental, vision, or hearing. | Often bundles basic dental, vision, hearing, and gym memberships. |

Spend time on the Medicare Plan Finder tool to input your specific prescription drugs and preferred doctors. Ensure your chosen path aligns with your expected medical needs and your budget for the next twenty years.

5. Retiring “From” Something Without Retiring “To” Something

The financial side of retirement gets all the attention, but the psychological transition derails far more seniors. When you leave work, you do not just lose a paycheck; you lose your daily routine, your primary social network, and often a significant piece of your identity.

“Don’t simply retire from something; have something to retire to.” — Harry Emerson Fosdick

Retirees who leave high-stress careers often envision a life of endless golf, reading, and relaxation. The reality is that permanent vacation quickly transforms into profound boredom and isolation. You need a purpose. Before you turn in your keys, outline your “Tuesday at 10:00 AM” plan. What exactly will you be doing on a random weekday morning when your friends and family are still at work? Whether it involves consulting, volunteering, mentoring, mastering a complex hobby, or helping raise grandchildren, securing your social and intellectual outlets before you retire is crucial for your mental longevity.

6. Carrying the Wrong Kind of Debt Across the Finish Line

Entering retirement completely debt-free is a wonderful goal, but it is not strictly necessary. What matters is cash flow. Retirees often regret aggressively draining their liquid savings to pay off a 3% fixed-rate mortgage, leaving them cash-poor when a medical emergency strikes.

The debt you must eliminate before retiring is high-interest consumer debt. Credit cards carrying 20% interest rates, personal loans, and variable-rate auto loans destroy the efficiency of your fixed income. Every dollar you spend servicing bad debt is a dollar you must withdraw from your portfolio, potentially triggering higher taxes and depleting your principal faster than anticipated.

Restructure your liabilities. If you have five years left in the workforce, redirect your bonus checks and surplus income entirely toward eliminating consumer debt. Protect your cash flow above all else; in retirement, flexibility and liquidity are your ultimate safety nets.

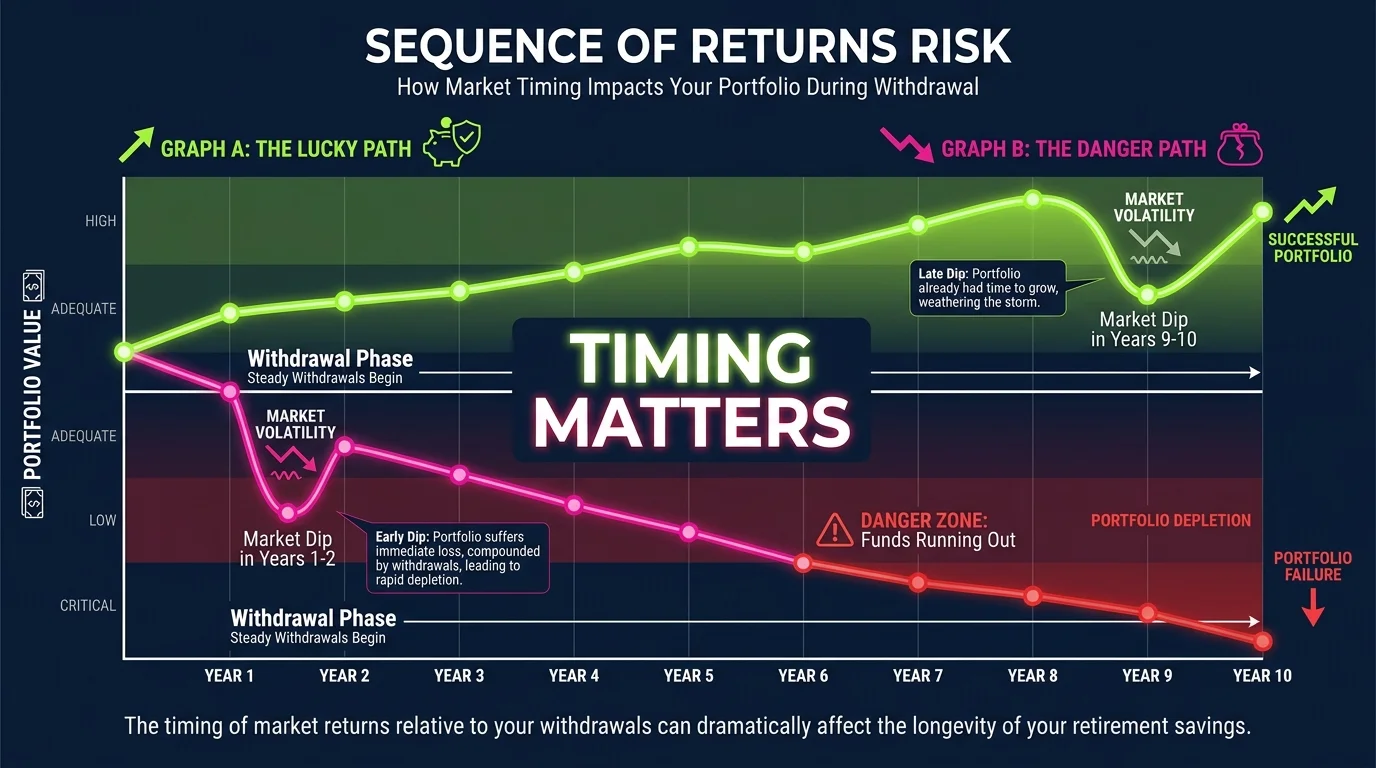

7. Ignoring Sequence of Returns Risk

When you are in your thirties, a stock market crash is a buying opportunity. When you retire, a market crash in your first three years can permanently cripple your portfolio. This mathematical phenomenon is known as “sequence of returns risk.” If you are forced to sell stocks at depressed prices just to buy groceries and pay the light bill, those shares can never participate in the eventual market recovery.

Retirees bitterly regret crossing the finish line without a cash buffer. To protect yourself, establish a “bucket strategy.” Ensure you hold one to two years of living expenses in highly liquid, safe vehicles—such as high-yield savings accounts, Certificates of Deposit (CDs), or short-term Treasury bills. If the market drops 20% the year you retire, you simply spend from your cash bucket, allowing your equity investments the time they need to rebound without realizing permanent losses.

Errors That Cost Retirees Thousands

Even well-prepared professionals stumble on the rigid bureaucratic rules surrounding taxes and government benefits. Watch out for these specific landmines:

- Missing your Initial Enrollment Period for Medicare: If you do not enroll in Medicare Part B when you are first eligible (and do not have qualifying employer coverage), you face a permanent 10% lifetime penalty for every 12-month period you delay.

- Triggering IRMAA surcharges: The Income-Related Monthly Adjustment Amount (IRMAA) is a surcharge added to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. Because Medicare looks at your tax returns from two years prior, a massive severance package or a large Roth conversion right before retirement can drastically spike your healthcare costs.

- Withdrawing from accounts in the wrong order: Pulling all your living expenses from traditional 401(k)s and IRAs creates a massive taxable income event. Blending withdrawals between taxable accounts, tax-deferred accounts, and tax-free Roth accounts helps you manage your tax bracket year by year.

- Failing to plan for Required Minimum Distributions (RMDs): If you have substantial assets in pre-tax accounts, the IRS will force you to begin taking withdrawals at age 73 (or 75, depending on your birth year). This forced income can bump you into a higher tax bracket and trigger taxation on up to 85% of your Social Security benefits.

When to Get Expert Help

Transitioning into retirement is complex, and you do not have to untangle the tax codes and benefit rules alone. Recognizing when to leverage an expert can save you tens of thousands of dollars.

If you are struggling with your Medicare choices, reach out to the State Health Insurance Assistance Program (SHIP). SHIP provides free, unbiased, one-on-one counseling to help you navigate your Medicare options without the pressure of a salesperson. You can find your local office through the National Council on Aging (NCOA) or other community resources.

For your portfolio and tax strategy, hire a fee-only fiduciary financial planner. Unlike brokers who may earn commissions on the products they sell, a fiduciary is legally bound to act in your best interest. Pay them for a standalone comprehensive retirement plan to ensure your withdrawal strategy is sustainable, your tax burden is minimized, and your sequence of returns risk is mitigated.

Finally, consider consulting an elder law attorney to establish your advanced healthcare directives, durable powers of attorney, and estate plans. Getting these legal structures in place while you are healthy ensures your wishes are respected and your family is protected.

Frequently Asked Questions

How far in advance should I start planning my exit strategy?

Ideally, begin your intense transition planning three to five years before your target retirement date. This window gives you enough time to test-drive your budget, shift your asset allocation, aggressively pay down consumer debt, and catch up on major healthcare procedures while still covered by your employer.

Do I have to take Medicare at 65 if I am still working?

If you are actively working and covered by a qualified employer group health plan (from an employer with 20 or more employees), you can generally delay enrolling in Medicare Part B without penalty until you retire. However, you should still verify your specific coverage status with your HR department and the Social Security Administration to avoid lifetime penalties.

What if I realize I made a mistake and want to return to work?

Returning to the workforce—often called “unretiring”—is increasingly common. Just be aware of the earnings test if you have already claimed Social Security before your Full Retirement Age. If you earn over a specific annual limit, the SSA will temporarily withhold a portion of your benefits. Once you reach Full Retirement Age, the earnings limit disappears entirely.

Taking the Next Step

Retirement is the culmination of your life’s work. By stress-testing your budget, maximizing your final corporate benefits, and establishing a clear sense of purpose before you leave the office, you safeguard your transition. Do not let the pressure of these decisions overwhelm you; take them one at a time. Start this week by logging into your employer portal to review your current health benefits, and write down your immediate plan for the first thirty days of your new life.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Medicare rules, Social Security benefits, and tax laws change regularly—verify current details at Medicare.gov, SSA.gov, or with a licensed professional.

Last updated: May 2026. Medicare and Social Security rules change annually—always verify current details at official government sources.