You saved for decades to reach this point. Here’s how to make sure the money lasts as long as you do—with a clear, practical strategy for every stage of retirement.

Here is a number that stops most retirees cold the first time they really sit with it: a 65-year-old American today has roughly a one-in-four chance of living past age 90. For couples, the odds that at least one partner reaches 90 are nearly fifty-fifty.

That means the retirement savings you’ve spent a lifetime building may need to last not ten or fifteen years — but twenty-five, thirty, or even more. And that changes everything about how you need to manage your money.

The accumulation phase of your financial life had a relatively simple goal: save as much as possible and let it grow. The distribution phase — turning those savings into a reliable income that sustains you for three decades — is genuinely more complex. The rules are different. The risks are different. The mistakes are different. And the stakes, frankly, are higher.

The good news is that making your retirement savings last 30 years is entirely achievable with a clear strategy. The not-so-good news is that most retirees are winging it — relying on general rules of thumb, outdated assumptions, and wishful thinking rather than a deliberate, personalized retirement income plan. This article is about closing that gap.

We’re going to walk through every major threat to your retirement savings — and exactly how to neutralize each one. By the end, you’ll have a complete framework for protecting your financial security for the long haul, regardless of what the markets, inflation, or life itself throws at you.

The math of longevity: a 65-year-old woman today has a 50% chance of living to 87 and a 25% chance of reaching 94. A 65-year-old man has a 50% chance of reaching 84 and a 25% chance of reaching 92. Plan accordingly — optimism about longevity is financially prudent, not naive.

Threat #1: Outliving Your Money — and the Withdrawal Rate Problem

The single greatest fear among American retirees — consistently, across every survey — is not death. It is running out of money before they die. And it is a fear grounded in real mathematical risk.

For decades, financial planners pointed retirees to what became known as the 4% Rule: withdraw 4% of your portfolio in year one, adjust for inflation each year after that, and statistically, your money should last 30 years. It became gospel. It’s still widely cited. And it’s no longer enough on its own.

The 4% Rule was developed in the 1990s using historical market data from a period of relatively high bond yields and strong equity returns. Today’s environment — lower long-term bond yields, higher starting valuations in the stock market, and retirees living longer than the original models assumed — means that a rigid 4% withdrawal rate carries more risk than it once did.

This does not mean you need to panic or live on bread and water. It means you need a dynamic withdrawal strategy — one that adjusts based on market conditions, your portfolio performance, and your actual spending needs in any given year, rather than mechanically pulling the same percentage regardless of circumstances.

The Guardrails Approach: A Smarter Way to Withdraw

One of the most practical frameworks financial planners now recommend is the “guardrails” approach to retirement withdrawals. Rather than a fixed percentage, you establish an upper and lower boundary for your withdrawal rate.

If your portfolio performs well and your withdrawal rate drops below the lower guardrail, you give yourself a small spending increase — a raise, essentially. If your portfolio struggles and your withdrawal rate climbs above the upper guardrail, you make a modest, temporary spending reduction — not a dramatic cut, just a recalibration.

This approach gives your retirement income a degree of flexibility that protects your portfolio during downturns without requiring you to live in permanent austerity. It is far more resilient than any rigid rule — and far more psychologically manageable than the anxiety of watching a fixed withdrawal drain a shrinking portfolio.

Practical starting point: rather than asking “what is my withdrawal rate?”, ask “what is the minimum I need each month to cover essential expenses — and what is the lifestyle amount I’d ideally like?” The gap between those two numbers is where your strategy lives. A certified financial planner (CFP) can build a dynamic withdrawal model around your specific numbers.

Threat #2: Inflation — The Slow Drain Most Retirees Underestimate

~50% of purchasing power lost

What $1,000 buys today versus what it bought 25 years ago — the quiet cost of inflation over a long retirement

Inflation is the most patient threat to retirement savings because it works so slowly that retirees often don’t notice it until real damage is done. A 3% average annual inflation rate — which is historically modest — cuts the purchasing power of a fixed income by nearly half over 25 years.

Think about what that means in practice. If your retirement income covers your expenses comfortably at 65, that same income may cover only 60–70% of the same lifestyle by the time you’re 80 — not because your spending changed, but because prices did. Groceries, utilities, healthcare, insurance, property taxes — all of it costs more every year.

Social Security has one powerful built-in inflation protection: the annual Cost of Living Adjustment (COLA), which ties your benefit to the Consumer Price Index. This is one of the most underappreciated features of Social Security, and it is a key reason why delaying your claim to maximize your monthly benefit is so strategically powerful for long-term financial security.

Beyond Social Security, protecting against inflation requires keeping a meaningful portion of your retirement portfolio invested in assets that historically outpace inflation over long periods — primarily a diversified equity allocation. The retirees most vulnerable to inflation are those who move entirely into cash and bonds at retirement, eliminating the growth engine from their portfolio precisely when they need it most.

The common mistake: moving to an “all safe” portfolio at retirement — 100% bonds, CDs, or money market funds — feels cautious but is actually one of the riskiest long-term decisions a retiree can make. A 30-year retirement needs growth. A blanket bond portfolio almost guarantees that inflation wins.

Threat #3: Sequence of Returns Risk — Why the First Five Years Matter Most

This is the retirement risk that most retirees have never heard of — and it may be the most dangerous one of all.

Here’s the core idea: the order in which your investment returns occur matters enormously when you are simultaneously withdrawing from your portfolio. Two retirees can have identical average returns over a 30-year retirement and end up with radically different outcomes — based purely on whether the bad years came at the beginning or the end.

A severe market downturn in your first three to five years of retirement — when your portfolio is at its largest and you are pulling from it to fund your life — causes permanent damage that a later recovery cannot fully repair. You are selling assets at depressed prices to meet living expenses. Those sold assets never participate in the recovery. The math works against you in a way that simply doesn’t apply during accumulation.

How to Protect Yourself: The Bucket Strategy

The most widely recommended defense against sequence of returns risk is the bucket strategy — dividing your retirement savings into distinct pools with different time horizons and risk levels.

Bucket One holds one to three years of living expenses in cash or near-cash equivalents — high-yield savings accounts, money market funds, or short-term Treasury bonds. This is your spending bucket. When the market falls, you draw from here — leaving your invested assets untouched while they recover.

Bucket Two holds three to ten years of projected spending in moderately conservative investments — a mix of bonds, dividend-paying stocks, and other income-generating assets. As Bucket One is depleted, Bucket Two refills it.

Bucket Three holds the remainder in a growth-oriented, longer-term portfolio — diversified equities, real assets, or other higher-return investments designed to fund the later decades of retirement and outpace inflation. This bucket has time to ride out market volatility because you won’t need it for a decade or more.

The bucket strategy doesn’t require a perfect prediction of the market. It simply ensures that short-term market turbulence never forces you to sell long-term investments at exactly the wrong moment — which is the core of what makes sequence of returns risk so damaging.

The bucket strategy is powerful because it is also psychologically protective. When the market drops sharply, you are not watching your “money” disappear — you are watching your long-term bucket fluctuate while your short-term bucket quietly covers your actual life. That distinction makes it far easier to stay the course rather than panic-selling at the bottom.

Threat #4: The RMD Time Bomb — Required Minimum Distributions Explained

If you have money sitting in a traditional 401(k), traditional IRA, or other tax-deferred retirement account, the IRS has not forgotten about it. In fact, they have a very specific schedule for when you must start withdrawing it — whether you need the money or not.

Required Minimum Distributions (RMDs) are mandatory annual withdrawals from tax-deferred retirement accounts that begin at age 73 under current law (a provision of the SECURE 2.0 Act, which also raises this age to 75 for those born in 1960 or later). The amount you must withdraw each year is calculated by dividing your account balance by an IRS life expectancy factor.

The problem isn’t the withdrawal itself — it’s the tax consequences. Every dollar you pull from a traditional 401(k) or traditional IRA counts as ordinary income in the year you receive it. For retirees with large tax-deferred balances, RMDs can push them into a significantly higher tax bracket, trigger IRMAA surcharges on their

Medicare premiums, increase the taxable portion of their Social Security benefits, and reduce their eligibility for income-based financial assistance. This is why proactive RMD planning — ideally beginning years before age 73 — is one of the highest-value conversations a retiree can have with a certified financial planner.

The Roth Conversion Strategy: Defusing the RMD Bomb Before It Goes Off

One of the most powerful tools for managing RMD risk is the Roth IRA conversion — converting some or all of your traditional IRA or 401(k) balance into a Roth IRA during the years before your RMDs begin.

When you convert, you pay income tax on the converted amount in the year of the conversion. In exchange, those funds — and all their future growth — become permanently tax-free. Roth IRAs also have no RMD requirement during the owner’s lifetime, which gives you complete flexibility over when and whether you withdraw.

The optimal window for Roth conversions is typically the years between retirement and age 73 — especially if you retire before Social Security begins and before RMDs kick in. In those early retirement years, your taxable income may be temporarily lower than at any point in your career, creating a strategic tax window to convert at a favorable rate.

How much to convert, and in which years, depends on your specific tax situation, your current and projected future brackets, your state’s tax treatment of conversions, and your overall retirement income picture. This is exactly the kind of multi-year, personalized analysis that a fee-only certified financial planner (CFP) is best positioned to provide.

Missing an RMD — or taking less than the required amount — triggers one of the steepest penalties in the tax code: a 25% excise tax on the amount you should have withdrawn. Set calendar reminders, work with your financial advisor, and treat RMDs with the same seriousness as a tax filing deadline. They are.

Threat #5: Healthcare Costs — The Budget Item That Grows Every Year

Healthcare is the fastest-growing expense in most retirement budgets — and the one most consistently underestimated when retirees do their pre-retirement financial planning.

A 65-year-old retiring today can expect to spend, on average, well over $150,000 on out-of-pocket healthcare costs during their retirement — and that figure climbs dramatically for those with chronic conditions, those who live into their late eighties or nineties, or those who ultimately require assisted living or skilled nursing care.

Medicare covers a great deal, but it doesn’t cover everything. There are premiums — Part B currently runs $185 per month per person in 2026. There are deductibles, co-pays, and coinsurance. There are gaps in coverage for dental, vision, and hearing. And there is the enormous potential expense of long-term care — which Medicare does not cover at all.

Building a Healthcare Financial Strategy

Your retirement income plan needs a dedicated healthcare cost model — not a vague line item, but a genuine projection of your expected Medicare premiums (including IRMAA surcharges if your income is higher), Medicare supplement insurance or Medicare Advantage plan costs, out-of-pocket maximums, prescription drug costs under Part D, and a realistic long-term care scenario.

Long-term care insurance — or hybrid life insurance policies with long-term care riders — should be part of this conversation. The median annual cost of assisted living in the United States now exceeds $60,000, and a skilled nursing facility can run $100,000 or more per year. For retirees without a plan to cover these costs, a single health event can devastate a retirement portfolio that took a lifetime to build. Discuss long-term care planning with a financial advisor well before you think you need it.

If you have a Health Savings Account (HSA) from your working years, it becomes one of your most powerful retirement healthcare assets. HSA funds can be withdrawn completely tax-free for qualified medical expenses — including Medicare premiums, dental and vision costs, and long-term care insurance premiums up to IRS limits. If you have an HSA, protect it and let it grow specifically for healthcare costs in retirement.

Important planning note: IRMAA — the Income-Related Monthly Adjustment Amount — adds significant surcharges to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. In 2026, the surcharges begin for individuals earning above $106,000. Strategic retirement income planning — including careful Roth conversion timing and capital gains management — can help keep your income below these thresholds.

Threat #6: Taxes in Retirement — The Bill Most Retirees Don’t See Coming

Many retirees are genuinely surprised to discover how much of their retirement income is taxable. They spent their careers deferring taxes — contributing to traditional 401(k)s and IRAs — and now the bill arrives in the form of taxable withdrawals, potentially taxable Social Security benefits, and capital gains on investments.

How Much of Your Social Security Is Taxable?

Up to 85% of your Social Security benefits can be subject to federal income tax, depending on your “combined income” — a formula that adds your adjusted gross income, non-taxable interest, and half of your Social Security benefit. If that combined figure exceeds $34,000 for single filers or $44,000 for married couples filing jointly, up to 85% of your benefit is taxable.

This threshold has not been adjusted for inflation since it was set in 1984, which means more and more retirees fall into the taxable zone every year — regardless of whether they consider themselves high-income. Managing your income strategically to stay below these thresholds is one of the most overlooked retirement tax planning opportunities.

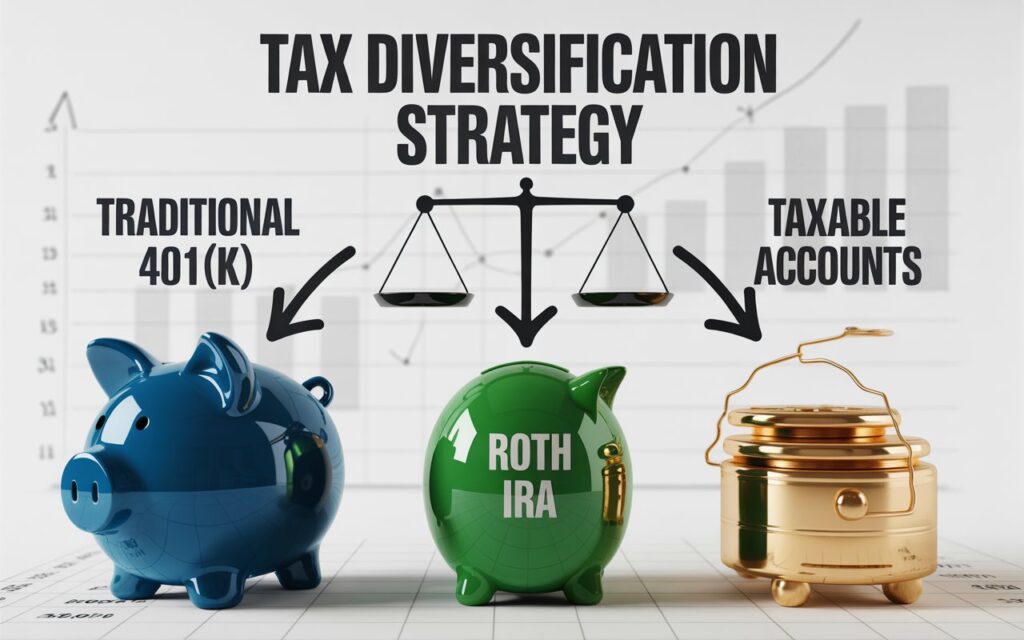

The Power of Tax Diversification

The most tax-resilient retirement portfolios draw income from three different types of accounts: taxable accounts (regular brokerage accounts, where you pay capital gains rates), tax-deferred accounts (traditional 401(k) and IRA, taxed as ordinary income on withdrawal), and tax-free accounts (Roth IRA and Roth 401(k), with no tax on qualified withdrawals).

Having all three gives you enormous flexibility to manage your taxable income in any given year — pulling from whichever source minimizes your tax bill based on your circumstances that year. Retirees who saved exclusively in tax-deferred accounts lose this flexibility entirely, which is why tax diversification is ideally built during the accumulation phase but can still be improved during retirement through strategic Roth conversions.

A tax-efficient withdrawal order to discuss with your CFP: in most scenarios, drawing first from taxable accounts, then tax-deferred, then Roth — while strategically filling lower tax brackets with Roth conversions — produces the best long-term outcome. But this general rule has many exceptions depending on your specific situation, state taxes, and income needs.

Threat #7: Overconservatism — Playing It So Safe You Run Out Anyway

Here is a retirement risk that never gets the attention it deserves, because it doesn’t feel like a risk. It feels like prudence.

Moving your entire retirement portfolio into cash, CDs, or short-term bonds at retirement feels safe. It is psychologically comfortable. It eliminates the anxiety of watching a stock portfolio fluctuate. And it is, for most retirees with a 20–30-year horizon, one of the most financially dangerous decisions they can make.

The math is straightforward. Inflation — even at a modest 3% per year — means your purchasing power halves in roughly 24 years. A portfolio that generates no real returns is a shrinking portfolio. And a shrinking portfolio, combined with three decades of withdrawals, runs out of money just as surely as a portfolio decimated by bad markets — only more slowly and more predictably.

This does not mean you should take on inappropriate risk or ignore your comfort level. It means that your asset allocation in retirement needs to be calibrated to your time horizon, not your fear level. A 65-year-old with a 30-year horizon has a very different risk profile than a 90-year-old. The portfolio should reflect that.

Most financial planners recommend that retirees maintain a meaningful equity allocation — typically somewhere between 40% and 60% of the portfolio in diversified stocks, depending on their specific situation — well into their seventies. The exact allocation should be determined with a certified financial planner who understands your full financial picture, your income needs, and your genuine risk tolerance.

The hidden danger of “safe” money: CDs and money market funds can feel like protection, but at current rates they often fail to keep pace with inflation over long periods. A retiree who shifted everything to 5% CDs in 2023 locked in returns that look good today but will underperform a balanced portfolio over a 20-year period in most historical scenarios.

Should You Consider an Annuity? The Honest Answer

No discussion of making retirement savings last is complete without addressing annuities — one of the most debated, most misunderstood, and most frequently both over-sold and unfairly dismissed financial products in the retirement landscape.

At their core, annuities are insurance products. You give an insurance company a sum of money, and they guarantee to pay you a stream of income — for a set period, or for the rest of your life. A simple income annuity, sometimes called a single premium immediate annuity (SPIA), does exactly one thing: it converts a lump sum into a guaranteed lifetime income stream. That is its value.

For retirees who have a significant gap between their guaranteed income (Social Security, pension) and their essential monthly expenses, a portion of retirement savings converted into a lifetime annuity can close that gap permanently. It eliminates longevity risk for that portion of your income — you cannot outlive an annuity payment.

Here’s How Social Security Benefits Work for Retirees — A Complete Overview

The trade-off is that you give up control of that capital. If you buy a $200,000 annuity and die two years later, the insurance company keeps the money (unless you purchased a rider protecting a minimum payout period). Annuities also typically don’t keep pace with inflation unless you pay extra for an inflation-adjustment feature.

The right question is not “are annuities good or bad?” but “does a lifetime income annuity solve a specific problem I have — and does the guarantee justify the cost and the loss of flexibility?” That is a conversation for a fee-only certified financial planner who is not compensated by commissions on annuity sales.

Rule of thumb: annuities make the most sense when used to cover essential, non-negotiable expenses — housing, food, utilities, healthcare premiums — turning that baseline into a guaranteed floor no market event can touch. They make less sense as a vehicle for all your retirement savings or as an investment product. Use them surgically, not broadly.

The 10 Golden Rules of Making Your Retirement Savings Last

Pull these together and you have a complete operating framework for a 30-year retirement:

1. Know your number — exactly.

Calculate the precise annual income your essential expenses require. Not a rough estimate. The actual number. That is your floor, and every strategic decision builds up from it.

2. Delay Social Security as long as your health and finances allow.

Every year you wait past your Full Retirement Age adds 8% to your benefit — permanently, and indexed to inflation for life. This is one of the best guaranteed returns available anywhere.

3. Use the bucket strategy to protect against sequence of returns risk.

Never be in a position where a market downturn forces you to sell long-term investments to fund short-term living expenses. Your short-term bucket prevents this.

4. Start Roth conversion planning the day you retire.

The window between retirement and age 73 is often your lowest-income, lowest-tax window in decades. Use it deliberately to reduce future RMDs and build a tax-free income source.

5. Keep a meaningful equity allocation for as long as your situation permits.

You cannot outrun inflation with bonds and cash alone over a 30-year horizon. Growth is not optional — it is what makes the money last.

6. Model your healthcare costs specifically, not generically.

Healthcare is not a line item — it is a financial plan within your financial plan. Know your Medicare costs, your Part D costs, your out-of-pocket exposure, and your long-term care scenario.

7. Manage your taxable income actively, every year.

Know where you stand relative to Roth conversion sweet spots, Social Security taxation thresholds, and IRMAA Medicare surcharge brackets. Tax planning in retirement is not a one-time event.

8. Review your plan annually — every single year.

Your portfolio performance, your health, tax laws, market conditions, and spending needs all change. Your retirement income strategy should adapt with them, not sit static in a plan written at 65.

9. Protect your plan from emotional decisions.

Market downturns will happen. Scary news cycles will happen. The most financially destructive thing most retirees do is panic-sell during market corrections. Your bucket strategy and your financial plan are your armor against this.

10. Work with a fee-only certified financial planner (CFP).

Not a salesperson. Not a broker with commissions to earn. A fiduciary, fee-only planner whose legal obligation is to act in your best interest. This relationship — revisited annually — is the single highest-return investment most retirees can make.

You Saved for Decades. Now Make It Last.

Thirty years is a long time. It’s long enough to see grandchildren graduate from college, to travel to places you’ve always dreamed about, to build a second chapter of life that might surprise you with how rich and full it becomes.

It’s also long enough for all the threats we’ve described in this article — inflation, sequence of returns, rising healthcare costs, unexpected tax bills, excessive caution — to erode financial security that took a lifetime to build quietly.

The difference between retirees who spend those thirty years with confidence and those who spend them with anxiety almost always comes down to one thing: a genuine, thoughtful, regularly reviewed financial plan. Not a plan written once and filed away. A living plan — one that adapts as markets change, as health changes, as life changes.

You did the hard work. You saved. You sacrificed. You showed up for your future self for decades.

Now it’s time to be as deliberate about protecting what you’ve built as you were about building it. Your retirement deserves nothing less.